Shares of Snap Inc. (NYSE: SNAP) plummeted 26% on Friday, after the company delivered mixed results for the second quarter of 2024 a day ago and provided third-quarter guidance that did not impress the Street. Here are the key takeaways from the earnings report:

Quarterly numbers

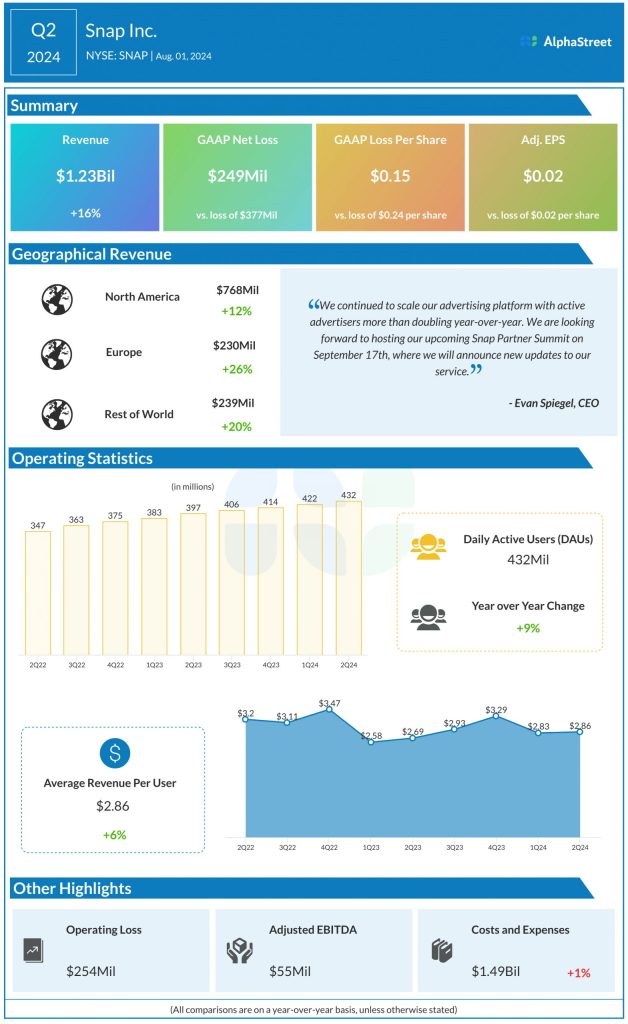

Snap generated revenues of $1.24 billion for Q2 2024, which rose 16% year-over-year but fell below estimates of $1.25 billion. GAAP net loss narrowed to $0.15 per share from $0.24 per share last year. Adjusted EPS amounted to $0.02, which came in line with expectations.

User growth and engagement

Snap’s monthly active users (MAUs) reached over 850 million in Q2, as it aims for 1 billion MAUs. Daily active users (DAUs) stood at 432 million, which was up 9% YoY. DAUs in North America dipped slightly to 100 million, while DAUs in Europe grew 3% to 97 million. Rest of World DAUs grew 16% to 235 million in Q2.

During the quarter, Snap saw improvement in content engagement with global time spent watching content growing 25% YoY. Global content viewers grew 12% YoY in Q2. Growth in engagement was mainly driven by growth in total time spent watching Spotlight and Creator Stories.

Advertising

In the second quarter, Snap’s advertising revenue increased 10% YoY to $1.13 billion. Direct response (DR) advertising revenue rose 16% YoY, supported by strong growth in active advertisers and early contributions from product improvements. Brand-oriented advertising revenue fell 1% YoY, mainly due to weak demand in certain consumer discretionary verticals such as retail, technology, and entertainment.

During the second quarter, Snap witnessed strength in DR in North America, helped by robust growth in the small and medium-sized customer segment. Brand-oriented demand remained weak in this region. The company witnessed continued progress on its DR ad platform in both Europe and Rest of World during the quarter while the demand environment for brand-oriented advertising solutions remained relatively stable in Europe.

Outlook

For Q3 2024, Snap expects revenue to range between $1.33-1.37 billion, representing a growth of 12-16% YoY. The company anticipates DAUs will reach approx. 441 million in the third quarter.