Athletic apparel retailer Lululemon Athletica (NASDAQ: LULU) started the new fiscal year on an upbeat note, reporting double-digit sales growth for the first quarter despite macroeconomic uncertainties and a general shift in consumer spending. Customer traffic, both online and at stores, has remained stable at a time when some of the other leading retailers are experiencing a slowdown in sales.

Last week, the Vancouver-headquartered athleisure brand’s stock rallied after it reported positive results for the first quarter of 2023. After hitting an all-time high more than a year ago, it has been a roller-coaster ride for the stock so far.

Tailwinds

An acceleration in Greater China sales contributed to the sales growth in recent quarters, while a moderation in freight costs and improvements in the supply chain helped margins. Demand for the company’s high-end yoga pants and athletic wear remained high even after it raised prices last year. Sales have not been materially affected by the shift in people’s spending patterns amid high inflation and economic slowdown.

That said, efforts are needed to have a more balanced inventory, which was up 24% in the most recent quarter and is expected to remain high in the coming months. Also, if the pullback on discretionary spending continues, amid recessionary fears, that is likely to affect Lululemon’s sales going forward. As of now, higher-income shoppers who account for a major chunk of the company’s customers keep buying its products as they are equipped to handle the macro pressures.

“We have a target to quadruple our business outside North America between 2021 and 2026. This will be driven predominantly by our existing markets, but we’ll be entering some exciting new markets as well. In 2022, international represented only 16% of our revenue, and I remain optimistic about our runway of global growth. As I stated earlier, our business remained strong in North America and across our international regions,” said Lululemon’s CEO Calvin McDonald at the Q1 earnings call.

Strong Q1

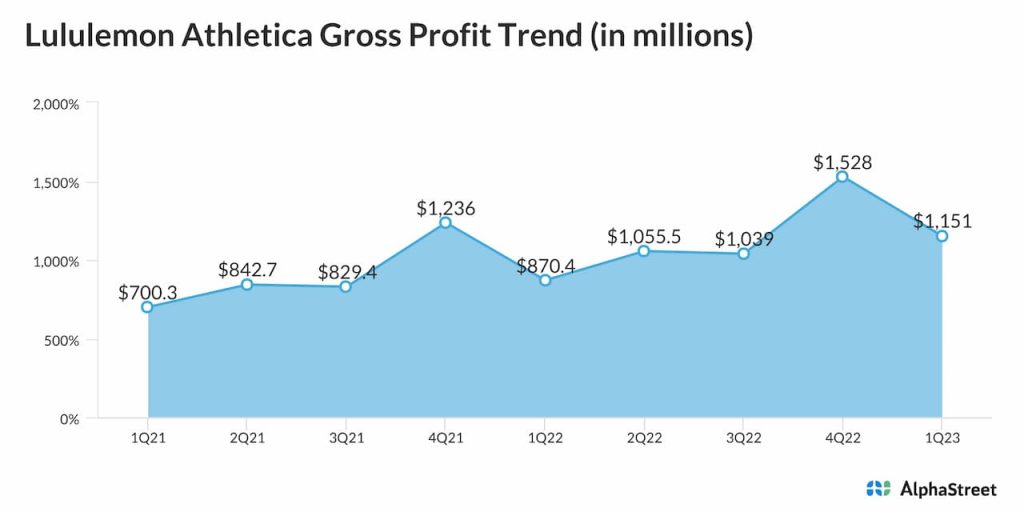

Over the past four years, Lululemon’s sales and earnings topped expectations in every quarter, and the trend continued in the April quarter. First-quarter revenues increased 24% from last year to about $2 billion, with sales growing in double digits in North America and the rest of the world. In China, revenue grew a whopping 79%, reflecting the ongoing market reopening.

There was a 14% increase in comparable sales and a 16% growth in direct-to-customer revenues. While comps exceeded estimates, DTC sales fell short of expectations. Net income increased to $290.4 million or $2.28 per share in the first quarter from $190 million or $1.48 per share last year.

Guidance

Encouraged by the solid outcome, the leadership raised the full-year guidance. For fiscal 2023, the company now expects revenue to be $9.44-$9.51 billion, and earnings per share in the range of $11.74 to $11.94. It also expects second-quarter revenue to be in the range of $2.14 billion to $2.17 billion, which is up 15% year-over-year. The forecast for Q2 earnings is between $2.47 per share and $2.52 per share.

Lululemon’s stock is up 10% since the beginning of the year. It traded slightly higher on Tuesday afternoon, extending the post-earnings uptrend.