Johnson Outdoors Inc (JOUT.NASDAQ), a Wisconsin-based manufacturer of outdoor recreation products spanning fishing, watercraft, camping, and diving, with a market capitalization of approximately $500 million, reported fiscal Q1 2026 results ahead of U.S. market open. Shares closed at $46.88 in the previous session, below the 52-week high of $50.99 but above the 52-week low of $21.33.

Revenue Growth and Profitability Improvement

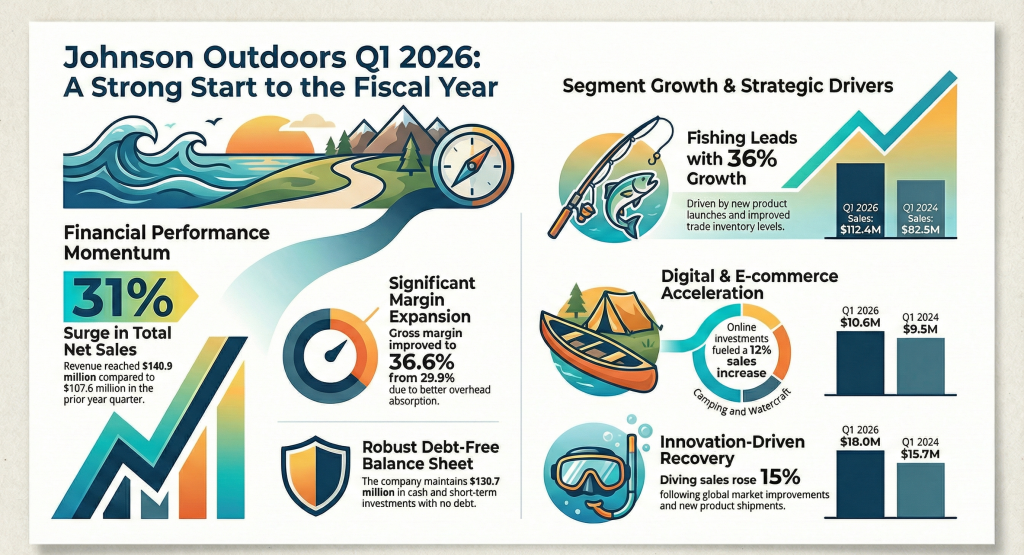

Net sales in the first quarter rose 31% year-over-year to $140.9 million, driven by higher unit volumes across all core segments. Gross margin expanded to 36.6% from 29.9% in Q1 2025, reflecting higher sales volumes and ongoing cost-reduction measures.

Operating loss narrowed sharply to $2.9 million from $20.2 million a year earlier. Net loss fell to $3.3 million, or $0.33 per share, compared with $15.3 million, or $1.49 per share, in the prior-year period. Reported EPS exceeded analyst expectations of approximately –$0.45.

Operating expenses increased by $2.1 million to $54.5 million, primarily due to volume-related costs, but were partially offset by reduced warranty expenses.

Segment-Level Performance

- Fishing: The largest segment posted revenue of $112.4 million, up 36%, returning to an operating profit of $7.5 million from a prior-year loss of $8.3 million. Growth was driven by new product launches, including the Humminbird Explore Series and MEGA Live 2 fish finders, as well as strong Minn Kota trolling motor demand.

- Camping & Watercraft: Sales rose 12% to $10.6 million, aided by increased digital commerce activity. Jetboil cooking systems and Old Town watercraft maintained market leadership.

- Diving: Revenue grew 15% to $18.0 million, reflecting improved global demand and the launch of the SCUBAPRO Hydros Pro 2 buoyancy control device.

The performance demonstrates that volume growth, rather than price increases alone, drove revenue gains across all segments.

Balance Sheet and Liquidity Position

Johnson Outdoors remained debt-free, with $130.7 million in cash and short-term investments as of January 2026. Inventory declined $17.7 million year-over-year to $183.9 million, signaling tighter working capital management. The company also maintained its quarterly dividend.

Strategic Priorities and Outlook

Management highlighted three operational priorities: maintaining innovation pipelines, expanding e-commerce channels, and continuing cost-efficiency initiatives. These measures aim to protect margins amid volatile supply chains and higher material costs.

No quantitative full-year guidance was provided. Seasonal demand trends suggest stronger revenue in the warmer months, which represent the peak selling period for outdoor recreation products.

Market Reaction

Despite exceeding EPS expectations, shares declined in early trading. Analysts cited the absence of full-year guidance and continued macro pressures. There were no significant price-target revisions linked to the Q1 results.

Sector Context and Competitive Positioning

The outdoor recreation sector continues to face consumer spending fluctuations, input cost pressures, and supply chain volatility. Johnson Outdoors’ gross margin expansion and segment profitability indicate effective operational management relative to peers. Competitors range from large generalist sporting goods firms to niche outdoor brands, and growth increasingly depends on innovation and direct-to-consumer digital channels.

Bottomline

Johnson Outdoors’ Q1 2026 results show a sharp turnaround in profitability, strong revenue growth, and improved operational efficiency. The company’s debt-free balance sheet and reduced inventory provide flexibility, but the lack of full-year guidance and sector-wide macro pressures keep investor sentiment cautious. Shares traded down from recent highs despite beating earnings expectations, reflecting the market’s focus on execution risks and broader outdoor recreation trends.