Like many store operators, Costco Wholesale Corporation (NASDAQ: COST) benefited from the sales boom set off by the pandemic. But the warehouse giant is experiencing a slowdown now, thanks to economic uncertainties and muted consumer confidence.

This week, the company’s stronger-than-expected Q4 results failed to impress investors soon after the announcement, but the stock gained during the extended session. It seemed that initially the market was disappointed by the high wage expenses, comparable sales miss, and the management’s decision not to hike membership fees. COST, which is one of the best-performing stocks, is moving closer to its April high. The good news is that despite the high valuation, the stock is considered a good investment option due to its strong growth prospects and potential to create shareholder value.

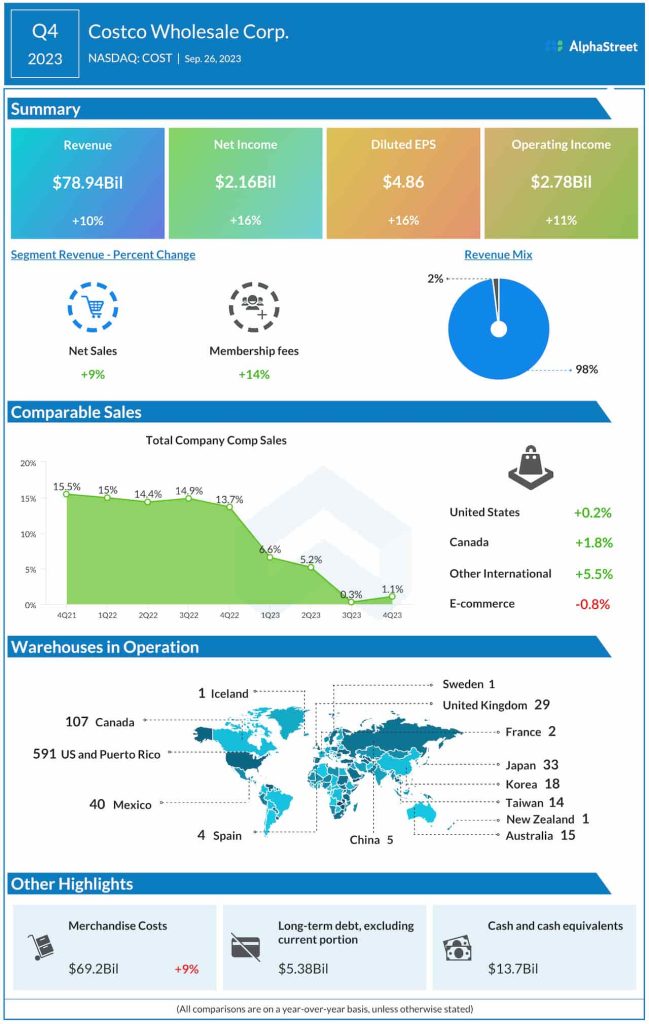

There was speculation that the company would raise subscription fees, which account for the bulk of its revenues, but there was no such move from the management. Meanwhile, membership growth continued in the latest quarter. While gross margin rose 42 basis points year-over-year, higher costs are putting pressure on profit though inflation is coming down in categories like food and consumables.

Fee Hike

A further improvement in the inflation situation would ease the strain on family budgets, setting the stage for Costco to hike membership fees towards year-end. Recent margin growth reflects fewer markdowns due to an improvement in the inventory position. Underscoring its resilience to inflation and macro headwinds, the company opened nine net new warehouses in the fourth quarter and ended the year with 23 net new units. Costco is planning to continue expanding in the US and overseas markets over the next decade.

Commenting on the Q4 outcome, Costco’s CFO Richard Galanti said, “Overall, for the fiscal fourth quarter, food and sundries were relatively strong once again, with fresh foods right behind and with some offsets on some of the non-food categories. In terms of Q4 comp sales metrics, traffic or shopping frequency increased 5.2% worldwide and 5% in the United States. Our average transaction or ticket was down 3.9% worldwide and down 4.5% in the U.S., impacted in large part from weakness in bigger ticket non-food discretionary items, as well as the gas price deflation.”

Comps Miss

At $4.86 per share, fourth-quarter earnings were up 16% year-over-year and above estimates. That reflects a 10% growth in revenues to $78.9 billion. Both numbers topped expectations, after missing in the last quarter. Comparable sales edged up 1.1%, marking a sequential improvement from the third quarter when comps declined. However, the number missed expectations. eCommerce sales dropped at a significantly slower pace. Merchandise costs were up 9%. The company ended the fiscal year with 71.0 million paid household members, which is up 8%.

Costco’s shares reversed a part of their post-earnings gains and opened lower on Wednesday, but regained strength later and closed the session up 2%.