Shares of Lamb Weston Holdings, Inc. (NYSE: LW) rose over 1% on Thursday. The stock has gained 4% over the past three months. The French fry giant is slated to report its earnings results for the second quarter of 2026 on Friday, December 19, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue

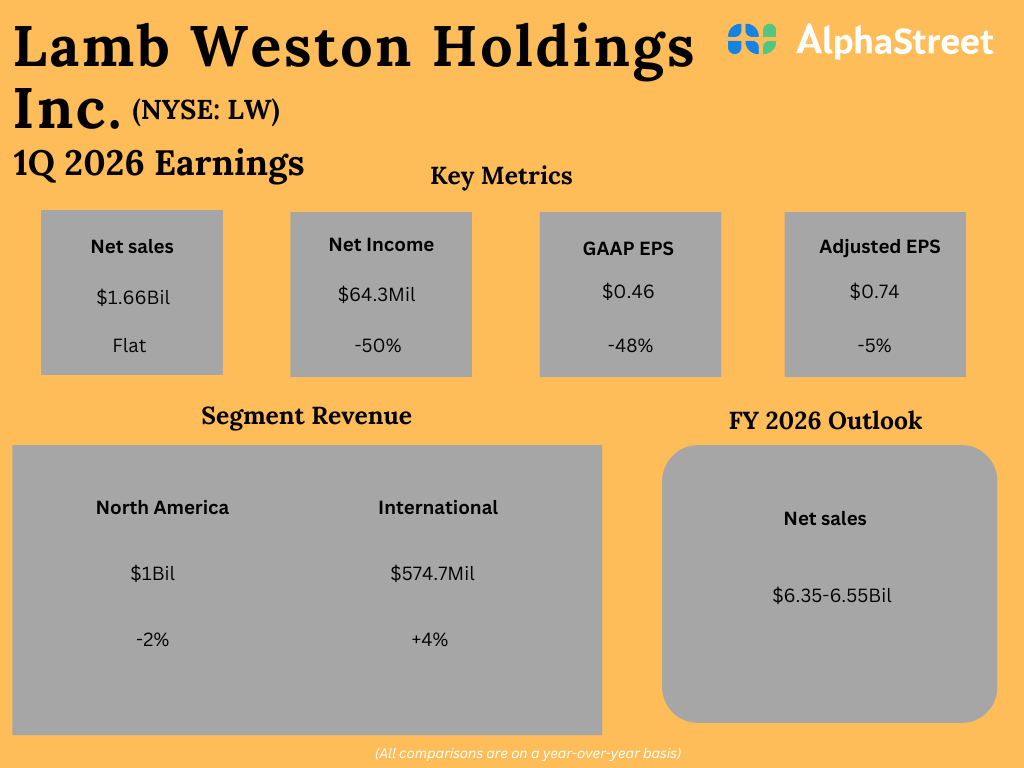

Analysts are projecting revenues of $1.59 billion for Lamb Weston in the second quarter of 2026, indicating a slight dip from $1.60 billion reported in the same period a year ago. In the first quarter of 2026, net sales of $1.66 billion remained relatively flat year-over-year.

Earnings

Analysts are predicting earnings of $0.64 per share for Q2 2026, which implies a 3% decline from Q2 2025. In Q1 2026, adjusted EPS decreased 5% YoY to $0.74.

Points to note

Lamb Weston can be expected to benefit from strong category demand. French fries remain immensely popular and their demand and appeal continue to grow across consumers of all generations. People are ordering fries more often with their meals, and as quick-service restaurants (QSR) expand, they introduce fries into developing markets, which helps in further expansion.

In Q1, Lamb Weston’s volumes increased 6%, driven by customer wins and retention. The company saw volume growth across both its North America and International segments, helped by customer contract wins, growth across channels, and gains from multinational chain customers. LW expects volumes in its North America segment to grow during the first and second half of the year, which is a positive sign for Q2.

However, subdued restaurant traffic remains a dampener. Last quarter, Lamb Weston saw restaurant traffic at several customer channels stay flat while some saw growth. Outside the US, restaurant traffic was mixed. The company saw a 4% decline in traffic in the UK, its largest international market.

Lamb Weston continues to make progress on its Focus to Win strategy. It is working on building customer partnerships, expanding its manufacturing network, and launching new innovative products. These efforts are expected to yield benefits.

LW anticipates continued headwinds from price/mix through the fiscal year, with the impact more pronounced in the first half. This does not bode well for Q2 results. The company expects gross profit margins in the second quarter to be relatively flat with the first quarter, along with low-single-digit inflation. It also expects margins in Q2 to be impacted by longer maintenance downtime at one of its plants and additional expenses related to the start-up of its Argentina plant.