For Kroger Co. (NYSE: KR), 2025 was a pivotal year as the retailer revisited its business strategy following the collapse of the Albertsons merger. The focus is on competing more effectively with market leaders like Walmart and Amazon. For 2026, the company’s growth plan centers on offering better prices, targeting the increasingly value-conscious customers. The company’s extensive private-label portfolio offers cheaper alternatives to national brands, helping retain customers while protecting margins.

When the grocery chain reports its Q4 FY25 results on March 5, before the opening bell, Wall Street analysts will be expecting around 2% year-over-year increase in revenues to $35.03 billion. The consensus earnings estimate, excluding special items, is $1.20 per share, compared to $1.14 per share in Q4 2024. The market is closely watching the event to see how the company’s price initiatives and e-commerce expansion influence overall performance. Private labels have become a significant part of Kroger’s business, growing faster than producer brands and helping the company defend margins amid pricing pressures.

After retreating from the all-time highs of August last year, Kroger shares experienced a downturn and slipped to a one-year low in early 2026. However, the stock changed course since then and has grown more than 10%. The company has regularly increased its quarterly dividend over the past many years, maintaining the yield near 2%.

ALSO READ: Key metrics from Kroger’s Q3 2025 earnings report

Mixed Outcome

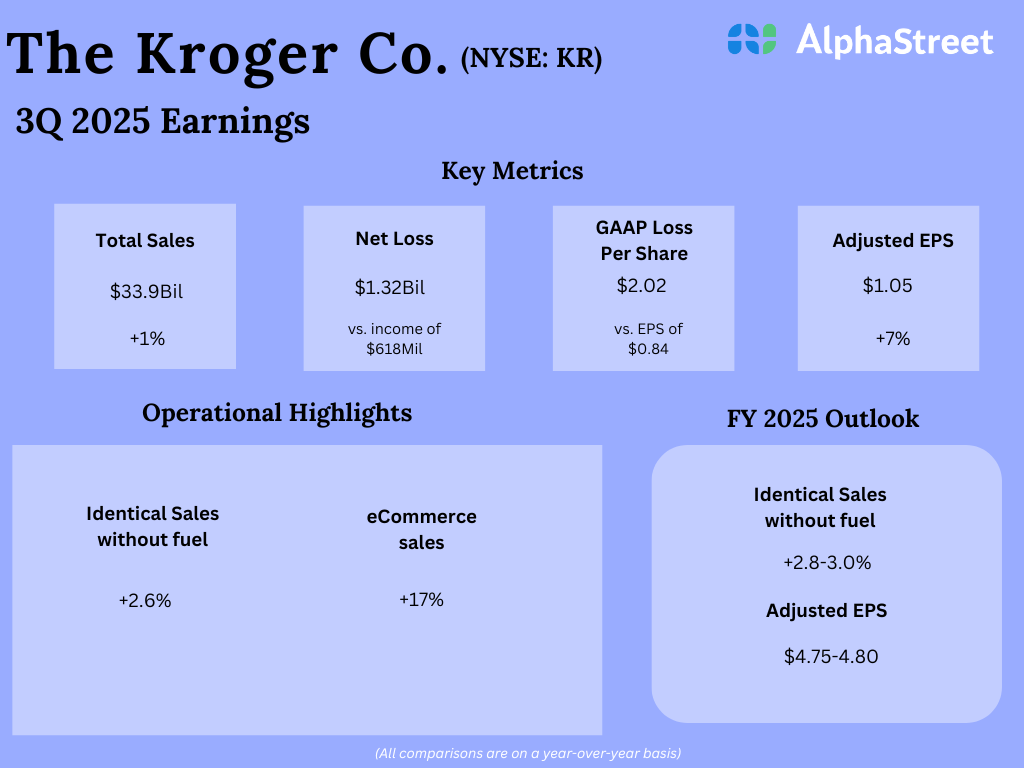

For the third quarter, Kroger reported earnings of $1.05 per share, on an adjusted basis, higher than $0.98 per share it earned in Q3 2024. Earnings came in above estimates, continuing the streak of outperformance that began in 2020. However, on a reported basis, it posted a net loss of $1.32 billion, reflecting merger-related charges. Total sales rose to $33.9 billion from $33.6 billion in the same period last year, but slightly missed expectations. Identical sales, excluding fuel, rose 2.6%. Management said it expects full-year adjusted earnings per share to be between $4.75 and $4.80. The guidance for FY25 identical sales growth is 2.8-3.0%, without fuel.

Ronald Sargent, then interim CEO of Kroger, said in the Q3 earnings call, “Looking ahead, we plan to accelerate capital investment in new stores beyond 2025 to strengthen our competitive position, expand into high-potential geographies, and support long-term growth. As we expand our footprint, our approach to site selection and store format starts with the customer, then prioritizes improving ROIC with a focus on delivering greater shareholder value.”

Digital Push

Kroger has consistently delivered positive identical-store sales growth in FY25, underscoring its resilience in a tough consumer environment. Middle and low-income customers remain under pressure due to elevated inflation and high interest rates. The company has been actively expanding its e-commerce footprint lately, reporting six consecutive quarters of double-digit digital sales growth. While Kroger has an aggressive store opening plan for the year, it continues to close underperforming stores and automated fulfillment centers, after its robotic fulfillment strategy failed to deliver expected returns.

The average price of Kroger’s stock for the past 12 months is $67.32. On Monday, the stock traded slightly higher in the early hours, after gaining approximately 10% in the past 30 days.