Executive Summary

Howmet Aerospace represents a high-quality, premier supplier of mission-critical components in the aerospace and defense sectors, riding a prolonged supercycle in commercial aerospace demand and elevated global defense spending. The company has consistently demonstrated pricing power, margin resilience, and strong free cash flow generation, culminating in record fiscal year 2025 revenues of $8.3 billion. However, the market has thoroughly recognized these fundamental strengths. The stock has experienced a massive rerating, surging over 64% in the trailing twelve-month period to trade at a premium forward price-to-earnings multiple of approximately 46.33x. While the recent $1.8 billion acquisition of Consolidated Aerospace Manufacturing (CAM) from Stanley Black & Decker provides a clear runway for inorganic growth and synergies in the fastener segment.

Business Description & Recent Developments

Headquartered in Pittsburgh, Pennsylvania, Howmet Aerospace Inc. is a global leader in engineering and manufacturing advanced solutions for the aerospace and commercial transportation industries. The enterprise operates through four distinct business segments. The Engine Products segment, historically accounting for nearly half of total net revenues, manufactures investment castings, seamless rolled rings, and airfoils utilized in aircraft engines and industrial gas turbines. The Fastening Systems segment produces specialized fasteners, fluid fittings, and installation systems for military and commercial aerospace platforms. The Engineered Structures segment supplies titanium ingots, mill products, and complex structural components. Finally, the Forged Wheels segment delivers forged aluminum wheels globally under the prominent Alcoa Wheels and Dura-Bright brands, primarily serving the commercial truck and bus markets. The company operates a vast global footprint across North America, Europe, and Asia, with international operations historically contributing over half of total consolidated revenues.

In a transformative strategic move, Howmet Aerospace announced on December 22, 2025, a definitive agreement to acquire Consolidated Aerospace Manufacturing (CAM) from Stanley Black & Decker for $1.8 billion in an all-cash transaction. This acquisition is designed to significantly enhance Howmet’s portfolio of high-tech, mission-critical fastening solutions. Management anticipates the CAM unit will generate fiscal year 2026 revenues between $485 million and $495 million, alongside an adjusted EBITDA margin exceeding 20% prior to the realization of operational synergies. The transaction is projected to close in the first half of 2026, subject to standard regulatory approvals, and is expected to yield favorable federal tax treatments that will effectively reduce the adjusted EBITDA transaction multiple to approximately 13x. In addition to aggressive inorganic growth, management has maintained a steadfast commitment to shareholder returns. In the first nine months of 2025 alone, the company executed $500 million in share repurchases and raised its dividend payout. This aggressive capital return strategy culminated in a newly announced quarterly dividend of 12 cents per share, payable in late February 2026, reflecting the Board’s confidence in the company’s sustained liquidity and free cash flow generation.

Industry & Competitive Positioning

Howmet Aerospace operates within an aerospace and defense oligopoly characterized by steep barriers to entry, immense capital requirements, and rigorous regulatory certification processes. The primary catalyst driving the commercial aerospace market is an ongoing, robust recovery in wide-body aircraft demand, coupled with sustained high build rates for narrow-body airframes. Despite historical quality control disruptions and labor strikes at major original equipment manufacturers (OEMs) like Boeing, the underlying demand for fuel-efficient, next-generation aircraft remains structurally intact. Airlines are actively modernizing aging fleets to reduce carbon emissions and combat volatile aviation fuel costs, ensuring a multi-year backlog for critical suppliers like Howmet. Concurrently, the global defense landscape has shifted materially. Rising geopolitical friction has prompted the United States and allied nations to permanently elevate baseline defense appropriations. Howmet specifically benefits from robust demand for engine spares supporting the F-35 Joint Strike Fighter program, as well as legacy platforms including the F-15 and F-16.

Competitively, Howmet defends its market share through a potent combination of proprietary metallurgical science, thousands of active patents, and deep-rooted OEM relationships. The competitive landscape includes formidable entities such as Berkshire Hathaway’s Precision Castparts, ATI Inc., and international players like VSMPO and Lisi Aerospace. However, Howmet’s entrenched position in investment castings and high-temperature titanium alloys provides a distinct competitive moat. It is exceptionally difficult for OEMs to switch suppliers for critical engine components due to the lengthy and costly Federal Aviation Administration certification requirements. Conversely, the commercial transportation sector presents a cyclical drag. The industry is currently enduring a period of softness driven by lower OEM truck builds, exacerbated by macroeconomic uncertainty and tariff-related anxieties in North America. Despite this, Howmet’s overarching market positioning remains highly favorable, as the blended strength of commercial and defense aerospace significantly outweighs the cyclical troughs of the commercial transportation segment.

Historical Financial Performance

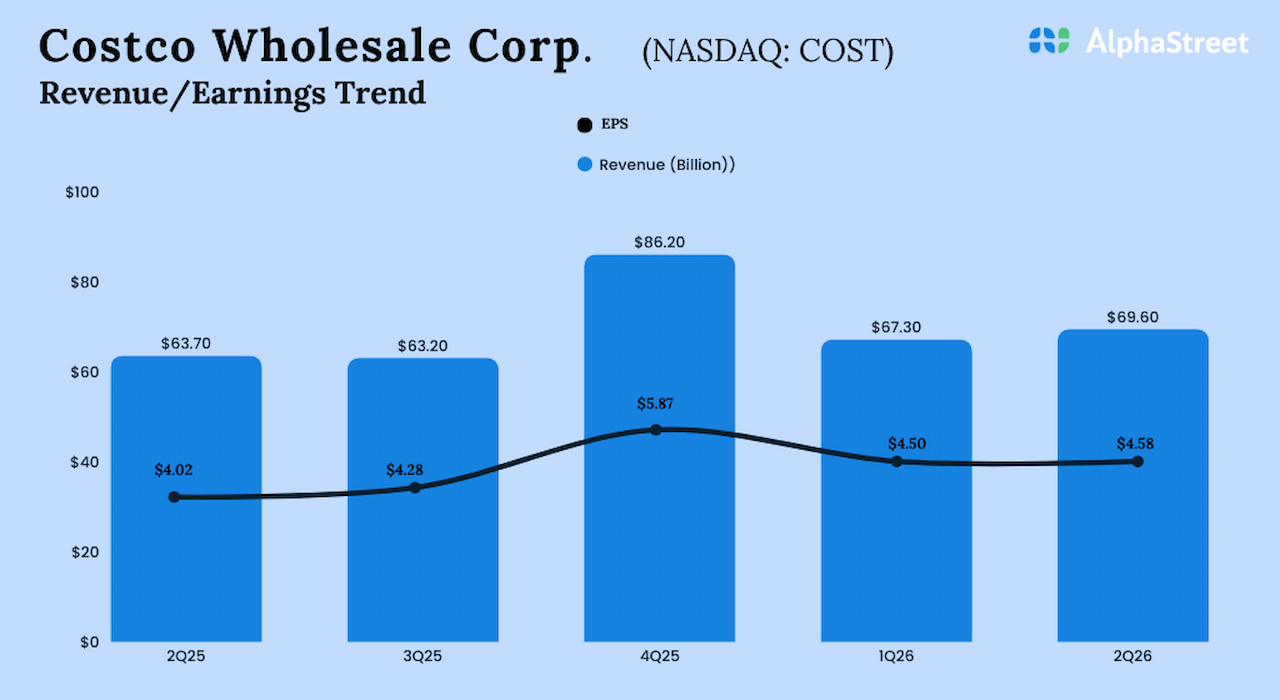

A retrospective analysis of Howmet Aerospace’s financial trajectory reveals a company consistently executing at a high operational cadence. The company recently reported stellar full-year 2025 results, decisively beating consensus estimates and marking a period of record profitability. Total revenues for fiscal 2025 reached an unprecedented $8.3 billion, representing an 11% year-over-year increase driven fundamentally by a 12% expansion in the commercial aerospace division and a 21% surge in defense aerospace. This top-line acceleration was mirrored by exceptional margin realization. The company’s adjusted EBITDA margin expanded to 29.3%, up 350 basis points from the prior year, illustrating management’s adept handling of the inflationary environment and the successful implementation of value-based pricing strategies. Adjusted earnings per share for 2025 leaped by 40% to $3.77, soundly outperforming prior analyst expectations and signaling rigorous cost control amidst rising labor and material inputs.

Cash generation has been a hallmark of Howmet’s recent financial narrative. In 2025, the enterprise generated approximately $1.9 billion in cash from operations, allowing for the aggressive deployment of capital toward shareholder remuneration and balance sheet optimization (Howmet Aerospace PR, MarketBeat; access date: 2026-02-16). The company successfully repurchased $700 million of its common stock throughout the year and paid $0.44 per share in annual dividends, completely funding these initiatives through internally generated free cash flow (Howmet Aerospace PR, TradingView SEC 10-K Summary; access date: 2026-02-16). Balance sheet fortitude remains a key asset; the company exited 2025 with $659 million in cash equivalents and a highly manageable debt profile, reflected in an interest coverage ratio exceeding 12.7 times, vastly superior to the industry average. This financial elasticity not only insulates the company against unforeseen macroeconomic shocks but also perfectly positioned the balance sheet to absorb the $1.8 billion all-cash CAM acquisition without jeopardizing investment-grade credit metrics.

Investment Thesis

The investment thesis for Howmet Aerospace is anchored in an undeniable narrative of high-quality growth, offset entirely by a restrictive valuation. The fundamental reasons to hold the stock revolve around the unprecedented visibility into future revenues provided by the global aerospace backlog. Catalysts for future upside are plentiful. The resolution of prolonged labor strikes at major airframers like Boeing will likely trigger a sharp acceleration in 737 MAX production, directly flowing through to Howmet’s Engine Products and Fastening Systems segments. Additionally, any geopolitical escalation or sustained military commitments by allied nations will further solidify the upward trajectory of the defense aerospace division, which is already experiencing 20% year-over-year revenue expansion. The successful and rapid integration of the CAM acquisition, specifically if management can realize synergies faster than the anticipated 2028 timeline, serves as another potent upside catalyst.

Conversely, the downside catalysts are equally critical for institutional investors to monitor. The stock is currently priced for absolute perfection. Any indication of slowing airline passenger traffic, perhaps triggered by a macroeconomic recession or a global health shock, would immediately compress the premium multiples the market has awarded the stock. Furthermore, the commercial transportation segment remains a notable anchor on overall performance; if the anticipated cyclical recovery in commercial truck builds fails to materialize by late 2026, it could drag down consolidated EBITDA margins.

Key Risks and Mitigants

Investing in Howmet Aerospace at current valuation levels carries an array of pronounced risks across operational, market, and macroeconomic spectrums. The foremost operational risk lies within the global aerospace supply chain. The industry remains exceptionally fragile, relying on highly specialized raw materials such as aerospace-grade titanium and specialized aluminum alloys. Disruptions in the availability of these materials, or a failure of tier-three suppliers to deliver intermediate components, could severely handicap Howmet’s ability to fulfill its backlog, leading to delayed revenue recognition and penalized OEM relationships. Management partially mitigates this risk through aggressive dual-sourcing initiatives, strategic inventory stockpiling, and the vertical integration of critical manufacturing processes.

Macroeconomic and geopolitical risks also loom large. With 50.7% of its revenues generated outside the United States, Howmet is highly exposed to foreign currency headwinds. A rapidly strengthening U.S. dollar inherently compresses the company’s profit margins upon repatriation unless the firm can execute aggressive price hikes in local foreign markets. Management utilizes standard corporate hedging programs and forward contracts to smooth currency volatility, but structural, long-term forex shifts remain a persistent threat. Geopolitically, the defense segment’s revenues are strictly tethered to the whims of legislative budget appropriations. A sudden shift in the United States political landscape resulting in aggressive fiscal austerity or defense budget sequestration would materially impair the company’s long-term growth algorithm. Finally, there is the overarching valuation risk.

Conclusion and Recommendation

In conclusion, Howmet Aerospace Inc. stands as an elite operator within the aerospace and defense supply chain, boasting unparalleled technological capabilities, a pristine balance sheet, and a management team executing flawlessly on both organic and inorganic growth vectors. The $1.8 billion acquisition of CAM will further solidify its dominance in aerospace fastening systems, while the commercial aerospace supercycle guarantees a durable multi-year revenue stream.