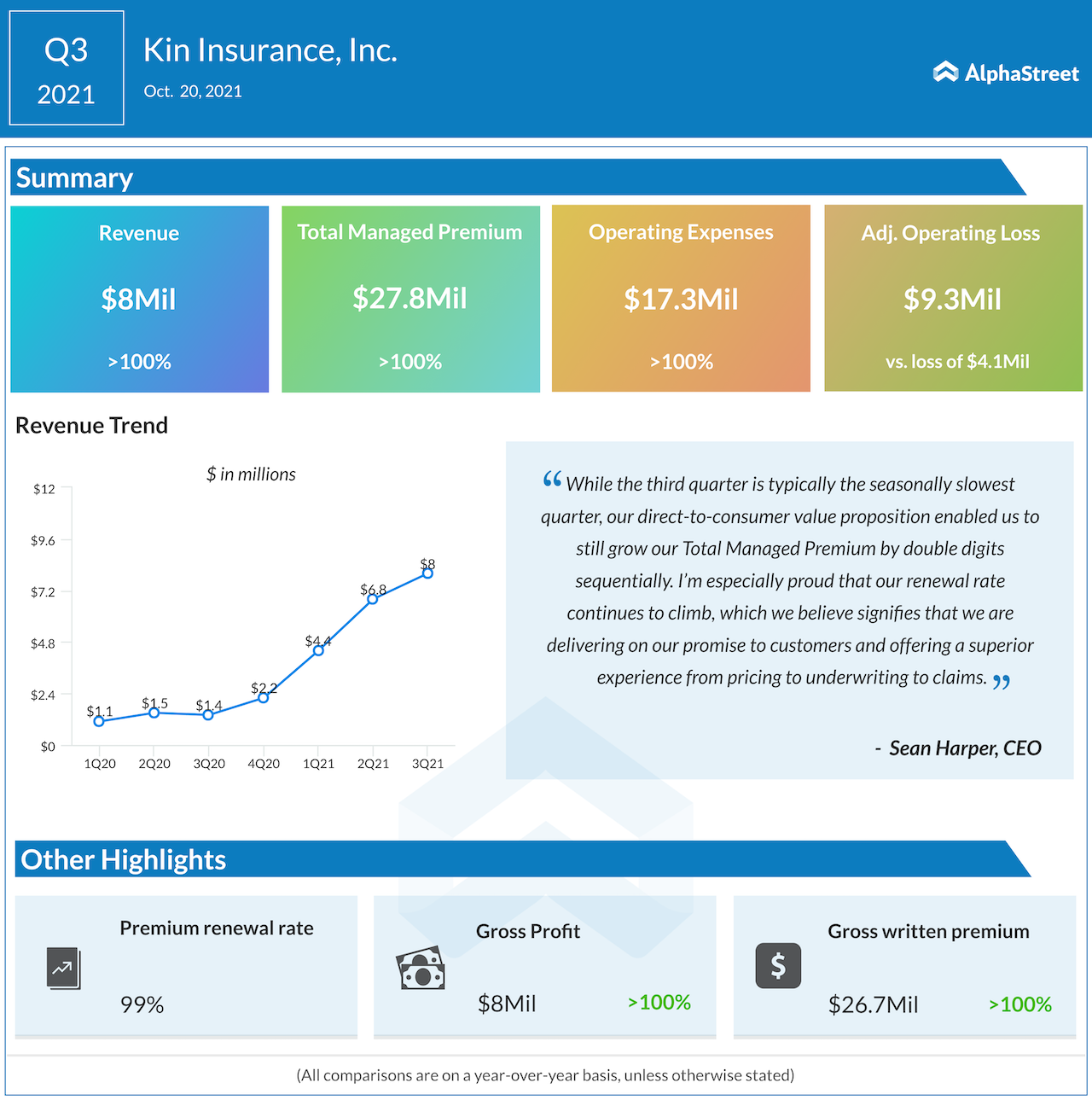

What factors drove the 420% increase in managed premium in Q3, despite being a cyclically slow quarter? Should investors expect a similar trend in the upcoming quarters?

While the third quarter is typically the seasonally slowest quarter, Kin’s direct-to-consumer value proposition enabled us to still grow our Total Managed Premium by double digits sequentially. We’ve built a company that enables us to acquire new customers efficiently, and this past quarter we invested more into it. Kin’s renewal rate on the carrier also increased to a record 99%.

We expect to experience a similar trend in the upcoming quarters because we have been adamant about not scaling this business prematurely. Our focus continues to be on making sure the math around our customer acquisition works really well and renews at a high rate.

{kind=link}

How do you manage risks and fraudulent claims when you do away with all the traditional documentations?

Reducing fraud and the risk that comes with it is imperative in our business. For example, the industry has been plagued by a type of fraud called Assignment of Benefits, which involves an agreement that transfers insurance claims rights to another party — usually a contractor. They take advantage of the agreement and inflate repairs and costs or bill for work that was never completed, which can hurt policyholders.

That’s why we created the Responsible Repair Discount, which rewards homeowners who decline to hand over their claim benefits to a vendor. We also offer a Managed Repair Program to connect our policyholders with a trustworthy licensed, insured, local contractor to handle repairs so they don’t have to vet professionals.

We rely on traditional documentation of losses – but we believe we acquire that documentation in a more strategic manner. For example, customers can get the claims process started via our website or by phone, email, or text. After a major disaster like Hurricane Ida, we also leverage aerial imagery to assess the damage, oftentimes before evacuated policyholders even return home.

ALSO READ Wellteq CEO Scott Montgomery: Our platform aimed at coaching people towards better health habit

What’s your customer growth trend and churn rate? And how is the general customer demographics?

Kin’s average customer age is 57, which is unique for a direct-to-consumer brand – many DTC businesses cater to younger customers. Kin’s customers have relatively high spending power, are embracing technology, and often recommend businesses they love to their friends and family. We believe these demographics provide us with a wealth of future cross-sell opportunities for existing and new customers. Last quarter, Kin had only a 1% churn rate, which is lower than our peers in the market.

What is going to be your focus over the next two years?

Our most important priority is to grow. We intend to grow a lot in the states where we currently operate, which are a $20 billion market in aggregate. We also plan to grow into new states; we anticipate we will launch enough new states next year that our TAM will be $50 billion. We are also focused on product innovation.

Why choose the SPAC route for public listing?

Our unit economics are very strong – our LTV (lifetime value of a customer) to CAC (customer acquisition cost) ratio is 7.9x, driven by our high premium-per-customer and by our low churn rate. Because our unit economics are so strong and predictable, we are in a good position to go public through the business combination with the SPAC and to use the proceeds of the transaction to fund our growth plan and continue to scale. We chose the SPAC route mainly because the SPAC we are merging with is strategic and able to help us progress the business in a variety of ways.

Overall, we chose to go public because it’s our mission to create a solution at the intersection of climate change and technology that disrupts the 100+-year-old insurance industry. By going public, we’re able to bring our solution to more homeowners.

ALSO READ Resonate Blends CIO David Thielen: Spent the last 18 months cleaning up our balance sheet

Did Covid have an impact on your business?

We moved our operations entirely online in March 2020. Unlike most insurance companies, we are a digitally-native business and were able to keep operating without major disruption. The nature of our business is that people need home insurance, pandemic or not, so we’ve been able to not only retain all our staff during COVID-19 but also to grow our team. Looking ahead, we intend to continue hiring the best and brightest talent to help elevate our data-centric insurance solutions that address the needs of today’s world.

________