Kohl’s Corporation (NYSE: KSS) is slated to report its third-quarter 2019 earnings results on Tuesday, November 19, before the market opens. The results will be hurt by comparable sales as the consumer demand for a wide variety of merchandise are likely to fluctuate. This is due to an economic slowdown or uncertain economic outlook.

The retail chain has been struggling in the past due to stiff competition. Following this, the company has taken steps for transformation, which is likely to yield the results soon. During the third quarter, the company is expected to face on a rise in the expenses due to the investments in the expansion plans.

The company continues to make investments to target market share gains over the long term. Also, the company will incur additional charges related to the closure of its locations and voluntary role reduction program. However, digital demand is likely to accelerate driven by strong growth from Kohl’s app, its app visits, and conversion.

Analysts expect the company’s earnings to drop by 12.20% to $0.86 per share and revenue will decline by 5% to $4.39 billion for the third quarter. The company has surprised investors by beating analysts’ expectations thrice in the past four quarters. The majority of the analysts recommended a “hold” rating with an average price target of $56.

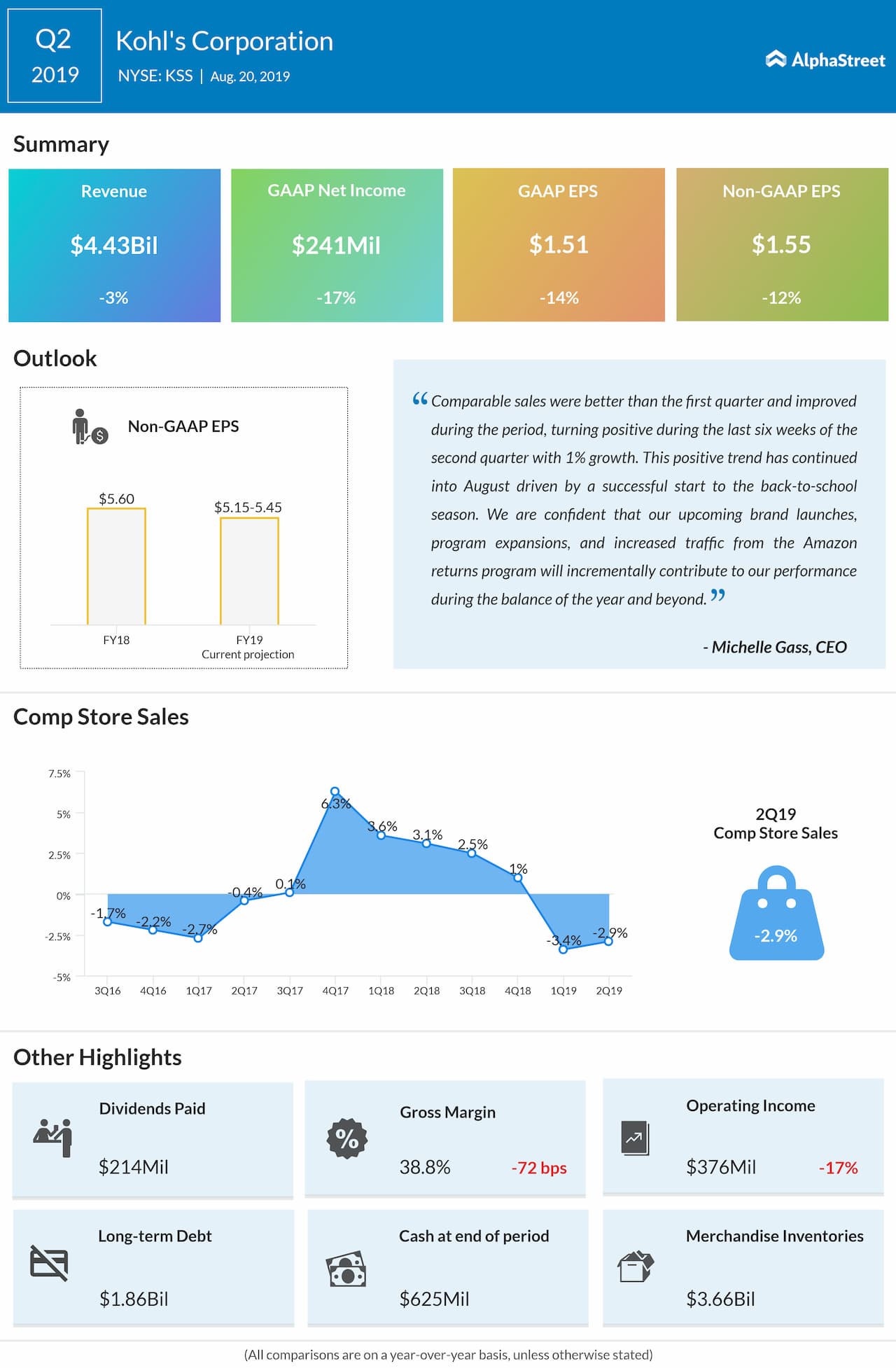

For the second quarter, Kohl’s posted a 17% decrease in earnings as a 2.9% decline in comparable sales hurt the top line. Comparable sales were better than the first quarter and improved during the period, turning positive during the last six weeks of the second quarter with 1% growth.

For the full year 2019, the company expects earnings in the range of $5.15 to $5.45 per share. This excludes $0.26 per share related to impairments, store closing and other costs recognized in the first six months of 2019.