Shares of Lowe’s Companies (NYSE: LOW) stayed in green territory on Monday. The stock has dropped 29% year-to-date and 18% over the past three months. Last week, the company delivered mixed results for its first quarter of 2022 with earnings beating estimates and revenues falling short of projections. Here are a few points to keep in mind if you are considering this stock:

Revenue

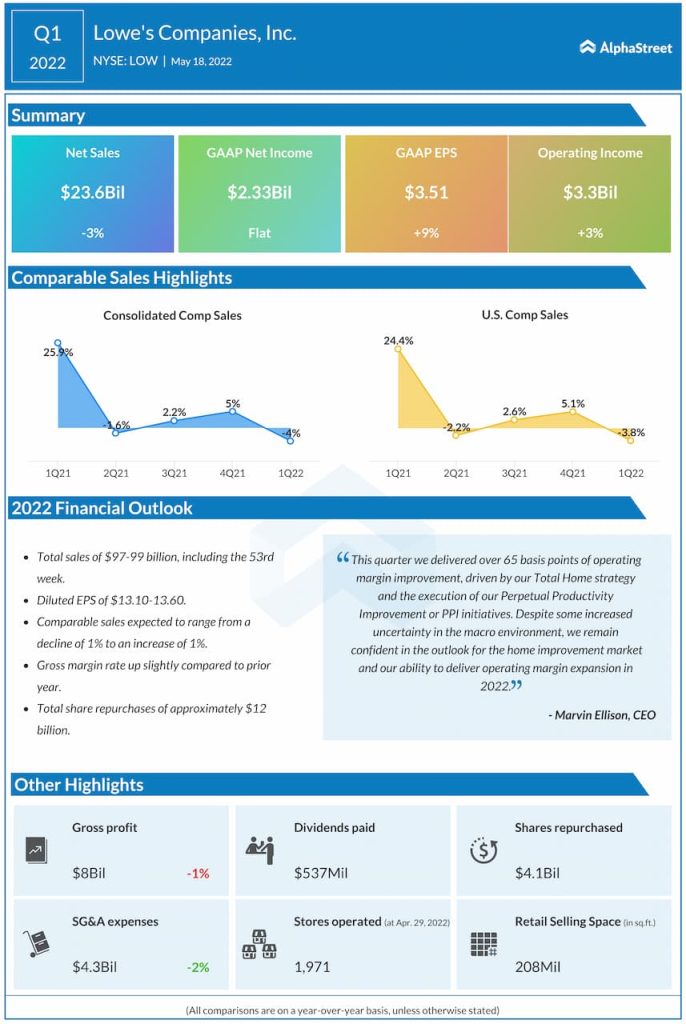

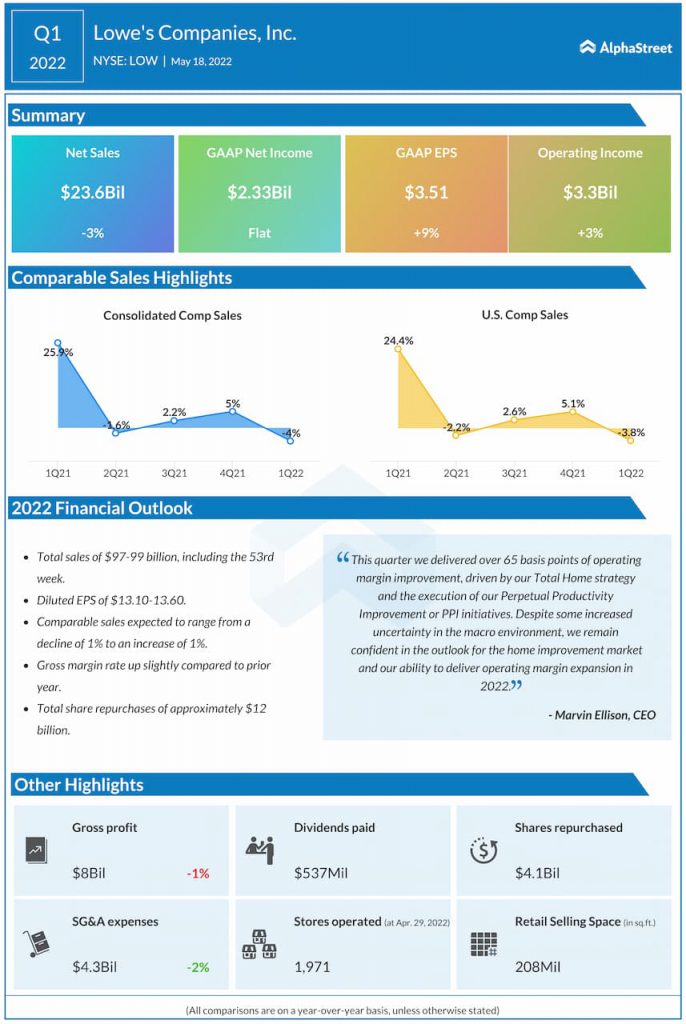

Lowe’s total sales in Q1 decreased 3% year-over-year to $23.7 billion while comparable sales fell 4%. Comparable sales for the US home improvement business was down 3.8%. Last year’s top line results included the benefit of government stimulus. During the quarter, sales in the Pro division outpaced the DIY division and while demand for core DIY categories stayed strong, lower sales in seasonal categories impacted sales by approx. $350 million.

The company expects the Pro category to outpace the DIY category for the year. Total sales for FY2022 is expected to range between $97-99 billion. The outlook includes a 53rd week, which equates to approx. $1-1.5 billion in sales. Comparable sales are expected to range between down 1% to up 1%.

Profitability

Lowe’s delivered earnings of $3.51 per share in Q1, which was up 9% YoY, driven by an improvement in gross margins as well as expense management. Gross margin rose 74 basis points to 34.03%. Operating margin expanded by 67 basis points to 13.96%. Margins during the quarter benefited from effective cost management and a favorable product mix.

Lowe’s expects gross margin rate for FY2022 to be up slightly compared to last year. Gross margin pressure is anticipated to shift into the second quarter due to a decline in lumber prices. This is expected to lead to a slight increase in gross margin during the first half of this year versus the same period last year. Operating margin is expected to range between 12.8-13% while EPS is estimated to be $13.10-13.60.

Category performance

On its quarterly conference call, Lowe’s said it witnessed strong momentum in its Pro category as its Pro customers continue to see strong business demand and a full slate of projects for the year. The company saw a 20% growth in comps for the Pro category during the first quarter.

The Pro category outpaced the DIY category during the quarter. Around 75% of the company’s sales come from the DIY customer and Lowe’s saw solid DIY demand for core non-seasonal home improvement projects in Q1.

However, many seasonal categories like grills and patio furniture are more heavily concentrated in the DIY category and the late arrival of spring impacted sales in this division. The company witnessed double-digit sales declines in many of its northern markets during the quarter.

Despite some uncertainty in the macro-environment, the company’s long-term outlook for the home improvement industry remains positive. The appreciation in home prices gives homeowners confidence to go for big-ticket purchases. Factors like the extension of remote work, the age of the housing stock and millennial household formation are all long-term tailwinds for home improvement.