Abbott Laboratories (NYSE: ABT) has contributed significantly to COVID care activities by providing test kits, and the healthcare conglomerate’s revenues benefitted from that in recent years. Since the demand for coronavirus diagnostics has fallen sharply, the company is banking on its strong R&D pipeline, with an array of product launches lined up, to drive growth going forward.

However, the management’s cautious guidance – though the outlook is well above the pre-pandemic numbers — shows the current weakness is likely to continue this year. Interestingly, it still predicts COVID testing-related sales of $750 million for the first quarter and about $2 billion for fiscal 2023. Meanwhile, the top line is expected to be impacted by unfavorable exchange rates.

A Good Buy?

ABT has long been an investors’ favorite, thanks to regular dividend hikes and a decent yield of about 2% which is above the average for the benchmark S&P 500 index. The stock experienced fluctuations since peaking more than a year ago and is currently trading slightly above $100. It is expected to grow in double digits in the next twelve months, creating significant shareholder value. The majority of experts following the stock recommend buying it.

Going forward, Abbott’s diversified business model would come in handy for beating challenges like the fall in COVID diagnostics. In January, Navitor, the company’s next-generation transcatheter aortic valve implantation system, received FDA approval. Earlier, its FreeStyle Libre 2 and FreeStyle Libre 3 integrated continuous glucose monitoring system sensors for integration with automated insulin delivery systems got regulatory clearance.

Baby Formula Blues

Meanwhile, an investigation by the Justice Department into its baby formula manufacturing facility in Michigan came as a setback for the company a few months ago. Earlier, it had shut down the plant and ceased production due to major sanitization lapses. The company also initiated a recall of its popular infant nutrition formulas like Similac, which in turn resulted in a shortage of such products in the market.

From Abbott Laboratories’ Q4 2022 earnings conference call:

“As we reflect back on the impact of COVID testing efforts over the last few years, it’s clear that our success in this area will have a positive long-lasting impact for the company. It strengthened our strategic position in diagnostics through the expansion of our installed base of instruments, including ID NOW, our rapid point-of-care molecular testing platform, and through the opening of new testing channels such as physician offices and at-home testing.”

Financials

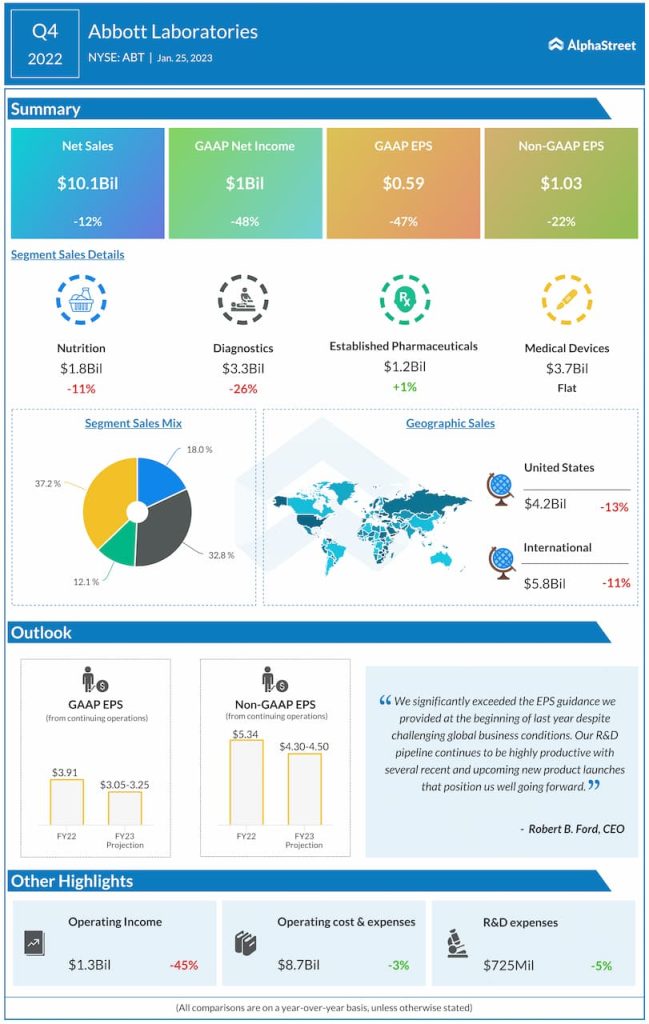

The company is all set to report financial results for the first three months of fiscal 2023 on April 19, in the morning. It enjoys the rare distinction of not missing earnings estimates not even once in the past, and the trend was maintained in the fourth quarter. Though revenue declined in double digits to $10.1 billion in the December quarter, it exceeded the forecast. There was weakness across all operating segments and geographical divisions. At $1.03 per share, adjusted earnings were down 22%.

ABT opened Tuesday’s session at $104.42 and traded slightly higher in the early hours. It has lost about 5% since the beginning of the year.