Shares of McCormick & Company, Incorporated (NYSE: MKC) rose over 4% on Thursday, after the company delivered better-than-expected earnings results for the second quarter of 2024. The stock has dropped 7% over the past three months. The spice maker also reaffirmed its guidance for the full year. Here are the key takeaways from the earnings report:

Results beat estimates

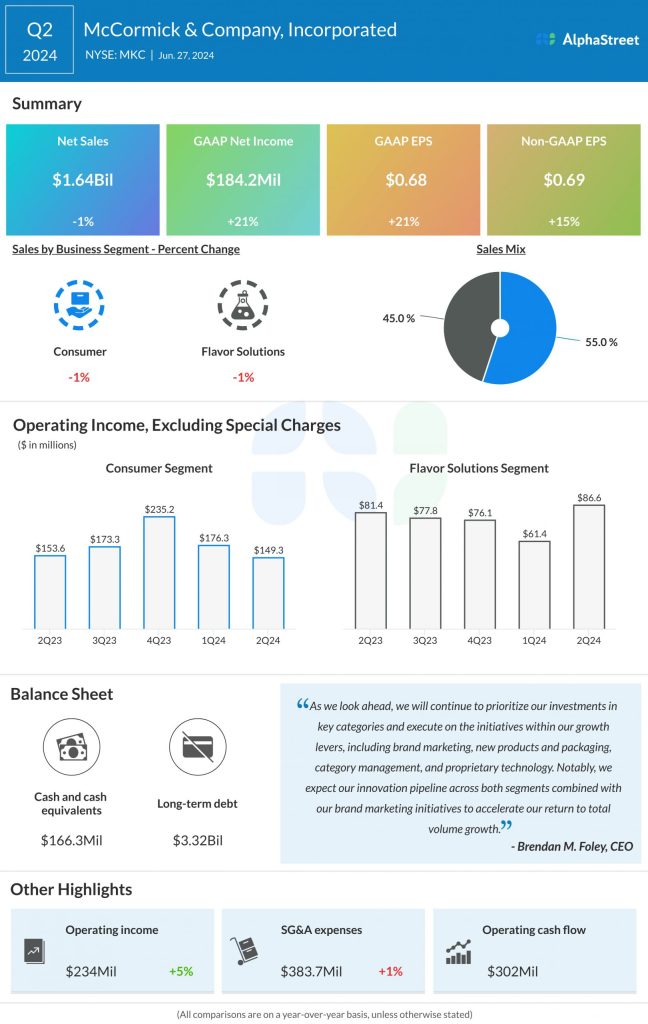

McCormick’s net sales for the second quarter of 2024 decreased 1% year-over-year to $1.64 billion, but surpassed estimates of $1.63 billion. The decline was caused by volume decreases in the Flavor Solutions segment and the impact from the divestiture of a small canning business. Adjusted EPS rose 15% to $0.69, beating the consensus target of $0.59.

Segment sales declines

McCormick saw sales decrease across both its segments during the second quarter. Sales in the Consumer segment dipped by 1% to $904.5 million, reflecting a 1% decrease from pricing, which was partly offset by modest volume growth.

Within Consumer, the company saw strong volume growth in core categories across its major markets. It benefited from spices and seasonings unit share gains in the US and recipe mix share gains in the UK. Volume declines in prepared foods categories negatively impacted results in this segment.

Consumer sales in the Americas decreased 2% due to price decreases and flat volumes. Sales in Europe, Middle East and Africa (EMEA) increased 5%, helped by higher volume and product mix. Sales in the Asia-Pacific (APAC) region fell 5%, due to volume declines, driven mainly by slower demand in China.

Sales in the Flavor Solutions segment dropped 1% to $738.7 million, mainly due to a decline in volume and product mix as well as the divestiture of the canning business. Sales in the Americas remained flat while in EMEA, it declined 7%, hurt by softness in volumes of some quick service restaurant and packaged food customers. APAC sales rose 6%, helped by growth in volume and product mix, driven by new products, as well as an increase from pricing.

Reaffirmed outlook

McCormick reaffirmed its full-year 2024 outlook. It expects sales to range between down 2% to flat for the year. On a constant currency basis, sales are expected to be down 1% to up 1%. It also expects to benefit from last year’s pricing actions.

The company expects to return to volume growth during the year by improving its volumes through investments and brand strength. However, the discontinuation of low margin business and the divestiture of the canning business are expected to impact volume growth in 2024.

GAAP EPS for the year is expected to range between $2.76-2.81 while adjusted EPS is expected to be $2.80-2.85.