Intel Corporation (NASDAQ: INTC) is working to regain dominance in the semiconductor market, while evolving from an integrated chipmaker into a global foundry player. The turnaround plan involves massive capital investments to reinvent its foundry business. After years of losing market share and falling behind in manufacturing technology, 2026 marks a pivotal year for the company as key technological and operational milestones are expected to converge.

Stock Rallies

In the latter half of 2025, Intel’s stock bounced back from a slump that lasted for several months. Last week, the shares gained further momentum and entered 2026 on a positive note. Notably, the value more than doubled last year after staying near multi-year lows for an extended period. The recovery reflects investors’ confidence in the turnaround strategy — the company has been widely considered a laggard in the industry due to competitive and strategic challenges.

Last year, INTC was one of the best-performing tech stocks, but its value remains below most industry peers. It appears that stakeholders turned optimistic about Intel’s prospects after the appointment of Lip-Bu Tan as the new CEO, succeeding Pat Gelsinger who made an abrupt exit after a failed turnaround program. Overall, the company now looks better positioned to leverage emerging opportunities in the semiconductor market, such as the booming demand for AI chips. Recent funding from the US government, Softbank, and Nvidia is expected to catalyse the turnaround.

Recovery

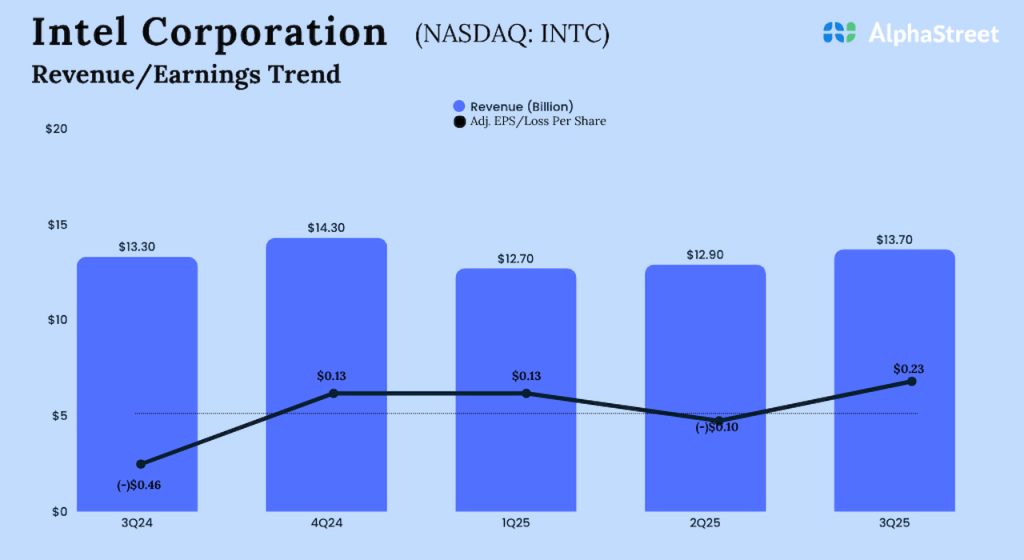

In the third quarter of FY25, Intel’s revenue increased 3% year-over-year to $13.65 billion. Client Computing revenue rose 5%, while Data Center and AI revenue declined 1%. Adjusted earnings were $0.23 per share in the September quarter, excluding special items, compared to a loss of $0.46 per share in the year-ago quarter. Earnings beat estimates. On a reported basis, net income came in at $4.06 billion or $0.90 per share in Q3, compared to a loss of $16.6 billion or $3.88 per share last year. The fourth-quarter report is scheduled for release on January 26, after the closing bell.

Lip-Bu Tan said in his post-earnings interaction with analysts, “As we look ahead, my focus remains firmly on the long-term opportunity across every market we serve today and those we will enter tomorrow. Our strategy is crystallized around our unique strengths and value proposition, supported by the accelerating and unprecedented demand for compute in the AI-driven economy. Our leadership continues to strengthen. Our culture is becoming more accountable, collaborative, and execution-oriented. And my confidence in the future grows stronger every day.“

Fab Power

The company bets big on its fab business, offering a full-stack solution that spans chip design through advanced assembly and testing. Intel Foundry is positioned as an alternative to Taiwan Semiconductor Manufacturing Company, the semiconductor giant that dominates the market. As fabrication plants increase production and start running in full capacity, the foundry business should turn profitable — it incurred an operating loss of more than $2 billion in the most recent quarter.

Intel’s shares opened higher on Monday and traded near the $40 mark mostly during the session. The average stock price for the last 52 weeks is $26.36.