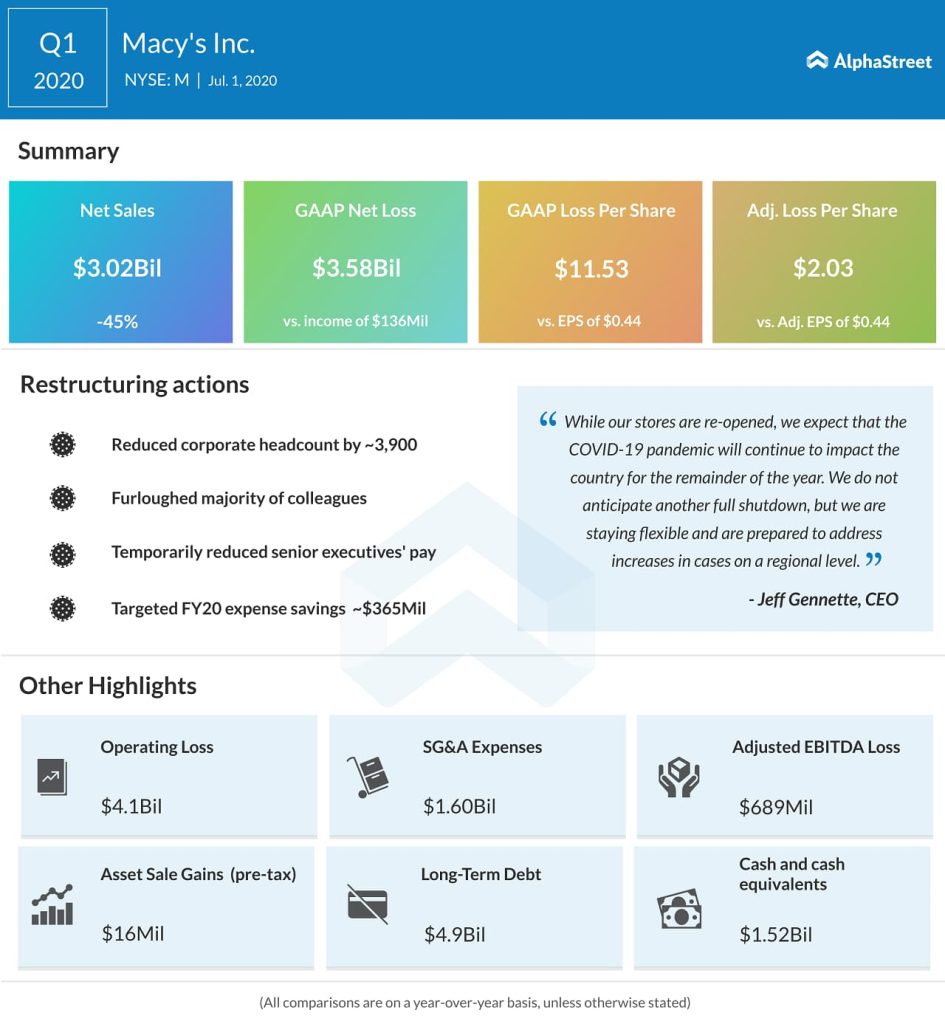

The retail industry was hit hard by the COVID-19 pandemic. The shelter-in-place orders and store closures impacted several major retailers and department store giants. Macy’s Inc. (NYSE: M) was one of them and the retailer reported a net loss of $3.5 billion for the first quarter of 2020.

But Macy’s problems are not new. The company has been

struggling for a while now and the pandemic just made things worse. Looking

ahead, despite the retailer’s optimism, the road to recovery is an

unpredictable one.

Past performance

Over the past five years, Macy’s net sales have continued to decline, witnessing a drop of 9% from 2015 to 2019. In fiscal year 2019, net sales declined 1.6% compared to 2018, with weakness in categories such as women’s sportswear and handbags. During this time period, the company’s profits have also rapidly fluctuated.

The sales trend over the past five quarters also follow a

relatively similar pattern with net sales witnessing year-over-year declines

every quarter. Net sales in the fourth quarter of 2019 fell 1.42% versus the

year-ago period.

Macy’s comparable sales, both owned and owned plus licensed,

have slowed down over the past five quarters. After witnessing increases of 0.6%

(owned) and 0.7% (owned plus licensed) in the first quarter of 2019, the number

slowed to 0.2% and 0.3% in the second quarter. This was followed by sharp

decreases of 3.9% and 3.5% in the third quarter. The company saw comps fall in

the fourth quarter of 2019 as well.

Looking at Macy’s sales trend by categories, over the past

three years, net sales in women’s apparel have steadily declined. The other

categories such as women’s accessories, shoes, cosmetics, men’s and kid’s and

home have remained relatively flat during this period.

Over the past couple of quarters, these categories have not

seen much of a pickup and have more or less declined. The home category alone saw

an increase of 1.7% in the second quarter of 2019 versus the year-ago period.

Quarterly results

This just turned worse in the first quarter of 2020 with the coronavirus outbreak forcing Macy’s to close all its stores in March. The retailer saw a sharp drop in net sales which fell 45% year-over-year to $3 billion. Diluted loss per share was $11.53 compared to EPS of $0.44 in the year-ago period. Due to the store closures, the company recorded an inventory write-down of around $300 million, mainly on fashion merchandise.

Digital

The company’s digital business saw good momentum with double-digit gains in the first and second quarters of 2019 but slowed down in the third quarter. Despite this, it ended fiscal 2019 on a strong note making up 26% of net sales compared to 23% in 2018 thanks to strong holiday sales.

In the first quarter of 2020, digital sales declined in the low single digits versus the prior-year quarter. Despite the decline, the company stated on its conference call that the digital business has been performing well and it is expected to grow at a healthy double-digit rate through the latter half of the year. The beauty and furniture categories have seen strong online sales in particular.

Polaris strategy

Earlier this year, Macy’s announced its Polaris strategy, a

three-year plan designed to stabilize profitability and drive growth. The

components of the strategy included streamlining costs, optimizing the store

portfolio and accelerating digital growth. The savings from Polaris were

expected to total around $1.5 billion in 2022.

However, the COVID-19 pandemic has led Macy’s to re-examine the strategy to decide which areas to move forward with and which to put on hold. The actions associated with the strategy are expected to continue through 2022 but it is not possible to quantify the benefits or costs at present.

Macy’s is undertaking restructuring activities and has

announced job cuts as part of these efforts. The restructuring is expected to yield

savings of approx. $365 million in fiscal year 2020. The company is expected to

incur around $180 million in additional costs for the restructuring, which will

be largely related to severance.

Looking ahead, Macy’s expects a slow recovery but remains cautious about unpredictable challenges that might arise in the back half of the year. The company expects to see a 6-7% comp improvement in the second quarter versus the first quarter.

The digital business is expected to outperform. The company saw digital sales penetration of approx. 43% in the first quarter and the annual digital sales penetration is expected to average in the mid-40s.

Click here to read the full transcript of Macy’s Q1 2020 earnings conference call