Shares of Lamb Weston Holdings, Inc. (NYSE: LW) turned red in mid-day trade on Friday. The stock has dropped 19% in the past one month. The company delivered disappointing results for the second quarter of 2025 and cut guidance for the full year. The frozen potato products supplier expects headwinds to persist through the remainder of this fiscal year and into the next. Here are a few points to note:

Lackluster Q2 performance

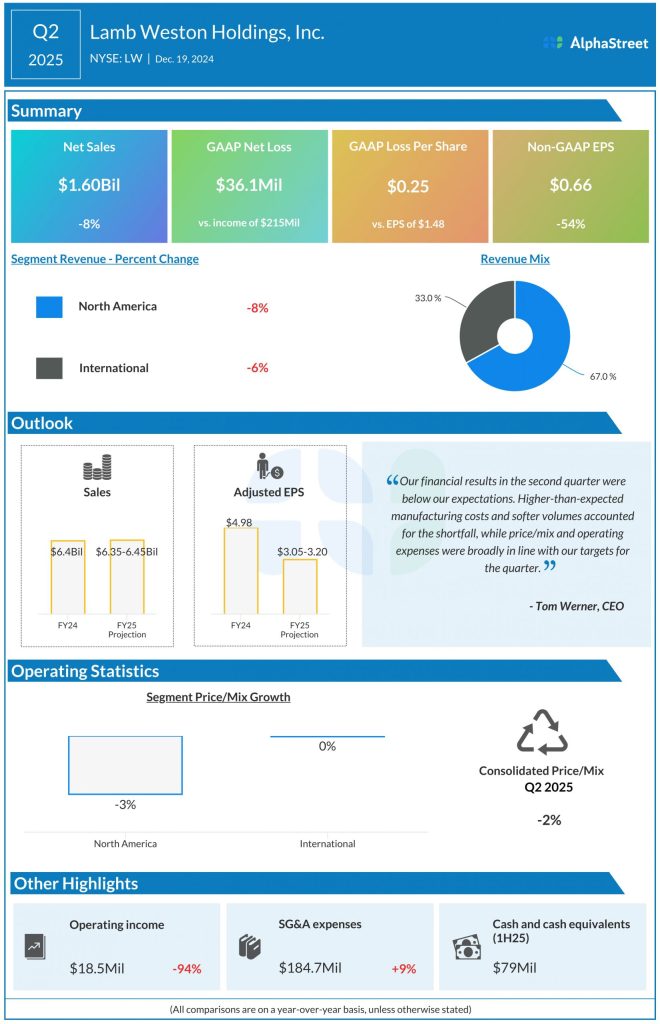

Lamb Weston’s sales and earnings for the second quarter of 2025 declined on a year-over-year basis and came below expectations. Net sales decreased 8% to $1.60 billion while adjusted earnings per share fell 54% to $0.66 in Q2.

The company saw volume decline 6% in the quarter, mainly due to weakness in global restaurant traffic, customer share losses, and impacts from the exiting of lower-price and lower-margin business in Europe. Sales and volume declined more than expected during the quarter due to incremental customer share losses in both segments caused by heavy competition.

In Q2, sales in the North America segment decreased 8% YoY. Volume fell 5%, mainly due to a decline in US restaurant traffic.

As mentioned on the conference call, US restaurant traffic dropped around 2% YoY in Q2. Despite a slight improvement sequentially owing to higher promotions by quick service restaurants (QSR), traffic trends remained down during the quarter. In addition, the fry attachment rate has remained steady, which is encouraging, but there has been a trade-down in serving size, which is a headwind to volumes.

Volumes in the North America segment were also hurt by the carryover impact of smaller and regional customer share losses in food away-from-home channels in the prior year as well as share losses in certain chain restaurant accounts.

Sales in the International segment fell 6% in Q2. Volume also fell 6%, mainly due to a drop in restaurant traffic across many key international markets. While restaurant traffic in the UK remained flat, it declined in Germany, France and Spain. China witnessed soft traffic growth, and in Japan, QSR traffic grew on a YoY basis but decelerated sequentially.

Volumes were also hurt by incremental customer share losses due to tough competition, particularly in the Middle East and certain markets in Asia Pacific. The exit of low-margin, low-price business in EMEA also impacted volumes in Q2, although this will be the last quarter LW sees this headwind.

Lowered outlook

Lamb Weston expects challenges in the operating environment to persist through the remainder of fiscal year 2025 and into fiscal year 2026, mainly due to an increasing rate of capacity additions and continued softness in global frozen potato demand, particularly outside North America.

The company lowered its outlook for fiscal year 2025 and now expects net sales to be $6.35-6.45 billion versus its previous expectation of $6.6-6.8 billion. Adjusted EPS is now expected to be $3.05-3.20 versus the prior outlook of $4.15-4.35.

As mentioned on its call, during the second half of the year, Lamb Weston expects incremental sales volume pressure in North America, due to the unexpected loss of a chain restaurant customer, and a larger-than-expected impact from the trade-down in serving size related to promotional meals. These headwinds may be partly offset by the benefit of some new customer wins.

In the International segment, the company expects volumes to be lower than previously expected, mainly due to incremental customer share losses caused by heavy competition, and softer restaurant traffic in key international markets. LW also expects incremental pricing pressure in each of its regions.

Lamb Weston is facing stiff competition in Asia Pacific and Latin America. Demand growth continues to slow and additional supply from Europe and new players in India, China and the Middle East are gaining share. The company is also moderating some of its pricing actions in EMEA. LW expects its net sales for FY2025 to decline 1% YoY, driven by a low to mid-single-digit decline in price-mix, partly offset by a low single-digit increase in volume growth.