AlphaStreet Newsdesk powered by AlphaStreet Intelligence

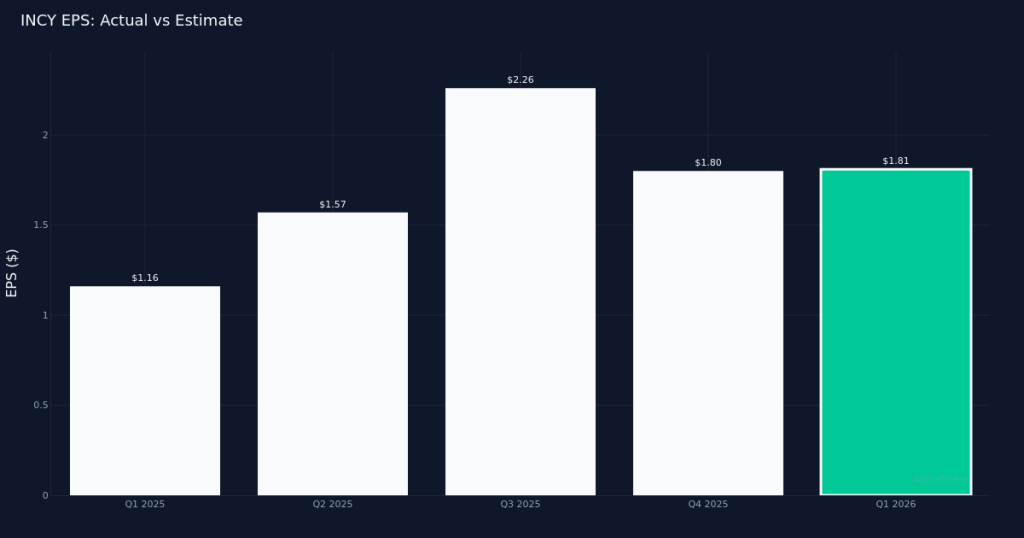

Strong Beat. Incyte Corporation (NASDAQ:INCY) delivered a robust Q1 2026 performance, posting Non-GAAP diluted EPS of $1.81 that topped Wall Street’s estimate. The biotechnology company generated $1.27B in revenue for the quarter, marking a 21.0% increase from $1.05B in Q1 2025. The company earned net income during the period, underscoring the strength of its commercial execution and expanding product portfolio.

Revenue-Driven Growth. The quality of this earnings beat appears particularly solid, driven by robust top-line expansion rather than mere cost optimization. Total net sales reached $1.10B for the quarter, reflecting strong commercial momentum across Incyte’s hematology and oncology franchises. This acceleration in revenue growth demonstrates the company’s ability to capture market share in competitive therapeutic areas while successfully launching newer products alongside its established blockbuster franchise.

Jakafi Maintains Momentum. The company’s flagship product Jakafi continued its steady performance, generating revenue with a 7.0% year-over-year increase. This sustained growth from a mature asset highlights the durability of Incyte’s core franchise in myelofibrosis and polycythemia vera, markets where the company has maintained its leadership position despite emerging competition. The single-digit growth trajectory suggests Jakafi remains a reliable cash generator to fund pipeline development and business development activities.

Market Reception. Shares of INCY traded at $95.72, up 1.1% following the earnings release, a relatively muted response given the magnitude of the EPS beat. The modest stock reaction may reflect investors taking profits after a strong run or waiting for additional catalysts from the company’s clinical pipeline. Wall Street consensus currently stands at buy ratings, hold ratings, and sell rating, suggesting a cautious stance from the analyst community despite the strong quarterly performance.

Diversification Imperative. While Jakafi’s continued strength provides financial stability, the product still represents a substantial portion of the company’s revenue base. The 21.0% overall revenue growth significantly outpacing Jakafi’s 7.0% increase indicates meaningful contributions from other products in the portfolio, a positive sign for those concerned about concentration risk. This diversification trajectory will be critical as the company navigates patent cliffs and competition in its core markets over the coming years.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.