Shares of Home Depot Inc. (NYSE: HD) have gained 27% over the past 12 months. The company benefited during the pandemic from strong demand for its products as customers took an increased interest in home improvement projects while spending more time at home. Home Depot ended fiscal year 2021 on a solid note with strong results for both the fourth quarter and full year.

Looking ahead, the company anticipates that a supportive macroeconomic environment and significant market opportunity will help drive growth for its business. However, there is a certain level of uncertainty caused by inflation and supply chain issues. Here are a few trends that provide optimism for the home improvement retailer over the long term:

Strong performance

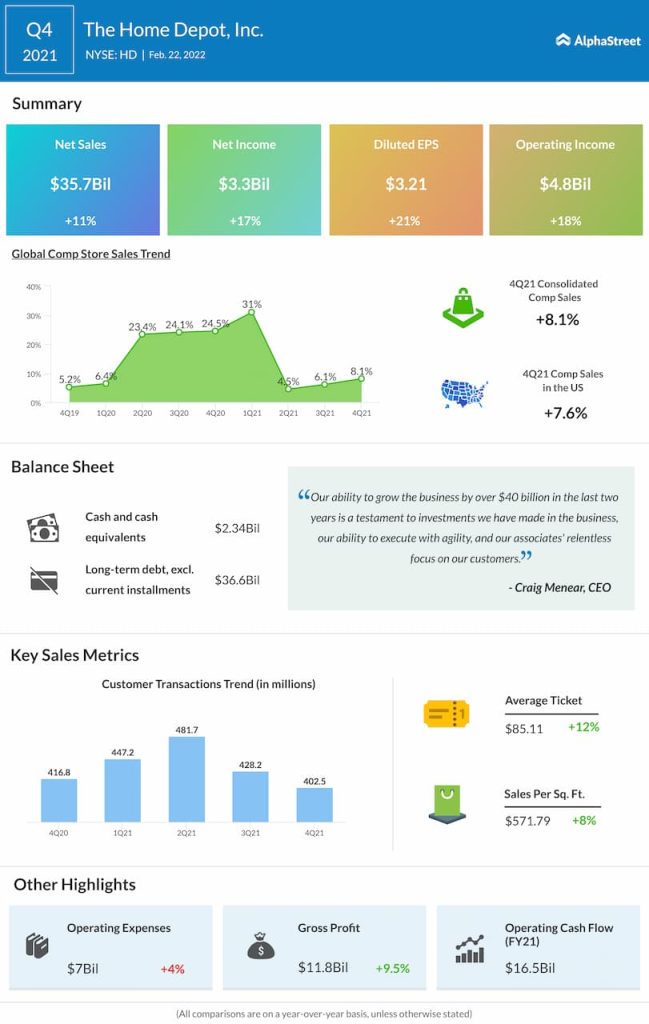

Home Depot reached a new milestone in fiscal year 2021 as it crossed over $150 billion in sales. The company grew its business by over $40 billion over the last two years while before the pandemic, it took nine years for it to accomplish the same feat. Home Depot also delivered double-digit comp growth during FY2021.

In the fourth quarter, total sales increased 10.7% year-over-year to $35.7 billion. Comp sales grew 8.1% while US comps rose 7.6%, helped by positive comps across all geographies and merchandise departments. EPS rose 21.1% to $3.21 in Q4 while margins took a hit due to product mix and investments in the supply chain network.

Home Depot recorded a 12.3% growth in comp average ticket, driven mainly by inflation across product categories such as lumber, building materials and copper. Big-ticket comp transactions were up 18% YoY, with strength in both Pro and DIY customers.

Housing market trends

On its quarterly conference call, Home Depot stated that there is a strong demand for homes currently and there are less number of homes available for sale which indicate that home prices could continue to increase.

The housing stock continues to age and there is healthy demand for home improvement projects. Despite this, there is uncertainty with regards to the impact of inflation, supply chain dynamics, and how consumer spending will evolve through the coming year.

Home Depot estimates its total addressable market in North America to be greater than $900 billion. The company sees significant growth opportunities with both DIY and Pro customers, with each of these groups representing an estimated 50% of the total addressable market. Home Depot also estimates that each of these groups represents around 50% of its total sales.

The company believes the addressable end market for Pro is over $450 billion. Within this, the addressable maintenance, repair and operations space is estimated to have expanded to over $100 billion. Home Depot represents a small part of a large and fragmented market that has seen meaningful expansion over the past two years.

Outlook

Home Depot estimates sales growth and comp sales growth to be slightly positive for FY2022. Operating margin is expected to be flat to 2021 while EPS is projected to see low single digit percentage growth compared to last year.

Click here to read the full transcript of Home Depot’s Q4 2021 earnings conference call