The Kroger Co. (NYSE: KR) is preparing to report third-quarter results this week while navigating a challenging market environment. In the first half, the grocery chain’s performance was not very impressive, with adjusted earnings declining on flat sales as consumer spending remained under pressure.

After making steady gains over the past six months, Kroger’s stock climbed to an all-time high last week. The price has increased about 15% in the past six months. The company’s sales strategy has focused on keeping prices low to drive store traffic, which has partly contributed to the positive investor sentiment.

Estimates

When Kroger reports third-quarter results, Wall Street will be looking for earnings of $0.98 per share, compared to $0.95 per share in Q3 2023. Revenue is expected to stay broadly unchanged at $34.22 billion in the October quarter. The report is scheduled to be published on Thursday, December 05, at 8:00 am ET. The company has a history of delivering stronger-than-expected quarterly numbers – earnings beat estimates consistently for about four years.

From Kroger’s Q2 2024 earnings call:

“Customers continue adjusting to the current economic environment. The reduction of excess savings built up during the pandemic, higher interest rates, and the effect of inflation are pressuring customers’ ability to spend. This is especially true for our most budget-conscious customers as we’ve been seeing for a while now, but we’re now seeing other customer segments beginning to make changes as well. Customers are purchasing lower-priced cuts of meat, buying less, and focusing on essentials.”

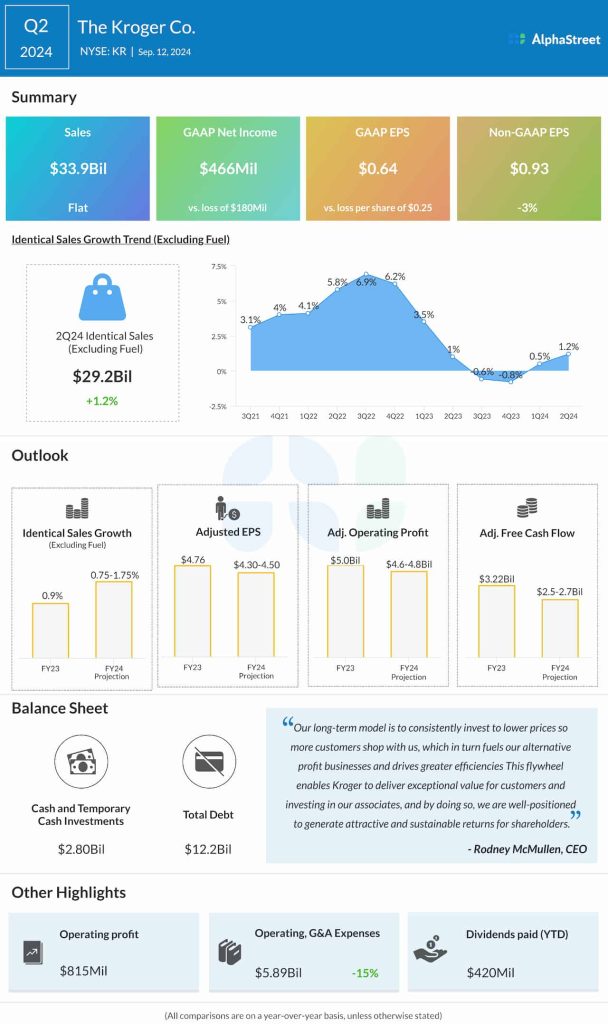

In the second quarter, identical sales rose 1.2% annually to $29.2 billion, continuing their recovery from the recent slowdown. At $33.9 billion, Q2 sales were unchanged from the year-ago period and fell short of expectations. Net income, adjusted for special items, declined 3% year-over-year to $0.93 per share during the three months. For the full fiscal year, the management forecasts adjusted earnings in the range of $4.30 per share to $4.50 per share. Identical sales, excluding fuel, are expected to grow 0.75-1.75% in FY24.

Headwinds

Of late, the grocery space has been experiencing stiff competition, with market leaders like Walmart and Costco trying to attract customers with promotional offers. Customers, in general, continue to cut back on discretionary spending and focus on buying essentials, despite economic conditions improving and interest rates dropping. Meanwhile, the Federal Trade Commission’s objection to the proposed Kroger-Albertsons merger, citing antitrust concerns, has triggered a legal battle between the two parties.

On Monday, Kroger’s stock dropped in the early hours, after maintaining an uptrend in recent sessions. It has grown by more than a third so far in 2024.