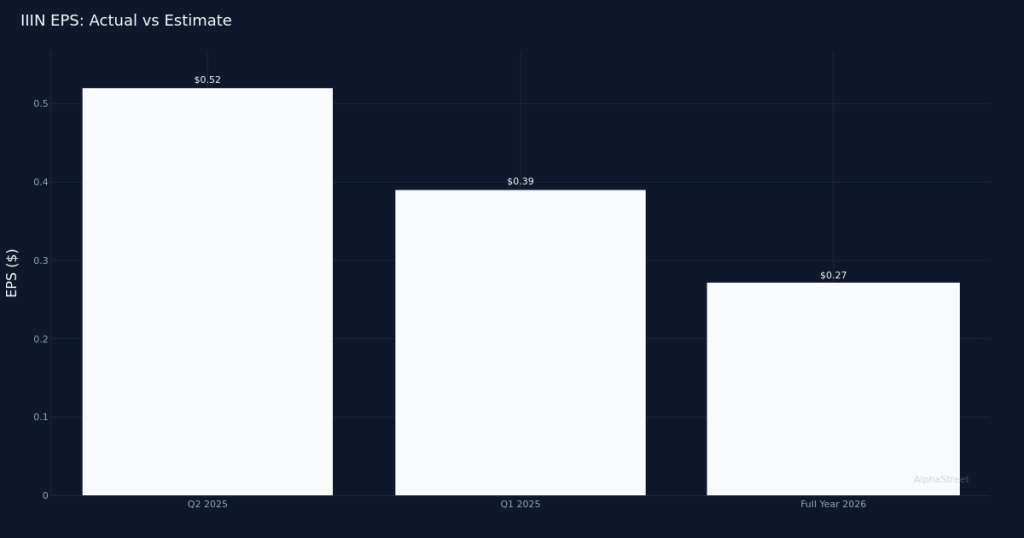

Mixed quarter. Insteel Industries Inc. (IIIN) reported Q2 2026 diluted earnings of $0.27 per share on revenue of $172.7M, delivering a top-line expansion that masked deteriorating profitability in the metal fabrication specialist’s core business. The company posted bottom-line profit of $5.2M for the quarter, as shares retreated in response to the weaker-than-expected margin profile despite the revenue gain.

Revenue growth misleads. While revenue climbed 7.5% year-over-year from the $160.7M recorded in Q2 2025, the headline figure obscures operational weakness beneath the surface. Shipments declined 5.9% for the quarter, indicating the revenue increase was driven by pricing rather than volume momentum—a less sustainable growth driver in cyclical fabrication markets. This disconnect between pricing power and actual demand raises questions about the durability of the current trajectory, particularly as construction and infrastructure end-markets show signs of softening.

Profitability compression accelerates. The earnings picture deteriorated sharply, with EPS plunging 48.1% from the $0.52 posted in Q2 2025. This dramatic margin contraction suggests cost pressures are overwhelming pricing gains, a concerning dynamic for a manufacturer operating in a capital-intensive industry. The company maintained a cash balance of $15.1M at quarter end, providing some financial cushion but offering limited room for error if operating conditions continue to weaken. The magnitude of the profit decline relative to the modest revenue gain points to unfavorable operating leverage and potential inefficiencies in the production footprint.

Street turns cautious. Wall Street consensus reflects growing skepticism, with analyst coverage standing at 0 buy ratings, 3 hold ratings, and 1 sell rating—a decidedly defensive positioning that suggests the institutional community sees limited upside from current levels. The absence of any buy recommendations is particularly notable for a company trading in the mid-$30s, indicating concerns extend beyond the current quarter’s results to broader structural challenges in the business model. The stock’s negative reaction appears warranted given the earnings miss and volume contraction.

Volume trajectory critical. The most concerning aspect of this quarter remains the negative shipment trend, which threatens to undermine even the pricing gains that propped up revenue. For a metal fabricator serving construction and industrial markets, volume declines typically precede pricing pressure as competitors chase scarce orders, setting up potential for accelerated margin erosion in coming quarters.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.