Shares of Lowe’s Companies, Inc. (NYSE: LOW) stayed red on Wednesday. The stock has dropped 8% over the past three months. The home improvement retailer is scheduled to report its earnings results for the first quarter of 2025 on Wednesday, May 21, before market open. Here’s a look at what to expect from the earnings report:

Revenue

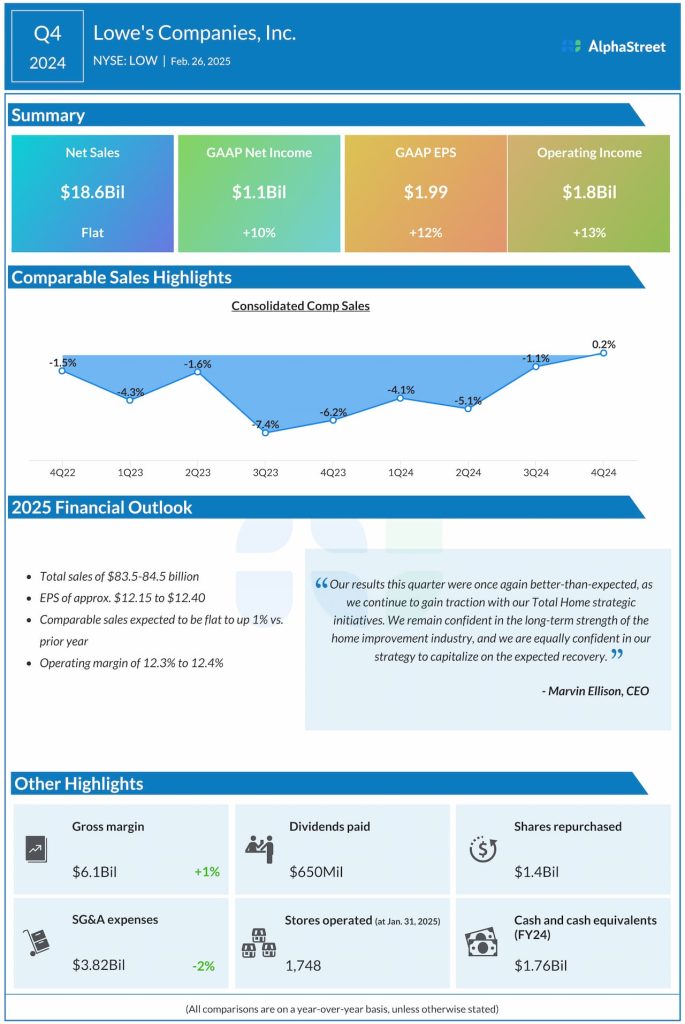

Analysts are projecting revenue of $21 billion for Lowe’s in the first quarter of 2025, which implies a 1% dip from the same period a year ago. In the fourth quarter of 2024, revenues remained flat year-over-year at $18.6 billion.

Earnings

The consensus estimate for earnings per share in Q1 2025 is $2.90, which compares to EPS of $3.06 reported in Q1 2024. In Q4 2024, adjusted EPS amounted to $1.93.

Points to note

The macroeconomic pressure on large discretionary projects seen over the past couple of quarters is likely to have continued in the to-be reported one as well. The impact from the ongoing tariff situation also remains to be seen. Lowe’s is likely to have benefited from seasonal demand and spring projects in Q1.

On its last quarterly call, Lowe’s forecast the home improvement market to be roughly flat in 2025, with the Pro segment outpacing the DIY segment, driven by repair and maintenance needs. The investments the company is making such as the loyalty program, assortment, discounts, and so on are anticipated to drive growth in the Pro segment. It is also expected to benefit from the initiatives laid out as part of its Total Home Strategy.

Based on these factors, Lowe’s expects comparable sales to be flat to up 1% in 2025. The company expects comp sales in the first half to be roughly flat, with some spring demand moving from the first quarter into the second quarter, as it cycles poor weather. Based on this, it expects comp sales in the first quarter to be approx. 200 basis points below the bottom end of its full-year guide.

The pressures in the home improvement market may not abate in the near term but the company’s efforts in driving growth in the Pro segment, particularly with the small and medium Pro, and its investments in its Total Home Strategy are likely to boost its performance.