Shares of General Mills, Inc. (NYSE: GIS) stayed red on Wednesday, following the company’s announcement of its first quarter 2026 earnings results. The bottom line beat estimates while the top line matched expectations. The company anticipates a challenging consumer environment and lower-than-expected category growth in fiscal year 2026, and plans to focus primarily on restoring organic sales growth during the year.

Q1 results

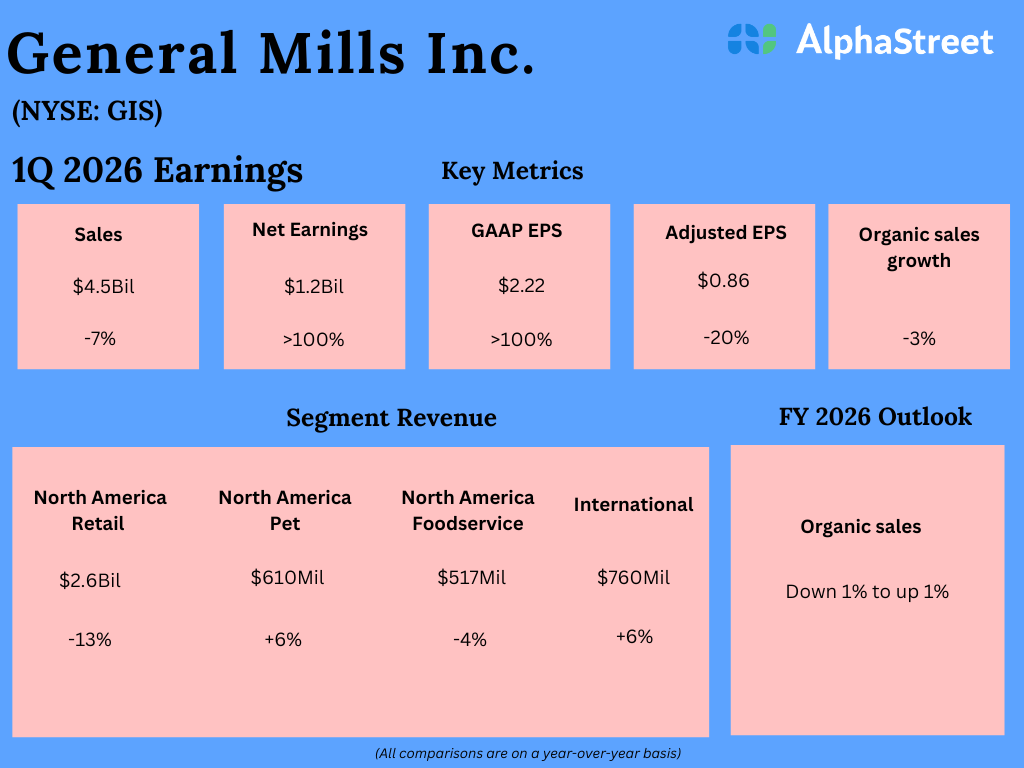

In Q1 2026, General Mills’ net sales decreased 7% year-over-year to $4.52 billion, but came in line with estimates. Organic sales were down 3%, mainly due to unfavorable price realization and mix. On a GAAP basis, earnings more than doubled YoY to $2.22 per share. On an adjusted basis, EPS fell 20% in constant currency to $0.86 but surpassed projections of $0.82.

Business performance

During the first quarter, sales in the North America Retail segment decreased 13% YoY. Sales were down double-digits for the Big G Cereal & Canada operating unit, mainly due to the divestiture of the yogurt business. Sales were down high-single-digits for US Snacks and low-single-digits for US Meals & Baking Solutions.

Sales in the Pet segment grew 6% from last year, helped by the North American Whitebridge Pet Brands acquisition. Within this segment, cat food and pet treats saw double-digit sales growth while dog food saw a mid-single-digit decline, mainly due to headwinds from the Wilderness product line. Sales in the Foodservice segment were down 4% while International segment sales were up 6% in the first quarter.

Outlook

General Mills anticipates a difficult consumer environment in fiscal year 2026, and expects category growth to come below its long-term projections due to less price/mix benefit. The company’s main focus during the year will be on restoring volume-driven organic sales growth.

During the year, GIS plans to invest more in brand-building and product innovation in order to boost its categories and drive market share. This includes launching Blue Buffalo into the fast-growing US fresh pet food sub-category during the second quarter of 2026. These investments, along with input cost inflation, are expected to outpace cost savings and other benefits during the year.

Accordingly, the company expects organic sales for FY2026 to range between down 1% and up 1%, and adjusted EPS to be down 10-15% in constant currency.