Shares of JetBlue Airways Corp. (NASDAQ: JBLU) turned red despite the company posting better-than-expected results for the third quarter of 2021. Revenue beat estimates while adjusted loss per share was narrower than expectations. The airline expects revenue to gain traction going into the holiday season.

Quarterly performance

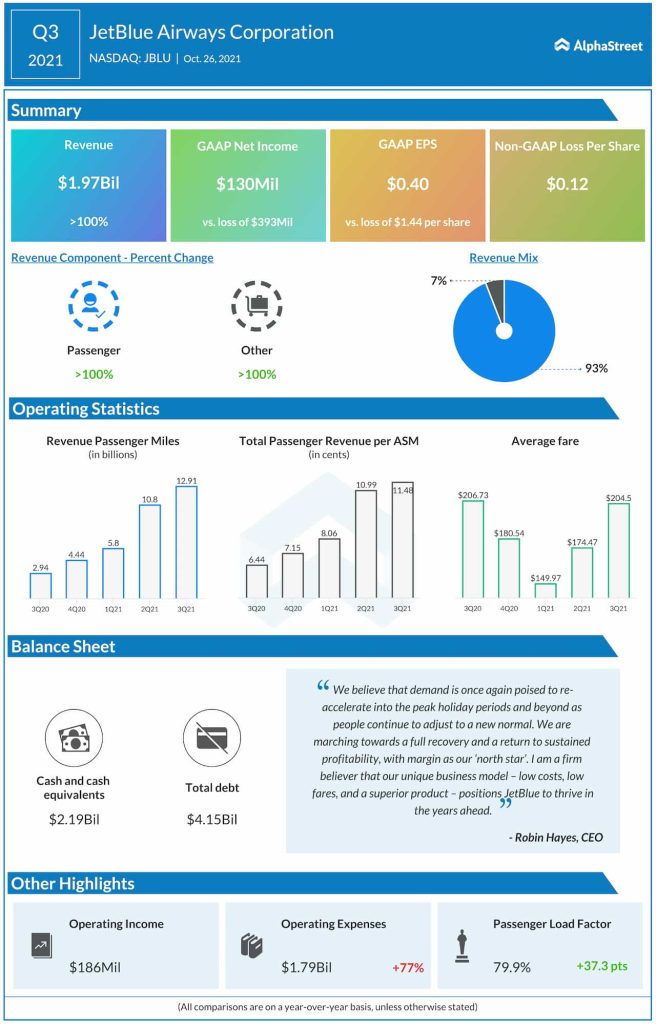

JetBlue’s total operating revenues jumped more than 300% year-over-year to $1.97 billion, beating estimates, but declined 5.5% compared to the third quarter of 2019. The year-over-two drop was better than the company’s assumption of a decline of 6-9% and was driven in part by an uptick in demand as it closed out the quarter. Adjusted loss per share amounted to $0.12 and was narrower than projections.

Trends

During the third quarter, softness in bookings was most pronounced in September as the Delta variant led to a rise in Covid cases. Trends have stabilized since then and continue to improve. The airline is seeing momentum in VFR and leisure demand. JetBlue expects revenue to pick up through the peak holiday season and beyond as things gradually shift back to normal and demand improves.

The company expects to face challenges from a slower recovery in business travel. On its quarterly conference call, JetBlue mentioned that corporate travel, which typically accounts for around 20% of its revenue, is currently trending close to the 5-10% range. Despite this, the company is seeing improvements and expects a more robust recovery this winter.

The Northeast Alliance with American Airlines (NASDAQ: AAL) is proving significantly beneficial to JetBlue. The companies have launched 58 new routes out of the Northeast and added frequencies on more than 130 routes. There are plans for expansion through next year including to 18 new international destinations. This alliance is expected to be margin accretive and JetBlue plans to continue investing in it as business travel recovers.

Outlook

For the fourth quarter of 2021, JetBlue expects revenue to decline between 8% and 13% compared to the fourth quarter of 2019. Capacity is expected to decline 4-7% versus Q4 2019.

JetBlue’s planning assumption for the fourth quarter is for CASM ex-fuel to increase between 14-16% year-over-two, which includes pressure from temporary headwinds tied to the recovery. The company expects CASM ex-fuel to improve from a double-digit growth rate in the second half of 2021 to low single-digit growth in 2022 compared to 2019 levels.

Click here to read the full transcript of JetBlue’s Q3 2021 earnings conference call