Innospec Inc. (NASDAQ: IOSP) announced Q4 2025 earnings on February 17, 2026. Results revealed operational momentum across key segments. So, the company delivered improved cash generation. Also, profitability gains offset revenue headwinds.

Key Financial Results

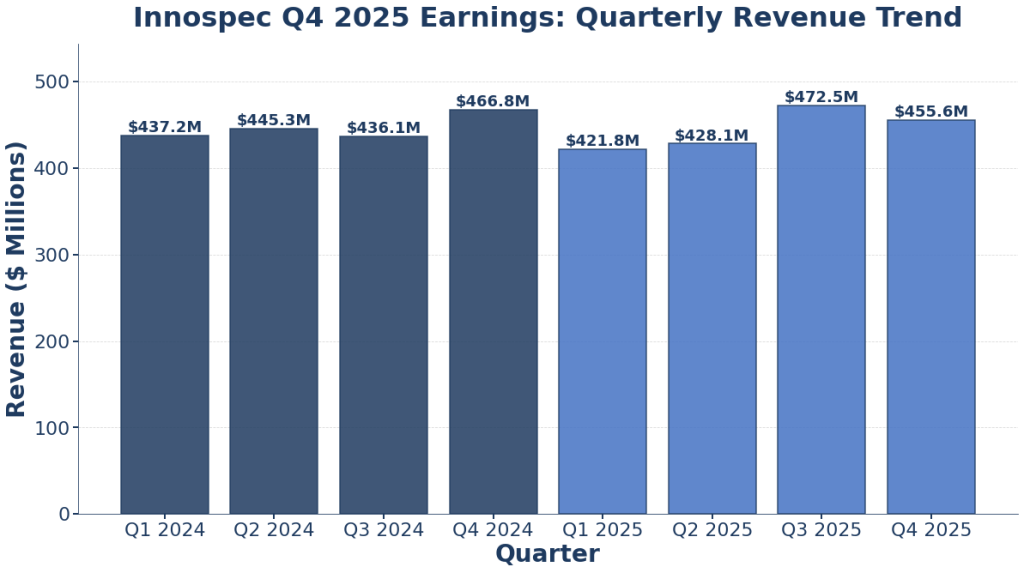

Quarterly revenue totaled $455.6 million, but this compared with $466.8 million in Q4 2024. The decline of 2% reflected mixed segment performance. So, net income reached $47.4 million versus $70.4 million lost last year. The prior year loss included $116.7 million from the pension scheme buyout. Plus, adjusted EBITDA was $55.7 million. Yet this was down 2% from $56.6 million. In fact, operating cash flow of $61.4 million remained robust. Also, Innospec generated solid cash returns. Now, net cash improved to $292.5 million. This strengthens the company’s financial position.

Full Year Performance

Full-year 2025 revenues declined 4% to $1.778 billion from $1.845 billion. Plus, net income surged to $116.6 million. This compared with $35.6 million in 2024. So, adjusted EBITDA totaled $203.0 million. Yet this was down 10% from $225.2 million. This decline reflected lower activity in oilfield services. Also, operating cash flow declined to $138.3 million from $184.5 million. Still, the company maintained solid liquidity. In fact, net cash totaled $292.5 million, up from $289.2 million. Thus, the financial foundation remains solid.

Quarterly Trend Analysis

Innospec Q4 2025 earnings quarterly revenue trend reveals variations. Q4 2025 revenue of $455.6 million trailed Q4 2024’s $466.8 million. But the company maintained solid operational execution. Also, segment dynamics created mixed results across the portfolio. Overall, the revenue trajectory reflects end-market normalization.

Segment Performance

Performance Chemicals revenue stayed constant at $168.4 million. Volume declines of 7% offset price gains of 3%. Plus, currency helped by 4%. So, operating income declined 14% to $17.7 million. Gross margin compressed by 460 basis points to 18.1%. Still, management initiated margin recovery actions. In fact, sequential improvement emerged in Q4. Also, the segment anticipates further gains in 2026. Meanwhile, operational discipline is yielding positive results. Thus, the path forward looks promising.

Fuel Specialties delivered the best output. Revenue rose 1% to $194.1 million. Volume gains of 8% offset price/mix headwinds of 10%. Plus, currency provided 3% support. So, operating income surged 7% to $37.2 million. Gross margin improved to 34.7%. In fact, this segment leads in margins and returns. Management anticipates consistent results in 2026. Thus, this division remains the portfolio anchor. Therefore, Fuel Specialties provides reliable earnings.

Oilfield Services revenue declined 12% to $93.1 million. Lower US completions and Middle East activity drove the decline. Plus, operating income rose 9% to $8.2 million. Margin gains of 180 basis points reflected operational discipline. Sales mix improved. So, management anticipates recovery as Middle East activity resumes. The recent DRA expansion will boost capacity. Meanwhile, cost controls are enabling margin expansion.

Balance Sheet and Cash Flow

The balance sheet remains solid with $292.5 million in net cash. Operating cash generation totaled $61.4 million in Q4. Capital expenditures of $20.5 million remain disciplined. So, the company generated $40.9 million in free cash after capex. Management paid a semi-annual dividend of $21.6 million. This represented a 10% increase versus the prior year. In fact, the net cash position provides significant flexibility. Plus, Innospec can pursue M&A, increase buybacks, or grow dividends. Meanwhile, the robust cash position supports growth investment. Therefore, shareholders benefit from operational discipline.

2026 Outlook

Management outlined a constructive 2026 outlook. Performance Chemicals will pursue margin recovery through operational improvements. New product launches accelerate across all end markets. Cost reduction actions will continue driving overhead efficiency. So, Fuel Specialties will deliver consistent results. The segment anticipates steady volume and pricing. Also, Oilfield Services anticipates recovery as Middle East activity rebounds. The DRA expansion provides new capacity. Mexico sales are not assumed in the outlook. Subsequently, management targets continued operating income growth. Overall, the strategic plan addresses multiple growth vectors.

Key Takeaways

Innospec’s Q4 results demonstrate operational progress. Margin enhancement initiatives are gaining momentum. The Fuel Specialties segment continues to deliver reliable results. Cash flow generation remains solid. So, the $292.5 million net cash position enables strategic flexibility. Management’s balanced approach protects shareholder interests. Near-term headwinds in some segments appear manageable. In fact, the transformation focusing on margin and returns shows promise. Therefore, investors should monitor 2026 execution closely. Meanwhile, the company’s strategic positioning justifies close observation. Additionally, shareholder value creation remains on track.