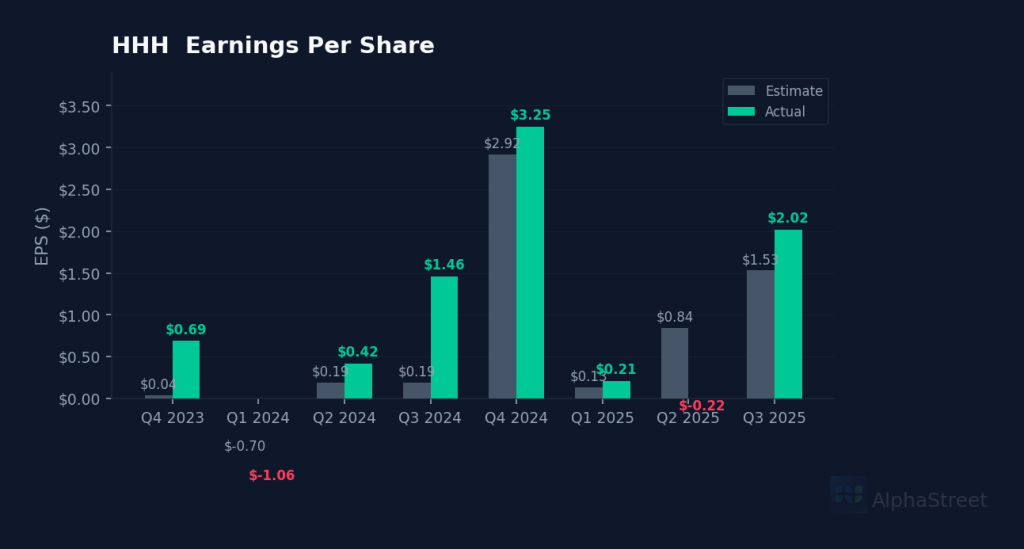

Real estate developer crushes the bar. Howard Hughes Holdings Inc. (HHH) delivered Q4 2026 EPS of $2.02, demolishing the consensus estimate of $1.53 by 32.0%. Revenue reached $1.83B for the quarter, though no Wall Street consensus was available for comparison. The real estate development firm’s bottom-line performance marks a dramatic turnaround from Q2 2025’s -$0.22 miss and continues the company’s volatile earnings pattern.

Muted market response despite the beat. Shares edged up just 0.19% to $83.03 in after-hours trading following the announcement, suggesting investors had already priced in strong results or remain cautious about the company’s lumpy earnings profile. The stock traded at $82.57 during the regular session, up 1.39% from the prior close of $81.44. HHH has climbed 7.1% over the past three months after bottoming near $78 in late December.

Land sales drive the upside. Management commentary from the Q3 2025 call (the most recent transcript available) provides context for the strong quarter. CEO David O’Reilly emphasized that super pad land sales would continue “at a much higher gross and net price per acre” following a large parcel transaction. CFO Carlos Olea disclosed refinancing of $114M in near-term debt maturities during Q3, pushing obligations into 2026 and beyond—a move that likely improved the company’s cash flow profile heading into Q4.

The valuation disconnect widens. At the current price, HHH trades at 15.3x trailing twelve-month earnings but a steep 81.0x forward P/E, reflecting Wall Street’s expectation that Q4’s $2.02 result represents an outlier rather than a sustainable run rate. Analysts project Q1 2026 EPS of just $0.64, implying the company’s master-planned community land sales remain highly episodic. The average analyst target of $96.33 suggests 16.7% upside from current levels.

Balance sheet in focus. The company completed a senior notes offering through its wholly owned subsidiary The Howard Hughes Corporation in mid-February, according to a press release dated February 17, 2026. This capital markets activity, combined with the Q3 refinancing efforts, positions HHH to fund ongoing development at its master-planned communities including The Woodlands (Texas), Bridgeland, and Summerlin (Nevada). Total assets stood at $10.7B as of Q3 2025, up from $9.2B at year-end 2024.

Operating leverage emerges. The company’s 44.9% operating margin and 15.0% profit margin demonstrate the high-margin nature of mature land parcels, though these figures fluctuate significantly based on the timing and mix of closings. Revenue growth of 19.3% year-over-year reflects strong demand for developed land in key Sunbelt markets where HHH maintains its flagship communities.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.