Software giant Oracle Corporation (NYSE: ORCL) this week delivered mixed results for the second quarter — earnings topped expectations while revenues missed the Street view. The updated version of Oracle Cloud Infrastructure, with the added strength of artificial intelligence, positions the company to expand its market share.

The Stock

A few months ago, Oracle’s stock climbed to an all-time high but experienced weakness since then. It suffered a major loss soon after the earnings release and is currently trading in line with the 52-week average. Currently, the stock is fairly valued. When it comes to buying ORCL, investors will be closely tracking the performance of the cloud business, which has been struggling to keep pace with peers.

Recently, the Oracle leadership exuded optimism that going forward, revenue growth will accelerate every year. They bet on the company’s unique offerings like Dedicated Region, Sovereign Cloud, and Alloy, which enables partners to become cloud providers, to gain an edge over competitors.

However, recent data shows that Oracle’s cloud business grew at a slower pace than most of its competitors, including AWS, Google, and Microsoft. Considering the relatively slow cloud growth since the launch of the business, it needs to be seen whether the company can take full advantage of the growing demand for cloud infrastructure and generative services.

Outlook

For the near term, the management sees a 6-8% revenue growth in the third quarter, including contributions from the Cerner healthcare division which was acquired last year. Total cloud revenue, excluding the Cerner business, is expected to grow between 26% and 28% in Q3. It is looking for adjusted earnings per share in the range of $1.35 to $1.39, which represents a 10-14% growth.

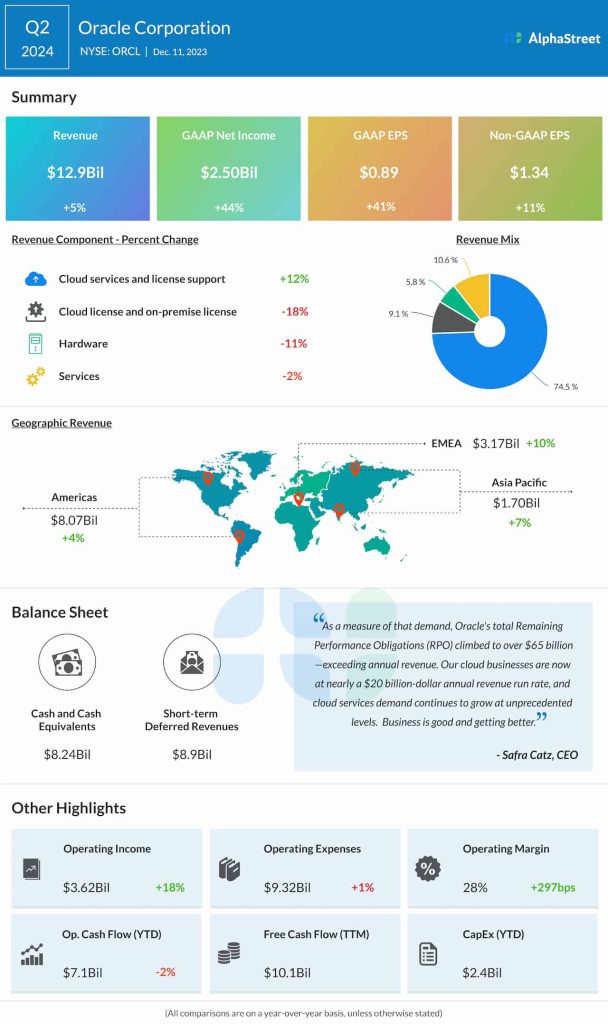

Second-quarter revenues totaled $12.9 billion, compared to $12.3 billion in the corresponding period of 2023. But the latest number fell short of expectations. Earnings, excluding special items, was $1.34 per share in the November quarter, compared to $1.21 per share in the prior-year period. Earnings came in at the high end of the management’s guidance and topped expectations, marking the fifth beat in a row. The company reported an unadjusted net income of $2.50 billion or $0.89 per share for Q2, compared to $1.74 billion or $0.63 per share in the prior-year quarter.

Cloud Business

Cloud Services and License Support, the largest segment that generates recurring revenue, has grown to 74% of the total business, growing by about $1 billion from Q2 2023. Revenues of the other divisions, which are non-recurring, declined year-over-year. Geographically, meanwhile, revenues grew across all regions.

From Oracle’s Q2 2024 earnings call:

“Rather than just offer public cloud services like our competitors, we are the only vendor which also offers dedicated Cloud@Customer; dedicated region; sovereign clouds; and Alloy, our partner cloud. And then finally, our belief in the importance of multi-cloud offerings will be industry-changing as these collaborations roll out. With all this success and exploding demand, we are working as quickly as we can to get the cloud capacity built out.”

Shares of Oracle closed the last trading session slightly above the $100 mark. It maintained a downtrend in early trading on Wednesday, reflecting the negative investor sentiment.