Lyft Inc. (NASDAQ: LYFT) delivered better-than-expected results for the second quarter of 2020. Despite falling 61% year-over-year, revenues managed to beat consensus estimates while adjusted net loss came in narrower than expected. The stock has dropped 31% since the beginning of the year.

COVID-19 impact

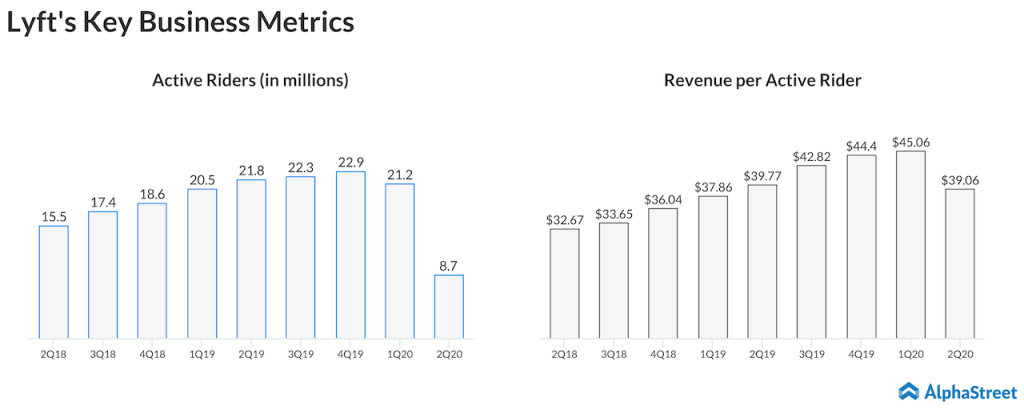

Rideshare rides declined remarkably during the second quarter due to a drop in active riders as shelter-in-place mandates and other restrictions reduced travel in general. This led to a 61% drop in total revenue. Ride frequency remained more resilient as revenue per active rider fell only 2% despite the difficult environment.

The company has seen a recovery in rides since the second week of April, and while airport rides fell significantly in April and remain down year-over-year, weekly airport rides rose by over 350% between April and late June.

Demand has rebounded and the company saw a 78% increase in rideshare rides in July versus April. From June to July, the growth was 12%. Rideshare rides for the week ending August 9 reached a new high since April but was down 53% year-over-year.

Bike Share

The bike share operations witnessed strong engagement during the quarter with revenue increasing both sequentially and year-over-year. Weekly bike rides rose over 200% during the quarter while new bike rider activations increased 11% year-over-year in June.

Bike ride volumes are currently above pre-COVID levels. The company’s e-bikes are now available in San Francisco, New York, Chicago, Washington DC, Minneapolis and Columbus and it is working on expanding the availability to more markets later this year.

Profitability

Lyft expects to achieve adjusted EBITDA profitability by the fourth quarter of 2021. Given its cost reduction actions and increased unit economics, the company believes it can achieve adjusted EBITDA profitability with 20-25% fewer rides than what was needed when it previously disclosed its target last October.

Lyft estimates it can achieve adjusted EBITDA profitability when quarterly rides on its rideshare platform reach around 5-10% above the level achieved in Q4 2019. The company expects to see strong organic revenue growth year-over-year in 2021.

Driver classification

In terms of the litigation issue on driver classification in California, earlier this week, the Superior Court of California granted a preliminary injunction motion filed by the State, which would force Lyft and Uber (NYSE: UBER) to reclassify drivers as employees in California. Lyft plans to appeal this ruling and request a further stay but if unsuccessful, the company would be forced to suspend operations in California.

Outlook

Lyft remains on track to achieve its fixed cost savings of $300 million on an annualized basis by the fourth quarter of this year. The company also expects to lower its Capex for 2020 to $125 million, which is better than its previous target of $150 million. Adjusted EBITDA loss for the third quarter is estimated to be $265 million if rides remain at July levels.

Click here to read the full transcript of Lyft Q2 2020 earnings call