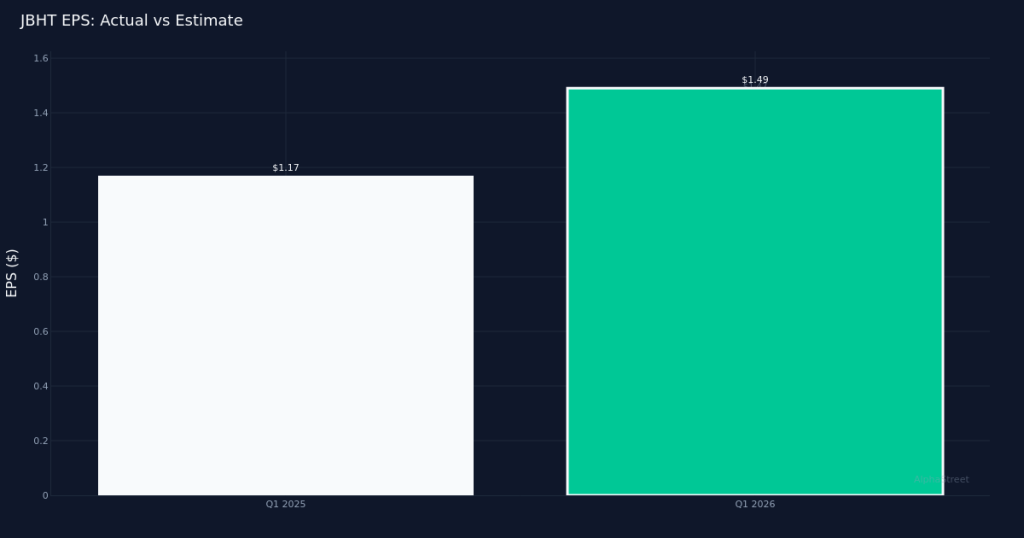

J.B. Hunt delivered a modest earnings beat in Q1 2026, but the market’s negative reaction signals investor concerns about the quality and sustainability of the company’s recovery. The integrated freight and logistics provider reported GAAP EPS of $1.49, exceeding the $1.47 consensus estimate by 1.4%, while revenue of $3.06B grew 5.0% year-over-year. Despite the headline beat, shares declined after the report, suggesting investors are looking past the near-term outperformance to structural challenges in key business lines.

The earnings quality story reveals a company making meaningful progress on margin expansion, though from a depressed base. Net margin expanded to 4.6% from 4.0% in the year-ago quarter, a 0.6 percentage point improvement that translated to net income of $141.6M compared to $117.7M in Q1 2025. This margin expansion is particularly notable given the modest revenue growth rate, indicating operational discipline is taking hold. Operating margin reached 6.8% with operating income of $207.0M, while the company generated robust free cash flow of $282.3M from operating cash flow of $353.0M. Management highlighted the efficiency gains, noting “In the first quarter, we continued to make additional progress, eliminating over $30 million during the quarter.” The EPS surge of 27.4% year-over-year significantly outpaced revenue growth of 4.8%, confirming that margin improvement rather than top-line acceleration drove the bottom-line beat.

Revenue momentum remains tepid, with growth barely eclipsing mid-single digits despite comparisons against a weak 2025. The $3.06B in quarterly revenue represents improvement from the $2.92B generated in Q1 2025, but the 5.0% year-over-year growth rate underscores the challenge J.B. Hunt faces in reigniting top-line expansion. The company is operating under a known headwind, with management previously disclosing “an expected $90 million revenue headwind this year from some lost business.” At a quarterly run rate of approximately $30 million, management confirmed “we’re sort of running at a pace north of $30 million a quarter” in lost revenue. This structural drag means organic growth in retained business must significantly exceed reported growth just to maintain current levels.

Segment dynamics reveal uneven performance, with Integrated Capacity Solutions providing the only meaningful growth offset. The ICS segment generated $322.7M with 20.0% growth, serving as the company’s primary growth engine and validating J.B. Hunt’s strategic push into brokerage and capacity management. However, this segment represents less than 11% of total revenue, limiting its ability to move the needle company-wide. The core Intermodal segment, at $1.50B, grew just 2.0%, with load volumes of 536,852 units suggesting pricing rather than volume drove the modest increase. Management acknowledged weather impacts early in the quarter, noting “I’m guessing that January, February had some impact on the year-over-year volume, but up 8% in March is pretty strong,” which implies volumes were negative in the first two months before the March rebound. Dedicated Contract Services posted $840.6M with identical 2.0% growth, reflecting stable but uninspiring demand from contracted customers.

The capital allocation framework suggests management is balancing growth reinvestment with shareholder concerns about returns. Management reiterated “our guidance of a $600 million to $800 million net capex plan for the year,” which against trailing free cash flow of $282.3M in just the first quarter suggests the company expects to fund growth internally while maintaining capacity for potential shareholder returns. The capex guidance implies management believes equipment and infrastructure investments remain necessary despite the tepid volume environment, betting on market share gains or modal shift tailwinds that haven’t yet materialized in the revenue numbers.

The stock’s negative reaction despite an earnings beat reflects investor skepticism about the trajectory implied by segment trends. The market appears focused on the deceleration risks embedded in the single-digit Intermodal and Dedicated growth rates rather than celebrating the margin expansion story. The divergence between EPS growth of 27.4% and revenue growth of 4.8% creates sustainability questions: margins cannot expand indefinitely, and durable outperformance requires top-line reacceleration. With 94,299,000 shares outstanding, the company’s market capitalization implies investors are pricing in continued earnings growth challenges as easy cost cuts get exhausted.

The March volume inflection in Intermodal provides a potential narrative shift, but one quarter doesn’t establish a trend. Management’s observation that volumes accelerated 8% in March after weak January and February performance could signal either seasonal normalization or genuine demand improvement. The distinction matters: if freight demand is genuinely improving industry-wide, J.B. Hunt’s operational leverage should drive margin expansion beyond what cost cuts alone can deliver. If March was merely a seasonal bounce, the company faces ongoing pressure to defend margins while competing for market share in a stagnant volume environment.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.