Lloyds Banking Group Plc (NYSE: LYG) has reported a year of sustained strength in financial performance, meeting its 2025 guidance while accelerating strategic delivery. The Group’s results, announced on 29 January 2026, underscore a significant transformation since 2021, characterized by a purpose-driven growth strategy focused on “Helping Britain Prosper”.

Performance by Business Vertical

The Group achieved diversified growth across its core business verticals:

• Retail: Recorded a c.13% Compound Annual Growth Rate (CAGR) in Other Income (OOI) since 2021. This was driven by growth in motor finance, credit cards, and banking income.

• Insurance, Pensions and Investments (IP&I): Saw an 11% OOI CAGR, bolstered by workplace pensions and the integration of Lloyds Wealth.

• Commercial Banking: Achieved a c.6% OOI CAGR since 2021, with solid performance in Markets and Transaction Banking.

• Equity Investments: Grew by c.2% CAGR, significantly influenced by the Lloyds Living residential housing initiative.

Key Segment Developments

Lloyds continues to deepen its relationship with customers through targeted segment developments. The mortgage book grew by £10.8 billion year-on-year to £323.1 billion, maintaining a c.19% flow market share. In the pensions space, the Group now boasts over 750,000 Scottish Widows app users, an increase of over 75% year-on-year. Furthermore, Corporate and Institutional Banking (CIB) lending rose by £4.1 billion, focusing on strategic sectors such as infrastructure and project finance, which has more than doubled in scale since 2021.

Core Growth Strategies and Strategic Expansion

The Group’s strategy is built on three pillars: Grow, Focus, and Change.

• Grow: Leveraging integrated financial services to capture new opportunities in areas like Lloyds Wealth and digital motor lending.

• Focus: Improving capital efficiency through £24 billion in cumulative Risk-Weighted Asset (RWA) optimization since 2021.

• Change: Implementing a digital-first model, with over 50% of technology applications now on the cloud and a 50% reduction in physical data centers.

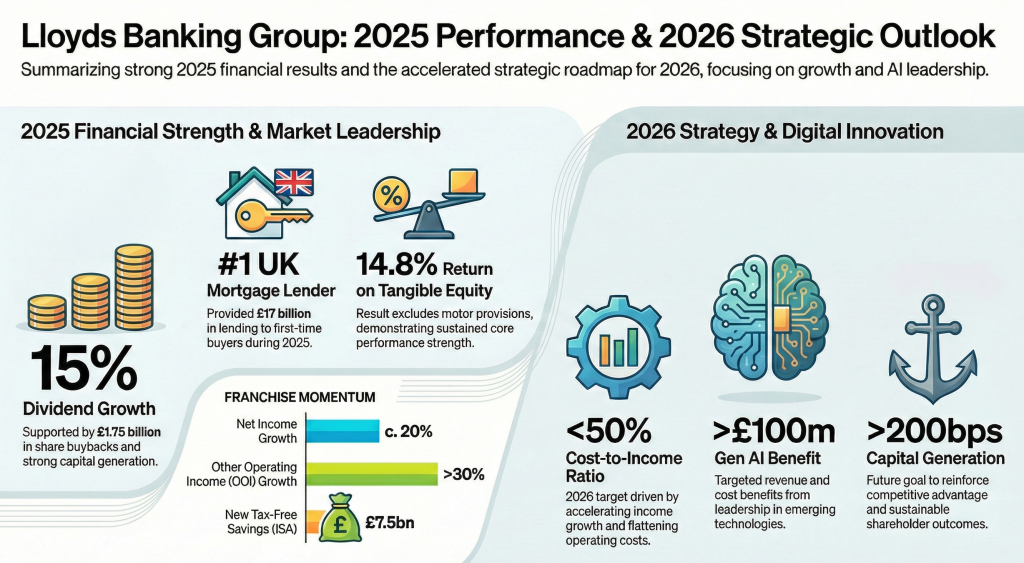

A centerpiece of their strategic expansion is Generative AI (Gen AI) leadership. The Group has c.50 live Gen AI use cases, which generated c.£50 million in P&L benefits in 2025, with a target of over £100 million in benefits for 2026.

Operational Scale and Market Leadership

Lloyds maintains a dominant position as the UK’s largest digital bank, recently rated “Outstanding” in Euromoney’s 2025 MarketMap. Its market leadership spans multiple categories, including being the #1 UK mortgage lender, #1 in credit cards and personal loans, and #2 in workplace pensions. Operational productivity has also improved, with a 45% increase in active customers served per distribution FTE since 2021.

Robust Capital Strength

The Group’s balance sheet remains resilient, with a pro forma CET1 ratio of 13.2%. Capital generation was robust at 147 basis points (178 basis points excluding motor provisions). The Group has signaled its intent to review excess capital distributions every half-year moving forward and plans to pay down to a c.13.0% CET1 ratio by the end of 2026.

Interim Dividend, Performance, and Shareholder Value

For the 2025 fiscal year, Lloyds reported a statutory profit after tax of £4.8 billion, with a Return on Tangible Equity (RoTE) of 12.9% (14.8% excluding motor provisions). This strong performance enabled a total dividend of 3.65 pence per share, representing 15% growth over the previous year. Additionally, the Group announced a share buyback of up to £1.75 billion, contributing to a total of c.£15 billion in shareholder distributions since 2021.

Outlook and Growth Trajectory

Looking ahead, Lloyds has upgraded its 2026 guidance, expressing confidence in its trajectory beyond 2026. Key 2026 targets include:

• Net Interest Income: c.£14.9 billion.

• Cost:Income Ratio: Under 50%.

• RoTE: Greater than 16%.

• Capital Generation: Greater than 200 basis points. The Group operates within a supportive UK economic environment, with a forecast average GDP growth of 1.4% per annum through 2029 and anticipated interest rate cuts by the Bank of England in 2026. Management remains committed to delivering stronger, sustainable returns while continuing to lead as an integrated financial services provider.