Shares of Delta Air Lines (NYSE: DAL) were down over 2% on Tuesday after the company published its fourth quarter 2025 earnings report. While the top line surpassed estimates, the bottom line matched expectations. The airline anticipates revenue growth in the upcoming fiscal year as demand remains steady.

Revenue beats, earnings in-line

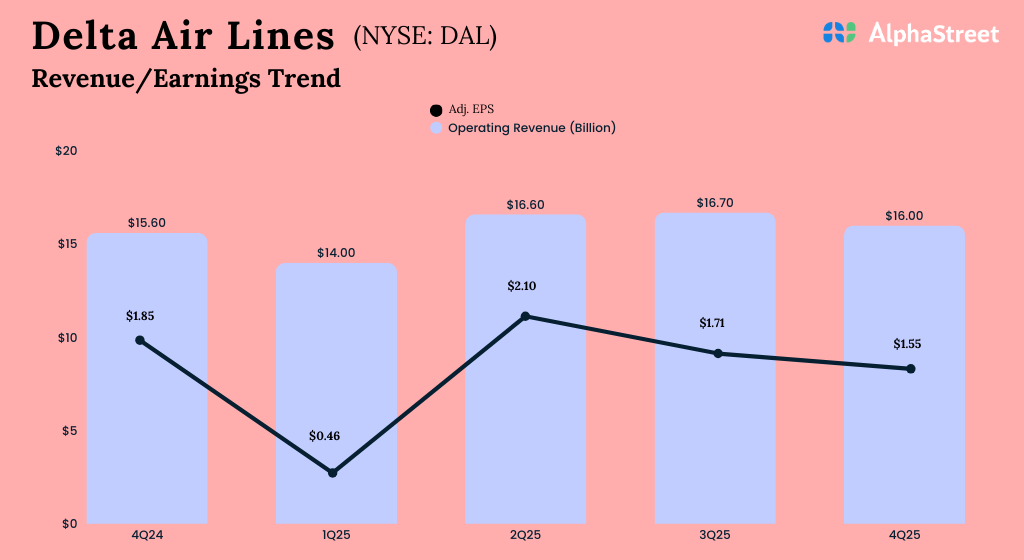

In the fourth quarter of 2025, Delta’s operating revenue increased 3% year-over-year to $16 billion, beating estimates of $15.7 billion. On a GAAP basis, earnings per share rose 44% to $1.86. On an adjusted basis, EPS fell 16% YoY to $1.55 but was in line with projections.

Growing demand for premium

In the December quarter, Delta’s diverse revenue streams saw high-single-digit growth from the previous year, reflecting strong demand for premium products. Premium revenue grew 9% in Q4 while loyalty travel awards were up 5%. Although cargo revenue dipped 1%, other revenue was up 14%.

In Q4, passenger revenue inched up 1% as domestic revenue remained flat YoY. Within international, Pacific saw 10% growth and Atlantic saw a 4% gain but Latin America was down 5%. Corporate sales witnessed high-single-digits increase in Q4, with broad-based growth across every sector.

In the December quarter, unit revenue was up 2% on a 1.3% rise in capacity. Passenger revenue per available seat mile (PRASM) remained flat while passenger load factor stood at 82%. CASM-Ex was up 4% while average price per fuel gallon was $2.28.

Outlook

Delta is seeing top line growth continue to gain pace supported by demand. For the first quarter of 2026, it expects total revenue to grow 5-7% YoY and EPS to range between $0.50-0.90. For fiscal year 2026, EPS is expected to be $6.50-7.50, representing a growth of 20% at the midpoint.