Shares of PepsiCo, Inc. (NASDAQ: PEP) gained over 1% on Tuesday even though the company delivered mixed results for the third quarter of 2024 and lowered its guidance for the full year. Earnings beat estimates while revenue fell short, as the beverages giant faced headwinds from soft category trends and global challenges. Here are the key takeaways from the Q3 report:

Revenues miss, earnings beat

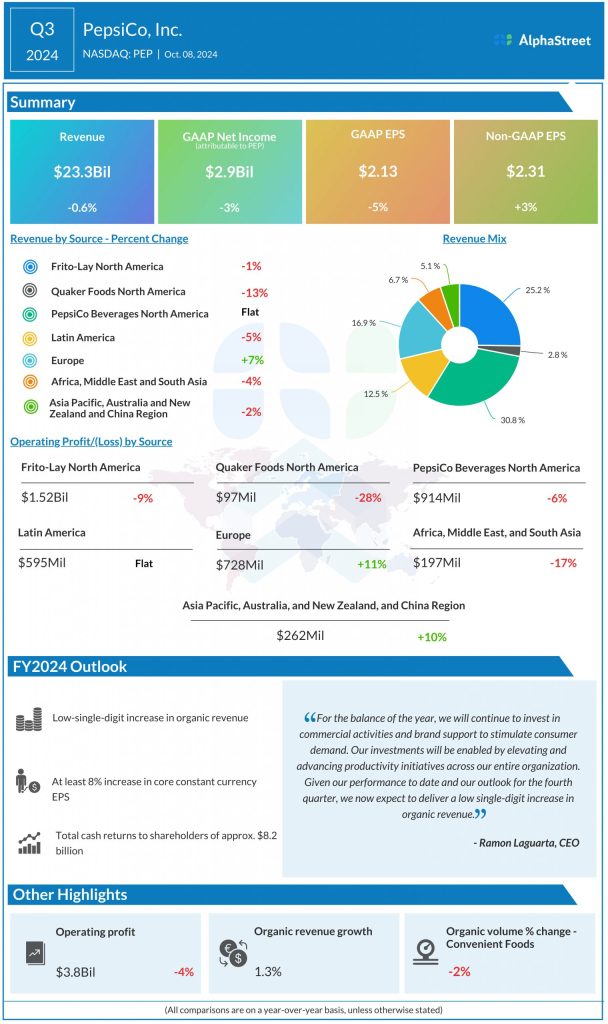

In Q3 2024, PepsiCo’s revenues dipped 0.6% year-over-year to $23.3 billion, narrowly missing estimates of $23.7 billion. Organic revenue growth was 1.3%. GAAP EPS fell 5% to $2.13 in Q3. Adjusted EPS grew 3% to $2.31, beating projections of $2.26.

Inflation hits snack demand

In the third quarter, on a reported basis, PepsiCo saw revenues decline across most of its segments except Europe, which recorded a 7% growth. Revenue for the PepsiCo Beverages North America segment remained flat in Q3 compared to the prior-year period.

On an organic basis, revenue in the Frito-Lay segment dropped 1% in Q3 as inflationary pressures impacted consumers’ spending, leading to softness in snacks. Revenue in the Quaker Foods segment fell 13%, hurt by product recalls and muted category performance. On its earnings call, PepsiCo said it expects revenues for the Quaker segment to improve in the fourth quarter of 2024 as it resumes production of the items affected by recalls.

Organic revenue for PepsiCo Beverages rose 1%, helped by growth for brands such as Gatorade, Propel and bubly, as well as gains in the away-from-home and e-commerce channels.

Although PepsiCo’s business was negatively impacted by geopolitical tensions in certain international markets, its International division saw organic revenues grow by 4% in Q3. Within International, the convenient foods business saw organic revenue growth of 3% while the beverages business saw organic revenues increase by 7%.

Guidance cut

PepsiCo expects customers to remain budget-conscious against an inflationary backdrop. It also anticipates geopolitical challenges and macroeconomic headwinds to persist in some of its international markets. Although inflationary pressures are anticipated to moderate compared to last year, some commodity costs might remain high.

Based on the muted performance of its categories and its year-to-date results, PepsiCo lowered its organic revenue guidance for fiscal year 2024. The company now expects a low-single-digit increase in organic revenue in FY2024 versus its previous expectation of approx. 4% growth. It also expects organic revenue growth in the International segment to surpass growth in the North America segment during the year.

PepsiCo continues to expect core constant currency EPS growth of at least 8% in FY2024. It estimates core EPS to grow 7% YoY to at least $8.15 for the year.