Shares of McCormick & Company, Incorporated (NYSE: MKC) were down over 2% on Tuesday following the announcement of the company’s third quarter 2025 earnings results. While the top and bottom line numbers came above expectations, the company lowered its earnings guidance for the full year due to higher costs and tariffs.

Better-than-expected results

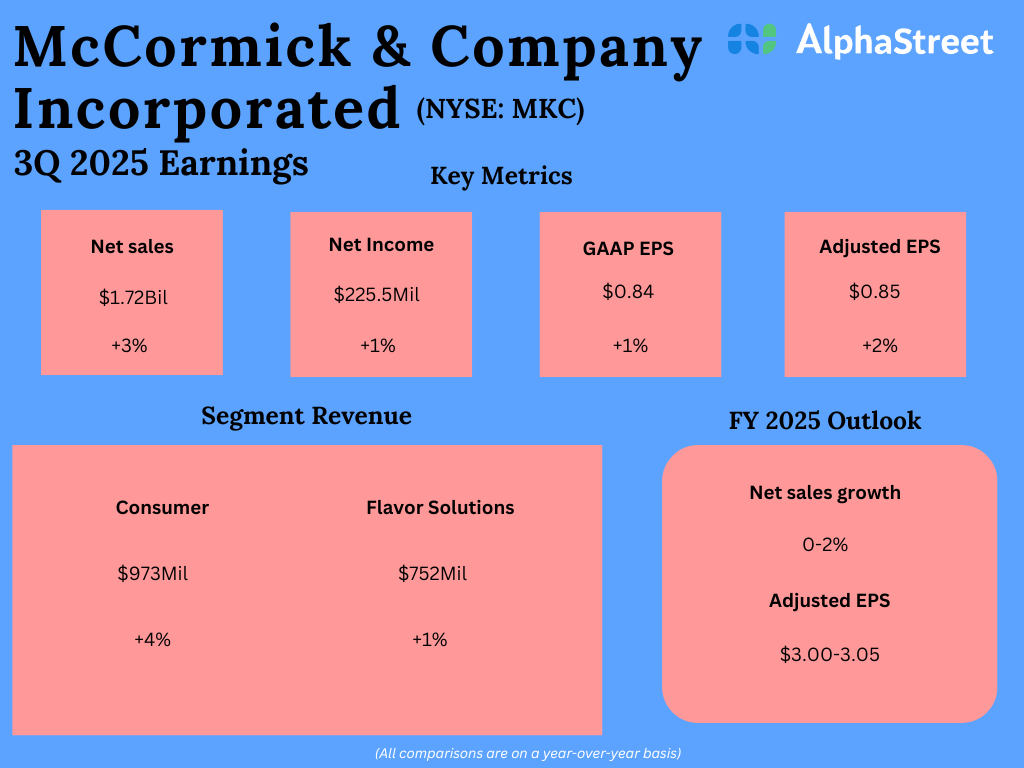

In Q3 2025, McCormick’s sales and earnings increased versus the year-ago period and surpassed market expectations. Net sales grew 3% to $1.72 billion, beating estimates of $1.71 billion. On a GAAP basis, earnings per share rose 1% to $0.84. Adjusted EPS grew 2% to $0.85, exceeding projections of $0.82.

Business performance

In Q3, McCormick’s organic sales grew 2% year-over-year, driven by volume growth of over 1%. Gross margin decreased by 130 basis points in the quarter. Margins were impacted by higher commodity costs, tariffs, and costs to support future growth investments. These headwinds were partly offset by cost savings from the Comprehensive Continuous Improvement (CCI) program.

Net sales in the Consumer segment increased 4% to $973 million. Organic sales grew 3%, driven by volume and product mix. This segment saw sales growth in the Americas and EMEA regions while APAC stayed flat. It also saw volume growth in these regions, barring APAC which saw a decline. It benefited from gains in categories like spices and seasonings, mustard, and hot sauce.

Sales in the Flavor Solutions segment rose 1% to $752 million, with organic sales also up 1%. This segment saw sales growth across all regions. Volumes dipped in the Americas and EMEA regions but in APAC, it grew 9%. This division benefited from strong QSR performance in the Americas and APAC regions, but was hurt by soft volumes from CPG customers in the Americas and EMEA, and by weak foot traffic in branded foodservice in the Americas.

Guidance cut

McCormick lowered its earnings outlook for fiscal year 2025 to reflect rising commodity costs and incremental tariffs. The company now expects GAAP EPS to range between $2.95-3.00, representing a year-over-year growth of 1-3%, versus its previous expectation of $2.98-3.03.

Adjusted EPS is now expected to be $3.00-3.05, representing YoY growth of 2-4%, or 4-6% in constant currency, versus the earlier expectation of $3.03-3.08. MKC continues to expect net sales growth of 0-2%, or 1-3% in constant currency, for the year.