AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street Expects Steady Growth. Analysts expect L3Harris Technologies to report earnings of $2.57 per share on revenue of $5.41B when the aerospace and defense contractor announces first-quarter 2026 results on April 30th. The consensus reflects input from 12 analysts, with EPS estimates ranging from $2.48 to $2.83 and revenue projections spanning $5.26B to $5.56B.

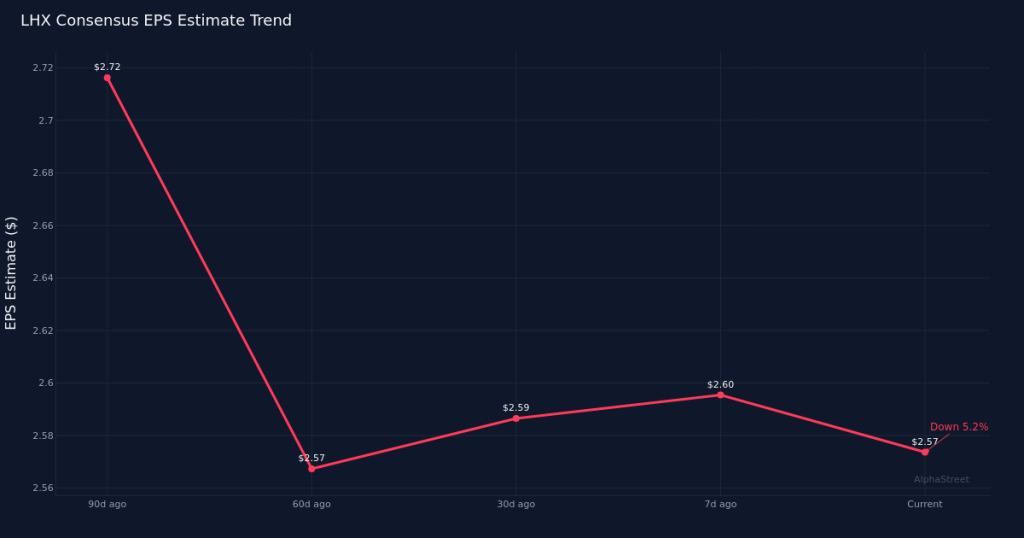

Downward Estimate Trajectory Signals Caution. Analyst sentiment has deteriorated in recent months, with the EPS consensus declining 0.8% over the past 30 days from $2.59 and falling 5.5% over the past 90 days from $2.72. This pattern of negative revisions suggests analysts have grown more conservative as the quarter progressed, potentially reflecting concerns about execution, program timing, or broader defense spending dynamics. The widening gap between current estimates and where they stood three months ago indicates material reassessment of near-term prospects rather than minor fine-tuning.

Year-Over-Year Comparison Shows Moderate Expansion. The consensus figures imply growth of 6.6% in earnings per share compared to year-ago EPS of $2.41, while revenue is expected to climb 5.5% from the prior-year total of $5.13B. Last year’s first quarter generated net income of $455.7M, translating to a net margin of 8.9%. Investors will be watching whether L3Harris can maintain or expand profitability as it scales revenue, particularly given the defense industry’s focus on program execution and cost discipline amid evolving Pentagon priorities and international security dynamics.

Defense Sector Context Matters. As a major defense prime contractor, L3Harris operates in an environment shaped by geopolitical tensions, modernization programs, and government budget cycles. The company’s portfolio spans communications systems, space capabilities, and electronic warfare technologies, making quarterly performance dependent on contract awards, production ramp schedules, and integration milestones. The aerospace and defense sector has faced scrutiny over supply chain pressures, labor availability, and the pace of classified program transitions, all of which could influence margin performance and cash generation in the quarter.

Profitability Trajectory Under Scrutiny. With year-ago net margin sitting at 8.9%, investors will examine whether operational leverage is materializing as revenue grows. Defense contractors typically face tension between top-line expansion and margin preservation, particularly when integrating acquisitions, ramping new platforms, or navigating fixed-price development contracts. Any commentary on program margins, cost recovery, or engineering non-recurring expenses will provide insight into the sustainability of profit growth beyond the current quarter.

Cash Conversion Remains Critical. For capital-intensive defense contractors, the relationship between reported earnings and cash flow often diverges due to working capital swings tied to contract milestones, advance payments, and inventory builds. Management’s discussion of cash generation, capital deployment priorities, and any updates to full-year free cash flow guidance will be as important as the headline earnings figure, especially given the sector’s emphasis on shareholder returns through dividends and buybacks.

Multiple Revenue Streams Create Complexity. L3Harris derives revenue from diverse defense programs spanning air, land, sea, space, and cyber domains. Quarterly results can be lumpy depending on delivery schedules for major platforms, the timing of international orders, and the stage of development for next-generation systems. Segment-level performance data and commentary on program health across the portfolio will help investors assess whether growth is broad-based or concentrated in specific capabilities.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.