PayPal Holdings Inc. (NASDAQ: PYPL) reported stronger-than-expected results for the third quarter. That gave a much-needed boost to the stock which has been languishing at multi-year lows since retreating from the 2021 peak. PayPal is a dominant player in the payments industry, delivering stable revenue and earnings performance over the years. But growth has slowed since the pandemic-era boom waned, and the stock is struggling to regain strength.

Stock Dips

For PYPL, 2023 has been a challenging year so far as it continued to lose momentum and mostly traded below the long-term average. On the positive side, the stock has become more affordable but the ongoing macro uncertainties and squeeze on consumer spending will be a concern for prospective investors. The market responded positively when PayPal’s new CEO Alex Chriss last week revealed plans to align the company’s resources to its most profitable growth priorities and to become leaner, more efficient, and more effective. Market watchers, in general, are bullish on the stock’s long-term prospects and predict double-digit gains.

As far as growth is concerned, one of the main challenges facing the company is competition. The market has changed significantly since PayPal separated from eBay about eight years ago, and now consumers have other options like Apple Pay that offer a fast and easy checkout experience. The payment systems of Amazon and Google keep gaining traction — that doesn’t bode well for PayPal which is highly dependent on e-commerce to generate revenue. It is worth noting that the termination of PayPal’s operating agreement with eBay a few years ago has been a drag on its growth.

Outlook

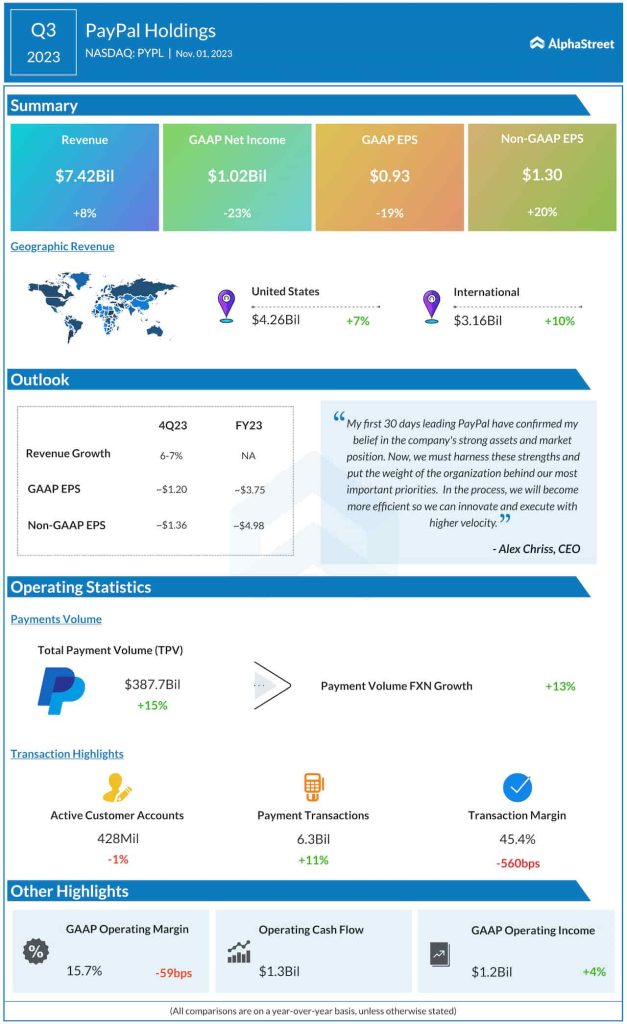

Revitalizing the business will depend a lot on how Alex Chriss executes the growth plan. In a sign that the management’s cost-cutting efforts are paying off, full-year earnings guidance has been raised from $4.95 per share to $4.98 per share, which is above estimates. Meanwhile, the cautious margin forecast is likely to add to concerns over the company’s low-margin business which is getting bigger compared to the branded segment.

During his first earnings call after taking the helm at PayPal a few weeks ago, Chriss said, “My focus is to clearly define our mission, vision, and purpose and unleash this team to execute a clearly defined and durable strategy. We will establish and refocus systems and processes to galvanize the entire organization behind our purpose and growth outcomes. On our customers and innovation, I generally see our customers falling into three categories: consumers, small businesses, and large enterprises.”

Strong Q3

In the third quarter, PayPal’s adjusted earnings came in at $1.30 per share, compared to $1.08 per share in the year-ago quarter. On a reported basis, net profit was $1.02 billion or $0.93 per share in Q3, vs. $1.33 billion or $1.15 per share last year. Revenues came in at $7.42 billion, compared to $6.85 billion in the corresponding period of 2022. Both profit and revenues topped expectations, continuing the long-term trend. For the fourth quarter, the company expects revenues to grow in the range of 6% to 7%.

After falling a dismal 27% so far this year, PayPal’s stock ended Monday’s session down 2.6%, which is far below the record highs of 2021.