JPMorgan Chase & Co. (NYSE: JPM) and Wells Fargo & Company (NYSE: WFC) reported their earnings results for the third quarter of 2024 on Friday. While JPM’s numbers were better than expected, WFC delivered mixed results. Here’s a recap of some of the main points from these banks’ Q3 reports:

JPMorgan

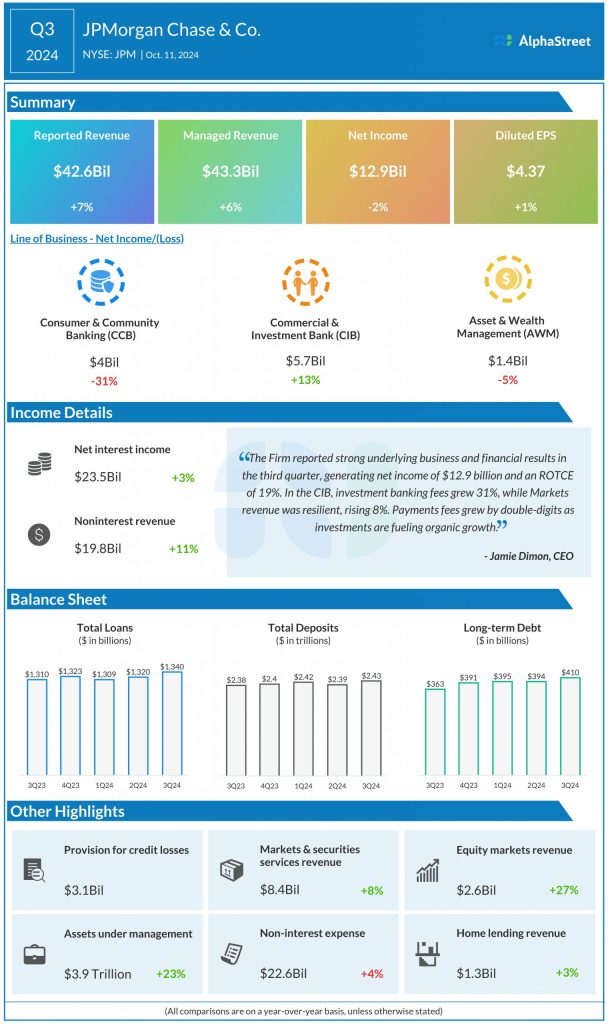

In Q3 2024, JPMorgan’s reported net revenue increased 7% year-over-year to $42.6 billion, beating estimates of $41.7 billion. Net income fell 2% to $12.9 billion. EPS rose 1% YoY to $4.37, surpassing projections of $4.01.

Net interest income grew 3% to $23.5 billion while non-interest revenue increased 11% to $19.8 billion compared to last year. Non-interest expense rose 4% to $22.6 billion, driven by higher compensation, partly offset by lower legal expense. Provision for credit losses was $3.1 billion, reflecting net charge-offs of $2.1 billion and a net reserve build of $1 billion.

Net revenue for the Consumer & Community Banking (CCB) segment dropped 3% YoY to $17.8 billion while revenue for the Commercial & Investment Bank (CIB) segment rose 8% to $17 billion in Q3. Revenue in the Asset & Wealth Management (AWM) segment grew 9% to $5.4 billion, driven by growth in management fees on higher average market levels and strong net inflows, investment valuation gains, and higher brokerage activity.

“We have been closely monitoring the geopolitical situation for some time, and recent events show that conditions are treacherous and getting worse. There is significant human suffering, and the outcome of these situations could have far-reaching effects on both short-term economic outcomes and more importantly on the course of history. Additionally, while inflation is slowing and the U.S. economy remains resilient, several critical issues remain, including large fiscal deficits, infrastructure needs, restructuring of trade and remilitarization of the world. While we hope for the best, these events and the prevailing uncertainty demonstrate why we must be prepared for any environment.” – CEO Jamie Dimon

Wells Fargo

Wells Fargo reported total revenue of $20.37 billion for the third quarter of 2024, which was down 2% from the same period last year and below expectations of $20.4 billion. Net income decreased 11% to $5.1 billion. EPS dropped 4% YoY to $1.42 but beat the consensus target of $1.28.

Revenue in the Consumer Banking and Lending segment decreased 5% YoY to $9.1 billion while revenue in Commercial Banking fell 2% to $3.3 billion in Q3. Corporate and Investment Banking revenue saw a slight dip to $4.91 billion while Wealth and Investment Management revenue increased 5% to $3.9 billion.

Net interest income decreased 11% YoY to $11.7 billion in Q3, mainly due to higher funding costs and lower loan balances. Non-interest income grew 12% to $8.7 billion, driven by better results from venture capital investments, an increase in asset-based fees in Wealth and Investment Management, higher investment banking fees, higher net gains from trading in the Markets business, and higher deposit-related fees.

Non-interest expense dipped slightly to $13 billion, as the impact of efficiency initiatives was offset by a rise in revenue-related compensation, and technology and equipment expenses. Provision for credit losses was down 11% to $1 billion.

Shares of JPMorgan and Wells Fargo were up over 4% and 6% respectively, in midday trade on Friday.