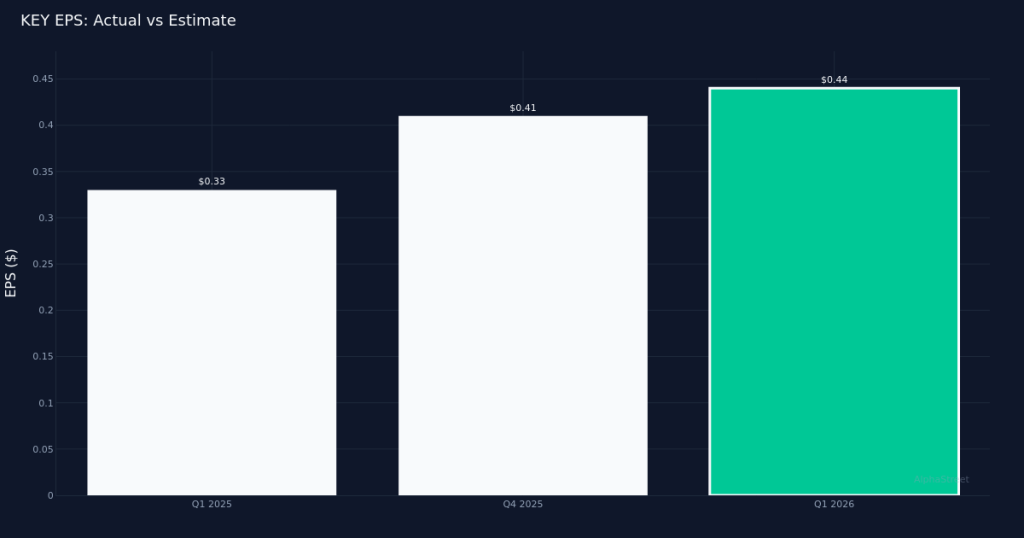

Solid Beat. KeyCorp (NYSE: KEY) delivered Q1 2026 diluted earnings of $0.44 per share, surpassing analysts’ $0.41 forecast by 7.3% based on estimates from 11 analysts. Revenue of $1.95B exceeded Wall Street’s $1.94B forecast by 0.7%, marking a tenth consecutive quarter of steady execution for the regional bank. The company earned $486.0M in net income as it continues to capitalize on favorable lending conditions and sustained deposit growth across its franchise.

Strong Year-Over-Year Growth. The results reflect meaningful momentum from the prior year, with EPS up 33.3% from $0.33 in Q1 2025 and revenue climbing 10.2% from $1.77B. This represents KeyCorp’s strongest year-over-year performance in recent quarters, demonstrating the firm’s ability to drive profitable growth while navigating a complex rate environment. Net interest margin was up 2.87% for the quarter, a critical metric that signals the bank is effectively managing the spread between what it earns on loans and pays on deposits—the core engine of profitability for regional lenders.

Commercial Bank Drives Performance. The Commercial Bank segment led with $1.12B in revenue, up 6.7% year-over-year, underscoring KeyCorp’s strength in middle-market lending and treasury management services. This segment remains the backbone of the company’s revenue base, and its consistent growth suggests healthy demand from business clients despite economic uncertainty. The performance indicates KeyCorp is maintaining competitive positioning in its core markets while managing credit quality effectively—a balance that regional banks have struggled to achieve in tightening cycles.

Quality of Beat. The earnings outperformance appears fundamentally sound, driven by top-line revenue expansion rather than aggressive cost-cutting measures. The revenue beat, while modest at 0.7%, combined with the substantial 33.3% EPS growth year-over-year, points to operating leverage and improved efficiency naturally flowing through the income statement. This is a more sustainable path to profitability than reliance on expense reduction alone, particularly for a bank positioned to capture market share in commercial lending.

Muted Market Response. The stock remained largely unchanged following the report, suggesting investors had already priced in much of the positive momentum or are waiting for clearer signals on credit trends and loan growth sustainability. Wall Street consensus stands at 11 buy, 12 hold, and 0 sell ratings—a relatively balanced view that reflects cautious optimism but not overwhelming conviction. The lack of sell ratings indicates analysts see limited downside, even as they debate the upside potential amid regional banking sector headwinds.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.