AlphaStreet Newsdesk powered by AlphaStreet Intelligence

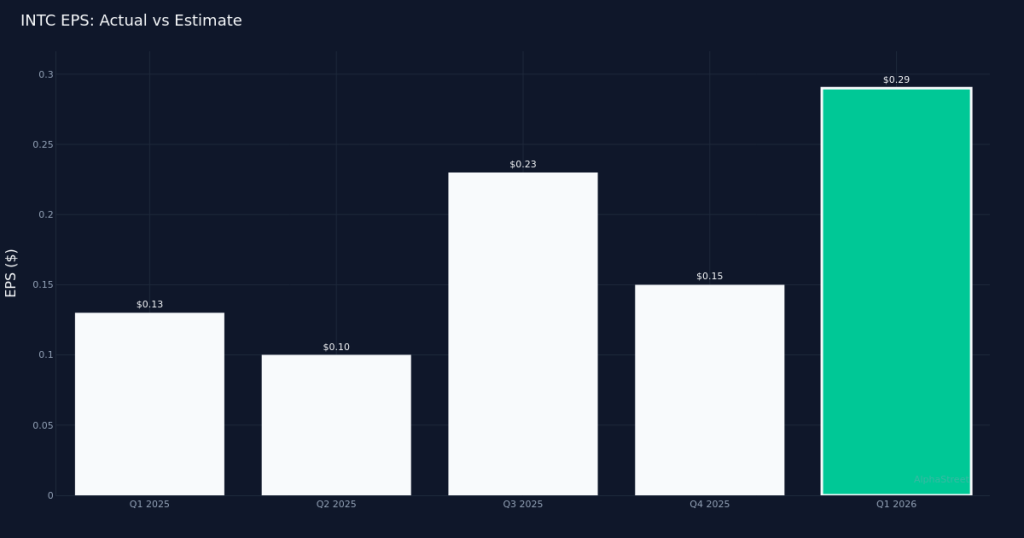

Massive Beat. Intel Corporation (NASDAQ:INTC) crushed expectations in Q1 2026, delivering non-GAAP earnings of $0.29 per share against analysts’ $0.01 forecast—a beat by 2800.0% that signals a dramatic turnaround for the semiconductor giant. Revenue totaled $13.58B for the quarter, up 7.0% from $12.67B in Q1 2025, as the company’s restructuring efforts and product portfolio realignment appear to be gaining traction. The stock surged 2.3% to $66.78 on the results, reflecting investor enthusiasm for the company’s execution.

Profitability Inflection. The company’s return to meaningful profitability stands as the quarter’s defining achievement, with net income of $1.49B demonstrating operational leverage that many analysts had doubted Intel could achieve in this timeframe. The 7.0% revenue growth, while modest compared to some semiconductor peers, represents a critical stabilization after years of market share erosion and manufacturing challenges. This combination of top-line expansion and bottom-line strength suggests the earnings beat reflects genuine operational improvement rather than purely financial engineering.

CCG Drives Performance. Client Computing Group (CCG) generated $7.73B in revenue for the quarter, anchoring Intel’s results as PC market conditions show signs of stabilization. The segment’s performance indicates that Intel’s core x86 franchise retains significant customer loyalty despite competitive pressures from AMD and the broader shift toward ARM-based architectures in certain applications. The company’s workforce stood at 83,200 total employees at quarter end, reflecting the completion of substantial restructuring initiatives announced in prior periods.

Conservative Guidance. Management projected Q2 2026 EPS (adjusted) in the $0.20 to $0.20 range, representing sequential deceleration from Q1’s $0.29 but still well above the trough levels of recent quarters. For the next quarter, the company expects revenue of $13.80B to $14.80B, suggesting continued sequential momentum with a notably wide range that likely reflects uncertainty around enterprise refresh cycles and AI accelerator demand. The midpoint of this guidance implies continued year-over-year growth, though the substantial range suggests management remains cautious about visibility.

Analyst Skepticism Persists. Despite the impressive quarter, Wall Street consensus stands at 9 buy, 35 hold, and 3 sell ratings, revealing that most analysts maintain a wait-and-see posture on Intel’s multi-year transformation. The hold-heavy rating distribution suggests that while near-term execution has improved, concerns about Intel’s competitive positioning in next-generation manufacturing nodes and AI accelerator markets continue to temper enthusiasm. The 2.3% stock gain, while positive, appears measured given the magnitude of the earnings surprise.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.