AlphaStreet Newsdesk powered by AlphaStreet Intelligence

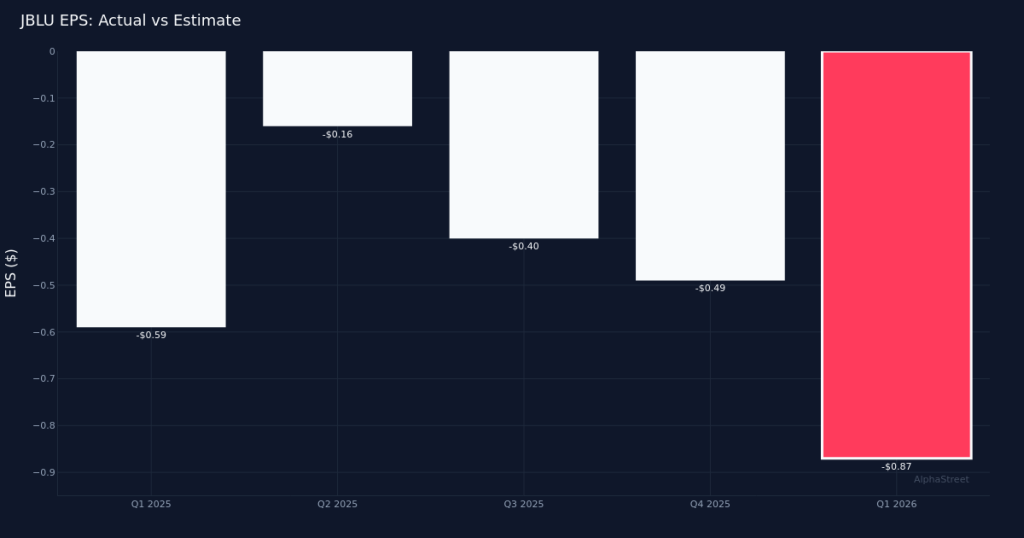

Wider Loss. JetBlue Airways Corporation (NASDAQ:JBLU) posted a disappointing Q1 2026 performance, reporting an adjusted loss of $0.87 per share excluding special items and gain on investments, missing analyst expectations of a $0.72 loss by 20.8%. The carrier generated $2.24B in revenue for the quarter, representing a 4.7% increase from $2.14B in the prior-year period. The bottom line showed an adjusted net loss of $322.0M as the airline continued to grapple with operational challenges and competitive pressures in its core markets.

Revenue Growth Insufficient. While top-line growth of 4.7% year-over-year demonstrates some demand resilience, the revenue increase failed to translate into improved profitability, suggesting significant margin compression during the quarter. The airline carried 9,330,000 revenue passengers during Q1 2026, though this passenger volume was insufficient to offset elevated cost pressures. With 289 average operating aircraft at quarter end, JetBlue’s utilization metrics appear strained as the carrier navigates a challenging competitive landscape characterized by industry-wide capacity additions and persistent cost inflation in labor and fuel categories.

Market Reaction Negative. The stock declined following the results announcement, reflecting investor disappointment with both the magnitude of the miss and the implied trajectory of the airline’s turnaround efforts. The sell-off underscores broader skepticism around JetBlue’s ability to return to profitability in the near term, particularly as the carrier operates without the scale advantages of legacy competitors or the cost structure of ultra-low-cost rivals. Wall Street sentiment remains decidedly bearish, with analyst consensus standing at 0 buy ratings, 16 hold ratings, and 5 sell ratings—a distribution that signals limited confidence in a near-term recovery.

Structural Challenges Persist. The wider-than-expected loss highlights fundamental challenges in JetBlue’s business model as the carrier attempts to differentiate its premium service offering while maintaining competitive pricing. The 20.8% miss versus consensus suggests either deteriorating unit economics or unexpected cost headwinds that management failed to adequately signal in prior guidance. Without meaningful improvement in load factors, yield management, or cost discipline, the path to sustainable profitability remains unclear for a carrier caught between service-oriented legacy airlines and aggressive low-cost competitors.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.