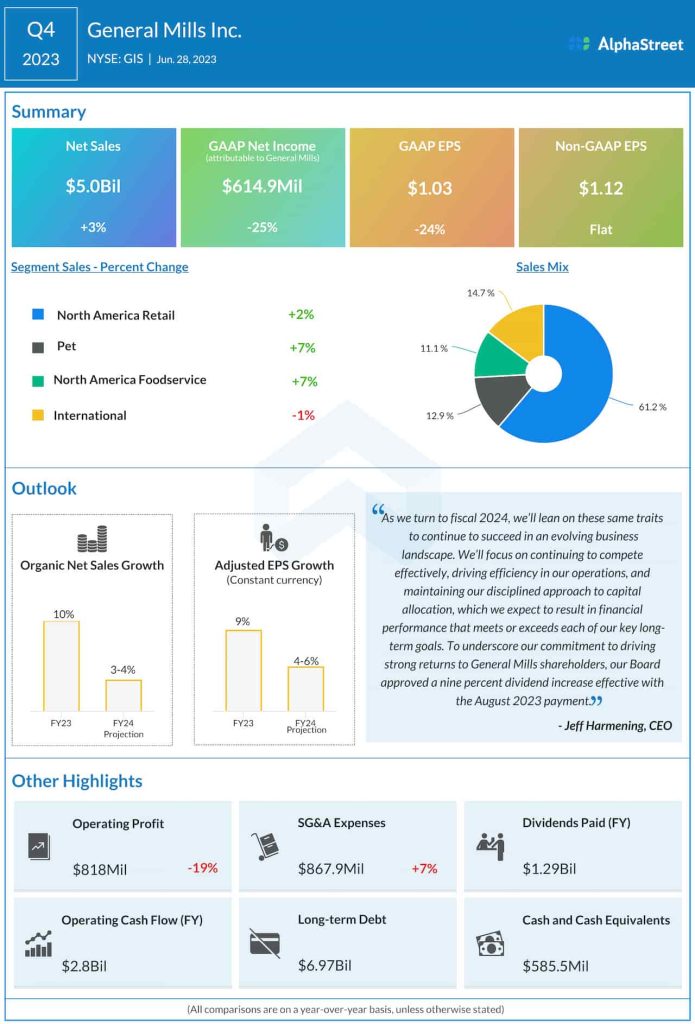

General Mills, Inc. (NYSE: GIS), the company behind popular food brands like Cheerios and Pillsbury, ended fiscal 2023 on a weak note. in the fourth quarter, volumes declined across all business divisions amid a slowdown in the demand for its meal kits and ready-to-eat cereals.

The Minneapolis-headquartered consumer foods company’s shares climbed to a record high of $90.61 in mid-May, but they pulled back pretty soon and have lost 15% since then, slipping below the 52-week average. The company’s not-so-impressive fourth-quarter data and weak guidance added to the downturn. Despite the dip, the valuation seems to be high and that should be taken into consideration before investing. Meanwhile, in a move that should bring cheer to shareholders, the management raised the dividend by 9%, effective the August 2023 payment. Pursuant to the hike, the yield has increased to 3.1%.

Inflation Woes

In an effort to counter the high inflation, General Mills has raised product prices, and that is having a negative impact on sales volumes as consumers continue to tighten their belts due to economic uncertainties. With more price hikes in the cards, margins, and profitability would remain under pressure this year.

With supply chain issues easing, the company now plans to focus more on product innovation and marketing, which in turn would translate into sales as the year progresses. Meanwhile, consumers’ propensity to eat at home, rather than eat out, due to concerns about the inflationary environment is likely to drive demand.

Mixed Q4

In the final months of fiscal 2023, higher sales at the North America Retail, Foodservice, and Pet divisions led to a modest increase in net sales to around $5 billion, which was partially offset by a decline in the International segment. The top-line growth was restricted by unfavorable foreign exchange rates and headwinds from net divestiture/acquisition activity to some extent. Fourth-quarter earnings, adjusted for one-off items, remained unchanged at $1.12 per share while unadjusted profit declined in double digits to $1.03 per share. Sales fell short of expectations while earnings beat, as they did in each of the trailing five quarters.

From General Mills’ Q4 2023 earnings call:

“As we look at what’s going to drive growth, I think it will be a number of factors. One I would lead with this new product innovation. Even though our new product innovation has led our categories each of the last four years, it’s still below what we would have expected normally. And the reason is not because we haven’t had good innovation is because some retailers were reluctant to bring it in because their own supply chains were pressured, our own supply chains were pressured.”

Weak Guidance

The company’s leadership forecasts muted earnings and organic sales growth for the fiscal year, reflecting the decline in demand due to the recent price hikes. Full-year adjusted profit is expected to grow by 4-6%, lower than the 9% earnings growth recorded in fiscal 2022. The estimated organic sales growth is between 3% and 4%, compared to last year’s 10% increase.

GIS traded lower throughout Thursday, after falling about 6% in the previous session following the earnings announcement. Currently, the value is close to where it was 12 months ago.