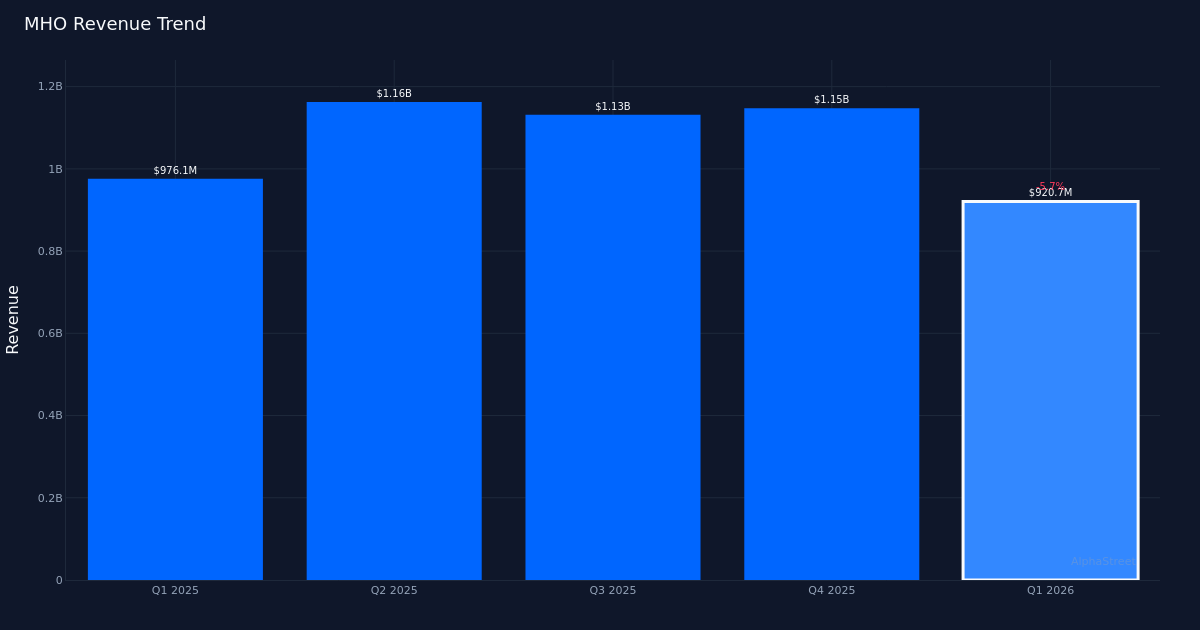

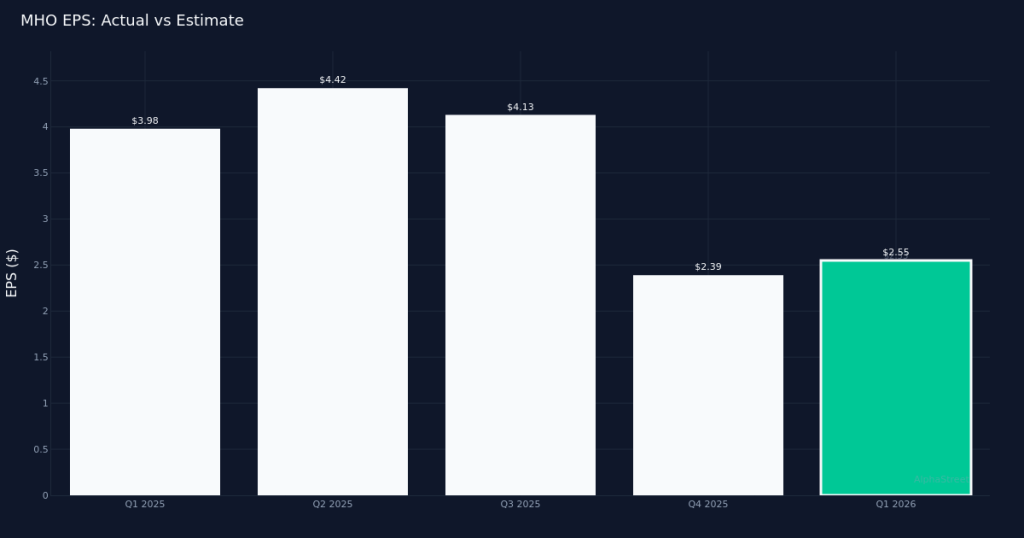

Narrow beat delivered. M/I Homes, Inc. (NYSE:MHO) posted Q1 2026 diluted earnings of $2.55 per share, edging past the analyst consensus of $2.53 by 0.8%. The homebuilder generated $920.7M in revenue for the quarter, translating to net income of $67.8M. While the modest beat demonstrates execution amid a challenging environment, the year-over-year comparisons reveal meaningful headwinds as both earnings and revenue contracted from the prior-year period.

Year-over-year pressures intensify. The quarter’s results reflect a 35.9% decline in EPS from the $3.98 reported in Q1 2025, while revenue fell 5.7% from $976.1M in the year-ago period. This compression in profitability outpacing the revenue decline suggests margin deterioration, likely driven by elevated incentives and pricing pressure in a market grappling with affordability constraints and elevated mortgage rates. The company’s ability to eke out a slight earnings beat against this backdrop speaks to cost discipline, though the magnitude of the profit decline will likely weigh on investor sentiment.

Operational footprint maintained. M/I Homes operated 230 communities at quarter end, providing the geographic diversity and lot position needed to navigate regional market variations. The company recorded 2,350 units in new contracts during the quarter, a critical leading indicator for future closings and revenue generation. This sales pace, when viewed against the revenue decline, suggests either lower average selling prices or a mix shift toward more affordable product, both of which would be consistent with builders adapting to current buyer affordability challenges.

Market shows cautious optimism. The stock traded at $132.72, up 2.9% following the release, indicating investors are giving management credit for the earnings beat despite the challenging comparisons. The muted price reaction reflects the difficult balance between near-term margin pressure and the potential for a housing recovery as demographics and supply constraints provide longer-term tailwinds. Wall Street maintains a constructive stance with analyst consensus standing at 4 buy ratings, 1 hold, and 0 sell recommendations, suggesting the investment community sees value at current levels despite cyclical headwinds.

Quality of beat questioned. The earnings outperformance, while positive, comes against a backdrop of sharply lower year-over-year profitability. Without corresponding revenue strength—revenues actually declined—the beat appears driven more by expense management and potentially lower tax rates rather than robust operational momentum. Institutional investors will scrutinize whether margin compression stabilizes in coming quarters or accelerates if the company must maintain elevated incentives to move inventory.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.