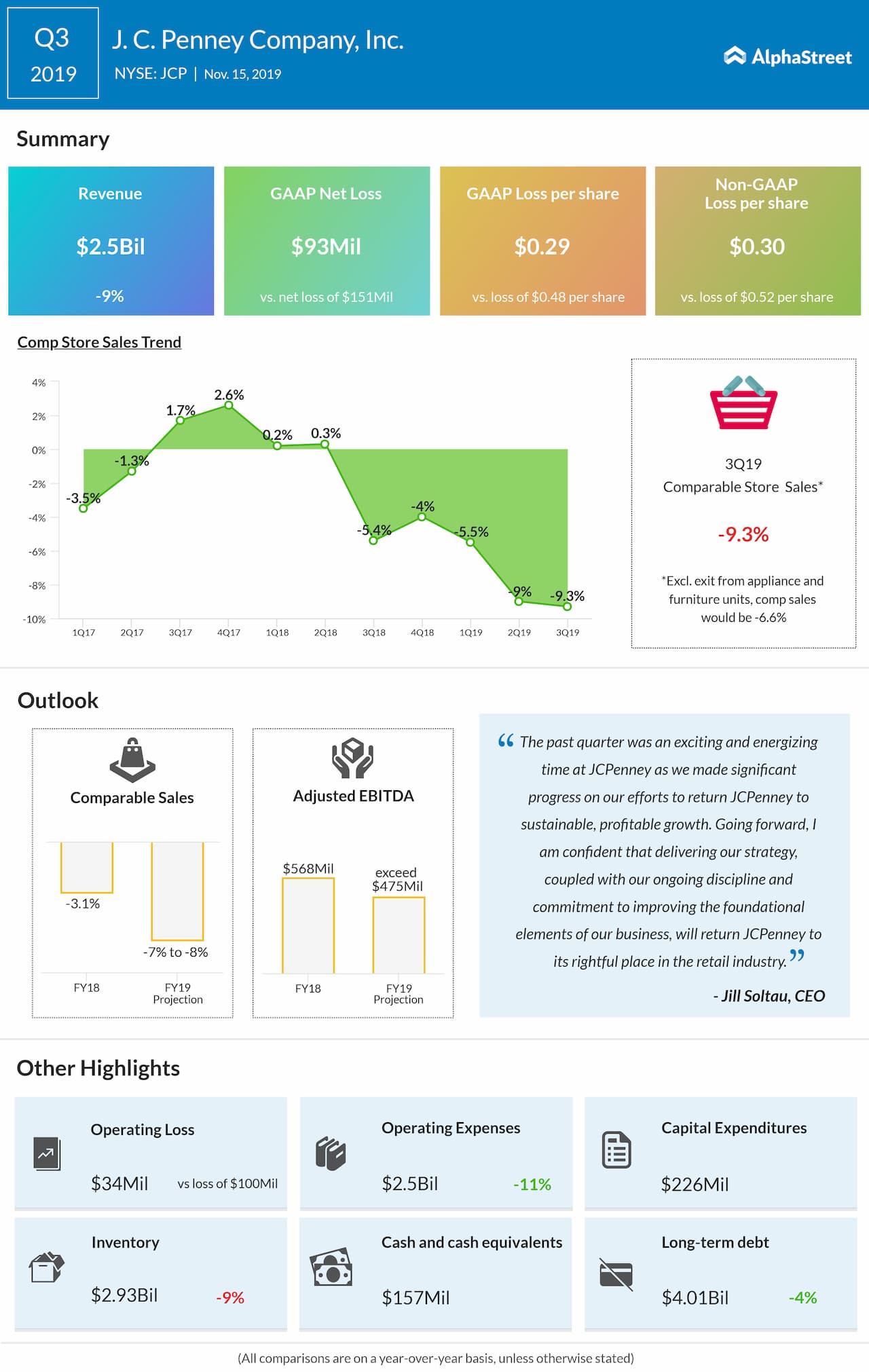

J. C. Penney Company Inc. (NYSE: JCP) reported a narrower loss in the third quarter of 2019 due to lower costs and expenses. The bottom line was narrower than the analysts’ expectations while the top line missed consensus estimates. Further, the company reaffirmed its comparable-store sales outlook for fiscal 2019.

Net loss was $93 million or $0.29 per share compared to a loss of $151 million or $0.48 per share in the previous year quarter. Adjusted loss per share narrowed to $0.30 from $0.52 a year ago.

Net sales dropped by 10.1% to $2.38 billion as comparable sales plunged by 9.3%. Excluding the impact of an exit from the major appliance and in-store furniture categories, comparable sales decreased by 6.6%.

Looking ahead into fiscal 2019, the company still expects comparable store sales to decline 7-8% and adjusted comparable store sales to fall 5-6%. Adjusted EBITDA is now expected to exceed $475 million compared to the previous range of $440 million to $475 million. The company reiterated its projection of positive free cash flow for the fiscal year 2019.

For the third quarter, the cost of goods sold improved by 350 basis points as a rate of sales driven by an increase in both store and online selling margins, improved shrink as a percent of net sales and the exit from the major appliance and in-store furniture categories earlier this year.

SG&A expenses declined by 3% primarily due to lower advertising and store controllable expenses, which were offset by slightly higher incentive compensation. Last year, the company recorded a benefit related to the buyout of a store leasehold interest.

The company ended the third quarter with liquidity of about $1.7 billion. The company expects liquidity to be at least $1.5 billion for the remainder of the year.