CarMax, Inc. (NYSE: KMX) is preparing to publish second-quarter results on Thursday. Over the years, it has evolved into a diversified company, with the scale of operations and omnichannel strategy setting the foundation for long-term growth. Being the largest used car retailer in the country, CarMax is better equipped than its peers to tackle macroeconomic uncertainties and volatility in consumer demand, but elevated interest rates and rising auto loan delinquencies paint a gloomy picture of its near-term prospects.

Valuation

CarMax’s value has nearly halved since the stock retreated from the record highs of 2021, but this year it maintained an uptrend so far. Considering potential future headwinds, the shares look overvalued now. With normalcy returning to markets post-COVID, CarMax looks on track to further expand its market share in the coming years, which is good news for long-term investors. The market will be closely following the upcoming earnings report, looking for cues on the company’s future performance. The stock is gaining momentum ahead of the announcement.

Of late, margins have come under pressure from high SG&A spending. Meanwhile, measures adopted by the management are easing the cost pressure, which includes increasing used saleable inventory units, slowing the planned store growth, and halting share repurchases to ensure more capital flexibility. CarMax has better pricing power than others due to the good customer experience it provides in terms of selection and delivery, though average selling prices declined in recent quarters.

Q2 Report

The company’s second-quarter 2024 earnings report is expected on Thursday, September 28, before the opening bell. Experts’ projection indicates that the recent downtrend continued in the August quarter – net income is expected to decline 3% from last year to $0.77 per share on revenues of $7.01 billion, which represents an 18% decrease.

CarMax executives, in a recent statement, exuded hope that the remainder of fiscal 2024 would benefit from the cost-cutting program they initiated in the second half of 2023. For strengthening the SG&A-gross profit leverage over time, the company looks to achieve a rate in the mid-70% range on an annual basis.

“Regarding capital structure, our first priority remains to fund the business. While our adjusted net debt to capital ratio was slightly below our 35% to 45% targeted range, given ongoing market uncertainties, we continue to appropriately manage our net leverage to maintain the flexibility that allows us to efficiently access the capital markets for both CAF and CarMax as a whole. In keeping with this goal of maintaining flexibility, we continue to pause our share buybacks in the first quarter,” said CarMax CFO Enrique Mayor-Mora.

Earnings Dip

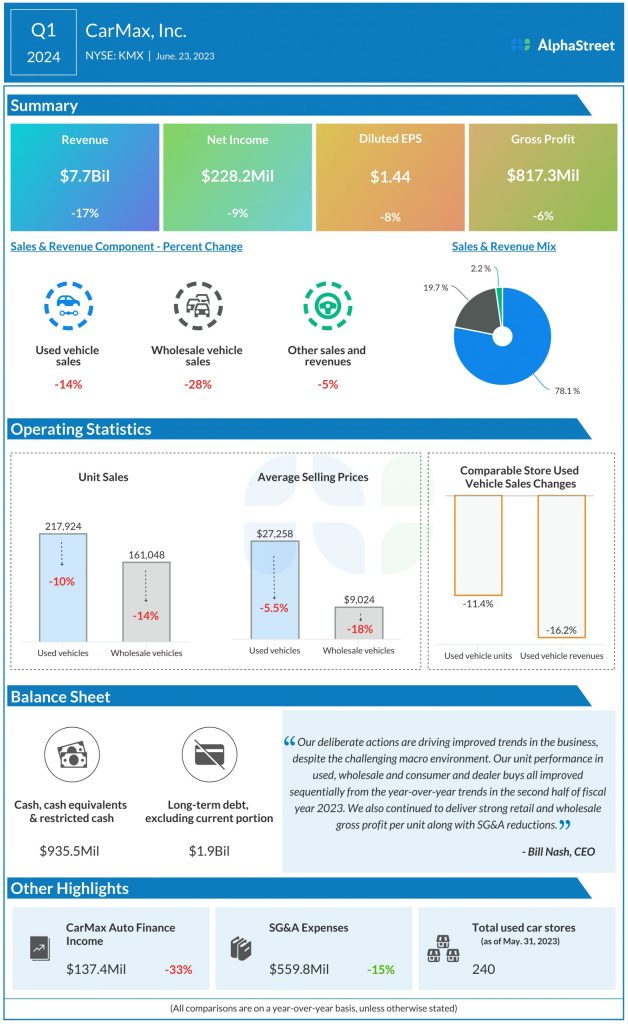

In the last two quarters, the company delivered stronger-than-expected earnings, after missing estimates for four quarters in a row earlier. In the first quarter ended May 2023, earnings declined 8% annually to $1.44 per share. At $7.7 billion, revenues were down 17% from last year and that reflects weakness across all operating segments – Used Vehicle Sales, Wholesale Vehicle Sales, and Other Sales and Revenues. Comparable store used vehicle sales and units declined in double digits.

CarMax’s stock, which is currently at a three-month low, traded sharply higher in early trading on Monday after closing the previous session lower.