Shares of the J.M. Smucker Co. (NYSE: SJM) were down over 2% on Tuesday. The stock has gained 11% over the past three months. The branded food company delivered better-than-expected earnings results for the third quarter of 2024 and updated its guidance for the full year. Here are the key takeaways from the Q3 report:

Results beat estimates

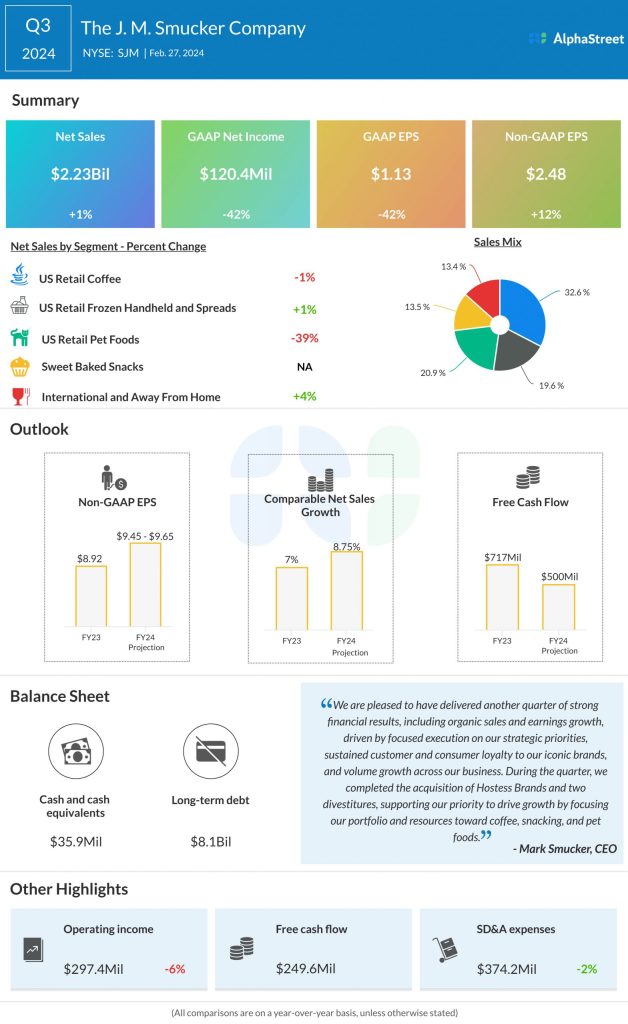

In Q3 2024, JM Smucker delivered revenue and earnings which grew on a year-over-year basis and surpassed projections. Net sales rose 1% to $2.23 billion. Comparable sales increased 6%, helped by net price realization and favorable volume/mix. Adjusted EPS increased 12% to $2.48, driven by improved gross margin and favorable SD&A expenses.

Reshaped portfolio

JM Smucker’s acquisition of Hostess Brands and its divestitures of the Sahale Snacks and Canadian condiments businesses will help it focus its resources on categories such as coffee, snacking and pet foods which have good growth potential.

In Q3, sales in the Coffee segment decreased 1%, mainly due to a list price decline, as the company passed the benefit of lower coffee costs to customers. The segment benefited from strong performances from the Café Bustelo, Dunkin and Folgers brands during the quarter.

Sales in the Frozen Handheld and Spreads segment grew 1% on a reported basis and 2% on a comparable basis. Sales for Jif peanut butter grew double-digits during the quarter while total company net sales for Uncrustables sandwiches rose 6%.

The Pet Foods segment saw sales decrease 39% in Q3 on a reported basis, reflecting sales from the divested pet food brands. Excluding this, sales grew 20%, driven by strong growth in the Meow Mix and Milk-Bone brands. Profit margin improved significantly in this segment as the company focuses on its leading brands and categories.

The newly-formed Sweet Baked Snacks segment contributed $300.3 million in net sales during the third quarter, with strong performances from the Hostess and Voortman brands. SJM remains bullish on the long-term growth prospects of this segment. The International and Away From Home segment saw sales grow 4% on a reported basis and 9% on a comparable basis in Q3.

Updated outlook

SJM updated its outlook for the full year of 2024 and now expects comparable net sales to increase 8.75% versus the prior year. This compares to the previous range of 8.5-9.0% growth. The comparable sales outlook reflects favorable volume/mix and higher net pricing. Net sales for the year are expected to decrease around 3.6% to approx. $8.22 billion, reflecting impacts from the recent acquisition and divestitures.

Adjusted EPS is now expected to range between $9.45-9.65 in FY2024 compared to the prior range of $9.25-9.65. The earnings outlook reflects negative impacts from the pet food divestiture and the Hostess Brands acquisition.

For the fourth quarter of 2024, SJM expects comparable net sales to increase a mid-single digit percentage and adjusted EPS to decline by a mid-teen percentage.