Shares of Hormel Foods Corporation (NYSE: HRL) were up over 2% on Thursday. The stock is recovering from a fall it took a day ago after the company delivered mixed results for the third quarter of 2024 and lowered its guidance for the full year. Here are a few factors that put a damper on the Q3 performance:

Sales and earnings decline

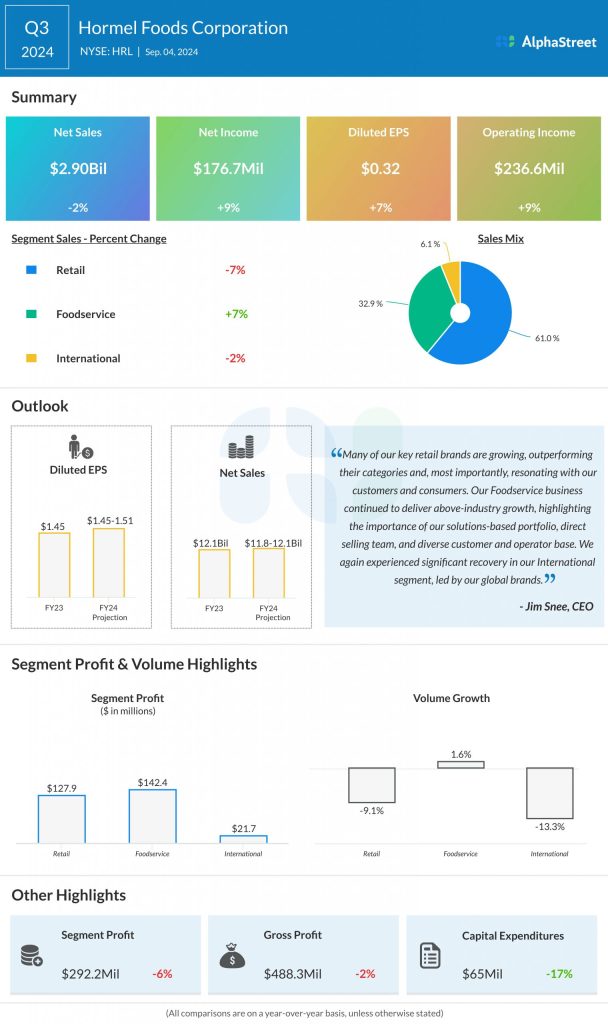

Hormel saw its sales and adjusted EPS decline on a year-over-year basis in Q3 2024. Net sales decreased 2% to $2.90 billion. The top line also fell short of expectations. Adjusted EPS of $0.37 was down 7% from last year but came ahead of projections.

Segment declines

In the third quarter, Hormel recorded sales declines in both its Retail and International segments. These declines offset sales growth in the Foodservice segment. The Retail segment saw sales decrease 7% and volumes decrease 9%, mainly due to lower sales of whole bird turkeys, lower sales of Planters snack nuts due to a production disruption at the Suffolk facility, and softness in the contract manufacturing business.

These headwinds were partly offset by sales growth for key brands such as Hormel Black Label bacon, Jennie-O lean ground turkey, SPAM luncheon meats, and Skippy peanut butter. The company is also seeing trends stabilize in the convenient meals and proteins business.

In the International business, sales dropped 2% while volume fell 13%. Sales and volume growth for SPAM luncheon meat, refrigerated foodservice exports, and Skippy peanut butter exports were more than offset by tough prior-year comparisons to higher export volumes of low-margin commodity fresh pork and turkey.

The Foodservice segment recorded sales growth of 7% and volume growth of 2% in Q3, driven by gains in the turkey, bacon, pepperoni, and premium prepared proteins categories. Hormel saw strong sales and volume growth for products such as Hormel Fire Braised meats, Hormel Bacon 1 cooked bacon, and Rosa Grande premium pepperoni. The company continues to see momentum in the Foodservice business.

Lowered guidance

Hormel lowered its sales guidance for the full year of 2024 to reflect commodity market conditions, the production disruption at its Suffolk facility, and declines in the contract manufacturing business. It now expects net sales of $11.8-12.1 billion versus the prior outlook of $12.2-12.5 billion.

The company expects lower volumes and pricing for commodity whole turkeys to continue to put pressure on earnings. The Suffolk production disruption is also expected to impact the bottom line. In light of this, Hormel narrowed its earnings guidance for the full year. It now expects GAAP EPS to range between $1.45-1.51 versus the previous range of $1.45-1.55. Adjusted EPS is now expected to be $1.57-1.63 versus the prior outlook of $1.55-1.65.