The stocks of Home Depot (NYSE: HD) and Lowe’s (NYSE: LOW) have gained over 9% and 11% respectively, this year. The challenging macro environment has pressured the home improvement industry dampening the near-term outlook but there are still a couple of reasons to retain optimism. Here’s a look at what these two home improvement retailers anticipate for the foreseeable future:

Recent quarterly performance

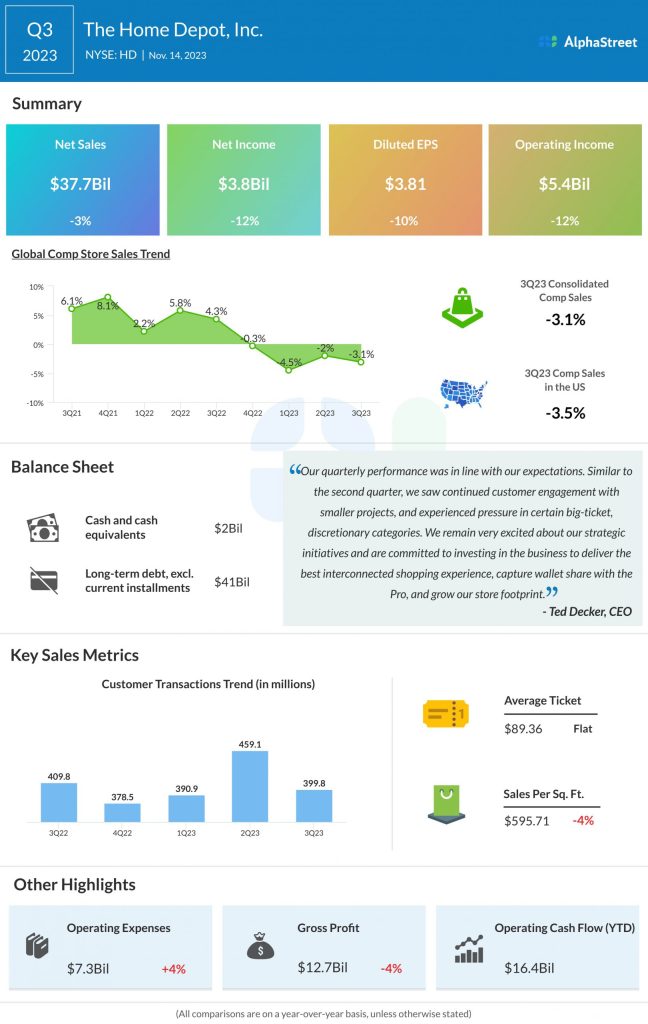

Home Depot and Lowe’s saw sales and comps decline in their most recent quarter. In the third quarter of 2023, Home Depot’s net sales decreased 3% year-over-year to $37.7 billion and its comparable sales decreased 3.1%. Lowe’s net sales in Q3 2023 dropped 13% YoY to $20.5 billion while its comparable sales fell 7.4%. Home Depot’s EPS decreased 10% to $3.81 during the quarter while Lowe’s EPS rose to $3.06 from $0.25 reported in the prior-year period.

Category and market trends

In their most recent quarter, both home improvement retailers saw pressure in big-ticket, discretionary categories. Home Depot saw customers focus on smaller home improvement projects instead of large-scale renovations. Lumber deflation was another factor that impacted business performance. All these led to declines in comp transactions and comp average ticket for both companies.

Home Depot and Lowe’s also saw the Pro customer segment outperform the DIY segment. The retailers saw strength in Pro-heavy categories like roofing, rough plumbing and paint. On its Q3 conference call, Home Depot said that although Pro backlogs appear to be lower compared to a year ago, they remain healthy and elevated relative to historical norms. The majority of Lowe’s Pro customers also appear to have healthy backlogs, which mostly comprise necessary repairs on aging homes.

Home Depot sees vast opportunity in Pro spend, which represents a $475 billion addressable market. The retailer holds only a small share in this space, which provides room for further expansion. As part of these efforts, the company struck a deal to acquire International Designs Group, the owner of architectural specialty products company Construction Resources.

Outlook

Home Depot and Lowe’s both revised their outlook for the full year of 2023. Home Depot now expects its sales and comparable sales to decline 3-4% from the previous year. EPS is now estimated to decline 9-11% from last year. The company’s previous expectations were for sales and comps to decline 2-5% and EPS to decline 7-13%.

Lowe’s lowered its FY2023 guidance due to lower DIY discretionary spending and macroeconomic uncertainty. It now expects total sales of approx. $86 billion and adjusted EPS of approx. $13.00 for the year. The prior outlook was for sales of $87-89 billion and adjusted EPS of $13.20-13.60. Comparable sales are now expected to decline 5% instead of the prior range of 2-4%.

Despite this, Lowe’s remains bullish in its medium to long-term outlook for the home improvement industry on the back of tailwinds such as millennial household formations, people choosing to age in place in their own homes, and an aging housing stock that will need repairs and remodels.