Shares of The J.M. Smucker Co. (NYSE: SJM) rose over 4% on Tuesday after the branded foods maker delivered an encouraging earnings report for the second quarter of 2025. Both the top and bottom line numbers beat expectations and the company raised its earnings guidance for the full year. Here are the main takeaways from the Q2 report:

Better-than-expected results

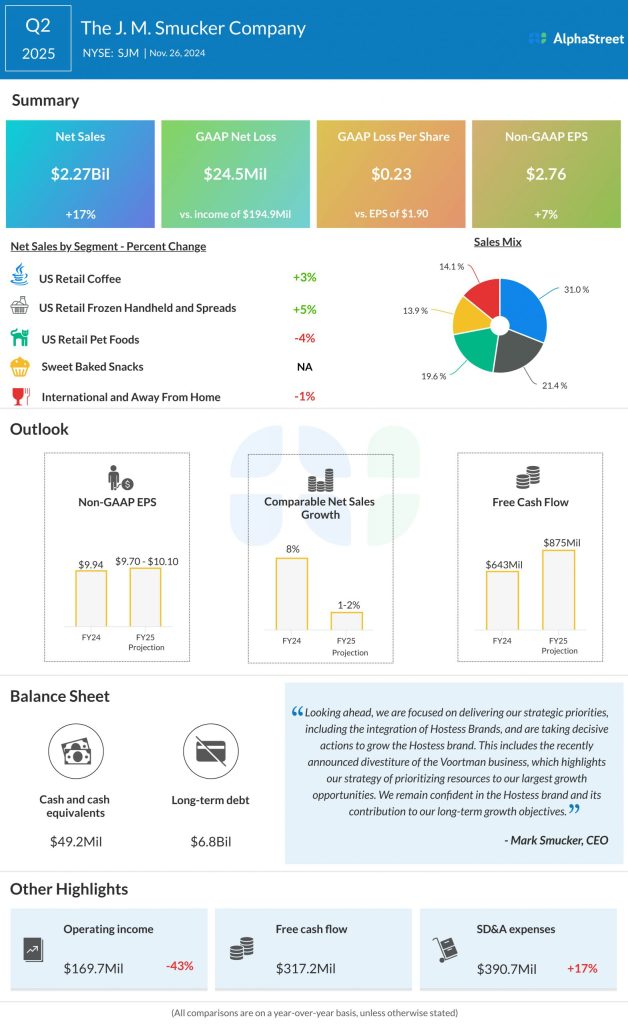

SJM’s net sales for Q2 2025 increased 17% year-over-year to $2.27 billion, beating estimates of $2.26 billion. Comparable sales increased 2%. The company reported a GAAP loss of $0.23 per share. Adjusted EPS grew 7% to $2.76, surpassing the consensus target of $2.51.

Business performance

In Q2, sales in the Coffee segment grew 3%, driven by price increases. The segment benefited from gains in the Café Bustelo and Folgers brands. Sales in the Frozen Handheld and Spreads division grew 5%, fueled by growth in the Uncrustables and Jif brands.

The Pet Foods segment recorded a sales decline of 4%, due to lower sales related to the divested pet food brands and decreases for the Canine Carry Outs and Pup-Peroni brands, which were offset by gains in the Milk-Bone and Meow Mix brands. Sales in International and Away From Home fell 1%.

SJM continues to focus its resources on the brands it believes have the highest growth potential, namely Uncrustables, Meow Mix, Milk-Bone, and Café Bustelo. The Uncrustables brand grew net sales by 16% at the total company level. The new facility at Alabama is expected to help the brand cross $1 billion in net sales. SJM now expects net sales for this brand to be over $900 million in fiscal year 2025. The Milk-Bone brand gained from double-digit sales growth in soft and chewy snacks while Meow Mix continues to maintain its leading position. Café Bustelo grew sales by 20% in Q2.

Hostess and Voortman

Sales from the Hostess brand continue to be below SJM’s expectations, as the sweet baked goods category faces headwinds from inflationary pressures and lower discretionary income, which have led to declines across all channels, including convenience stores. The company is working on driving growth for this brand through distribution expansion, product innovation, portfolio evolution, and revenue synergies.

The company has decided to divest its Voortman business and this deal is expected to close in Q3 2025. The transaction is expected to impact fiscal year 2025 net sales by approx. $65 million and adjusted EPS by approx. $0.10.

Guidance hike

J.M. Smucker raised its earnings guidance for the full year of 2025 and now expects adjusted EPS to range between $9.70-10.10 versus the previous outlook of $9.60-10.00. Net sales is expected to increase 8.5-9.5% from the previous year and comparable sales is expected to increase around 1-2%.