Shares of The J.M. Smucker Co. (NYSE: SJM) dipped over 1% on Monday. The stock has dropped 13% over the past 12 months. The branded foods seller is operating in an environment marked by pressures on consumer spending, and input inflation. Against this backdrop, the company is focusing its resources on the brands where it sees the largest opportunities for growth.

Priority brands

J.M. Smucker continues to see strong performances from a number of brands across its segments. These include the Uncrustables, Café Bustelo, Meow Mix, Milk-Bone, and Hostess brands. These brands continue to deliver sales growth and the company sees significant opportunity for further expansion, which has led it to prioritize its investments in them.

In the second quarter of 2026, net sales for the Uncrustables brand grew 4%. Sales were up 7% at the total Company level. SJM has been focusing on product innovation and distribution gains. It launched two new flavors with higher protein, which broadens the brand’s offerings to breakfast items while also catering to the health needs of a section of customers. The company also continues to roll out limited-edition flavors to provide variety for customers.

In terms of distribution, SJM is progressing well in its expansion into convenience stores, with sales for Uncrustables nearly tripling over the past year. The convenience channel provides the brand with benefits such as availability and immediate consumption.

Uncrustables continues to gain new buyers and with a household penetration of only 25%, it has substantial room for growth. The brand remains on track to generate over $1 billion in net sales by the end of fiscal year 2026.

The Café Bustelo brand saw sales grow by 41% in Q2, driven by gains from distribution and marketing. The brand’s new offerings are seeing positive results and SJM sees significant opportunity for increases in household penetration. The company anticipates another year of double-digit sales growth for the brand.

In the Pet segment, the Meow-Mix brand continued its momentum while the Milk-Bone brand saw a sequential pickup in sales. These brands are expected to benefit from the pet humanization trend, product innovation, and seasonal and premium offerings. The dog snacks seasonal business was up double-digits versus the previous year, and the company continues to roll out new flavors in this category. SJM expects its seasonal business to double over the long term.

J.M. Smucker is seeing strong growth in the dry cat food category, helped by distribution gains, product innovation, and marketing, and it sees meaningful opportunity for growth in the wet cat food and treats categories as well.

For the Hostess brand, SJM is working on stabilizing and positioning the brand for growth by simplifying its offerings and prioritizing high-velocity and margin-accretive SKUs to drive gains. It is also working on reducing costs and improving marketing to drive growth for this brand.

Q2 performance

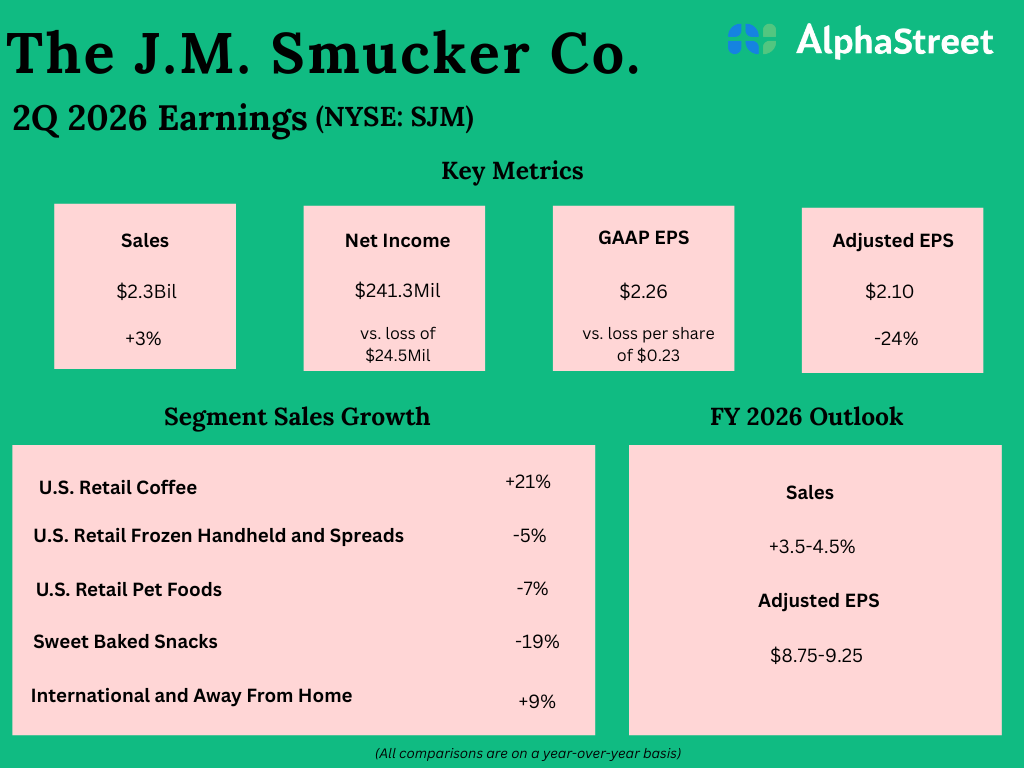

In Q2 2026, J.M. Smucker saw net sales grow 3% year-over-year to $2.3 billion. Comparable sales were up 5%. Adjusted earnings per share decreased 24% to $2.10 versus the previous year.

Outlook

For fiscal year 2026, SJM expects net sales to increase 3.5-4.5% and comparable sales to increase 5-6% versus the previous year. Adjusted EPS is expected to range between $8.75-9.25.