Earlier this week, biotech company ImmunoGen (NASDAQ: IMGN) reported mixed financial results for the first quarter of 2021, pushing the stock into the red zone. Investors were also worried about the delays in patient enrollment and certain other COVID-related impacts on the lead program, mirvetuximab soravtansine, a Phase 3 investigational drug to treat platinum-resistant ovarian cancer.

Since the announcement of the results, shares are down almost 10%, and this dip could be a good opportunity to snap up a promising oncology stock.

As you might be well aware, oncology treatment offers a tremendous market, which is estimated to grow at a compounded annual rate of around 10% to $284.5 billion over the next two years. Ovarian cancer, which is ImmunoGen’s primary focus, is among the most fatal gynecological malignancy. In 2020, approximately 14,000 women are estimated to have succumbed to this illness in the US alone. Hence, if ImmunoGen does succeed in its efforts, the upside potential is pretty vast.

ALSO READ: RESAAS: An under-the-radar technology firm with global ops and partnerships

The catch though is that oncology drugs have proved to be very difficult to develop in the first place, and hence, investing in such stocks comes with a fair amount of risk. However, mirvetuximab has a single-arm pivotal trial and randomized confirmatory trial – both in Phase 3 – with promising results so far. The drug is also being studied in combination with Avastin, which is currently in Phase 2.

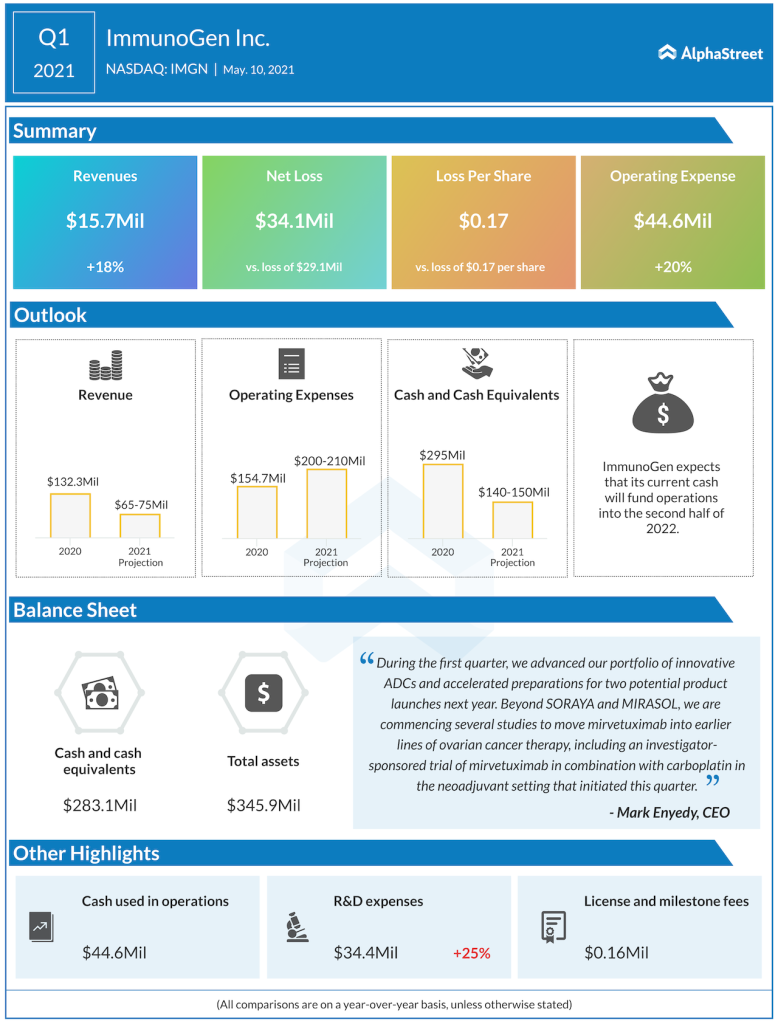

The delays have pushed the expected timing of top-line data by a quarter to Q4 of this financial year. The submission of the biologics license application (BLA) with the FDA is now expected sometime in the first quarter of 2022. Importantly, the management does not expect a significant cost impact from the delay.

ImmunoGen CFO Susan Altschuller said in an email interaction with AlphaStreet, “This was effectively a 6-week delay in patient accrual, so we do not anticipate any material impact on our expenses. Accordingly, as outlined on our call, there is no change to our guidance.”

The Waltham, Massachusetts-based firm had reaffirmed its guidance on operating expenses between $200 million and $210 million when it announced results earlier this week. The minor delay in the timelines with no cost impact offers little reason to see the kind of sell-off it witnessed post earnings. In fact, for a stock that has rallied over the trailing 12 months, the dip is possibly a window of opportunity.

ALSO READ: Trxade expects its health passport to be a key post-pandemic reopening tool

Strong pipeline, institutional backing

It may be noted that apart from mirvetuximab, ImmunoGen has a few other trials ongoing to treat other forms of cancer including acute myeloid leukemia, pancreatic, gastric, etc. Even though in the early stages, these trials continue to offer promise in the oncology department.

Another key reason to track this stock is its high institutional holding. Especially since the start of this year, there has been an increasing interest among institutional investors, who currently hold close to 90% of the shares.

Speaking about the institutional holdings, Altschuller said, “We entered this year with significant momentum and strong prospects for the business that included two product approvals next year, important near-term catalysts with our lead program, a second pivotal program with data in the first half of 2022, accelerating earlier stage portfolio, a strong cash position, and an experienced management team to deliver on the business. This profile has catalyzed investor interest that we have further cultivated through active outreach.”

The stock has a 12-month average price target of $9.13, which is at a 40% upside from Thursday’s trading price. Hence, the promising pipeline only accentuates the wealth-creation potential of the biotech firm in the long run.

(Written by Arjun Vijay)

_____

For more insights into ImmunoGen, read the latest earnings call transcript