Rev YoY +10.3%|Net Margin 0.1%

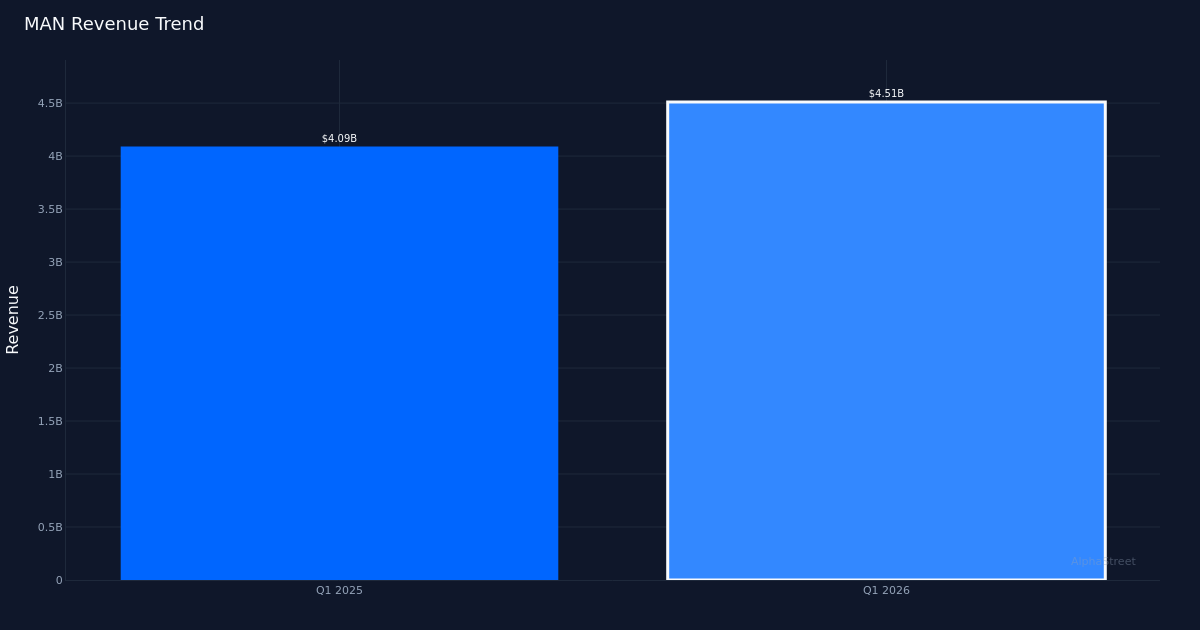

ManpowerGroup (NYSE: MAN) delivered a decisive earnings beat in Q1 2026, posting adjusted EPS of $0.51 against estimates of $0.49, while revenue climbed to $4.51B. The earnings surprise marks a return to profitability momentum for the staffing giant. Unadjusted EPS dropped to $0.05 from $0.12 in the year-ago quarter. Revenue growth of 10.3% year-over-year signals stabilization in demand for employment services after a challenging prior-year period, though the quality of that growth warrants closer examination.

The profitability picture reveals razor-thin margins that expose the fundamental challenge in this business. Net margin stood at just 0.1% on net income of $2.5M, unchanged from the year-ago net margin of 0.1%. This anemic profitability despite double-digit revenue growth indicates ManpowerGroup is operating in an intensely competitive environment where pricing power remains constrained. Operating income of $28.3M tells a similar story—the company is generating volume but struggling to convert top-line expansion into meaningful bottom-line results. Gross margin of 16.0% on gross profit of $723.0M provides some cushion, but the deterioration from gross profit to operating income underscores a heavy overhead burden that the company must address.

Management’s strategic response acknowledges this structural margin pressure directly. The announcement of a “strategic global transformation program” targeting $200 million in permanent cost savings by 2028 represents a clear recognition that current operating leverage is insufficient. This initiative becomes critical to improving profitability, as organic revenue growth alone—even at the 3% organic constant currency rate management cited—won’t dramatically alter the margin profile without concurrent expense discipline. The transformation program suggests management sees a multi-year path to normalized profitability rather than expecting near-term margin expansion from revenue recovery alone.

Revenue momentum appears sustainable based on management’s forward indicators and Q2 guidance trajectory. Management noted that “System-wide revenue, which includes our expanding franchise revenue base, was $5.0 billion,” pointing to a broader revenue base beyond the reported $4.51B figure. The Q2 2026 adjusted EPS guidance of $0.91 to $1.01, with a midpoint of $0.96, implies sequential acceleration from Q1’s $0.51 result and suggests management sees improving demand conditions. Management’s commentary that “it’s good to be back to growth here, and thinking about the guide of organic constant currency, same-day basis of 3% is pretty similar to the first quarter” indicates confidence in sustaining the current pace rather than expecting dramatic reacceleration or deceleration.

Weather-related headwinds masked stronger underlying performance in certain operations during the quarter. Management specifically flagged that one business segment “was up 5% in the quarter, actually a bit impacted by weather, extreme weather in the quarter, probably was about a 1% drag, so it would have been about 6%.” This suggests the normalized growth rate exceeds reported figures and that Q2 could benefit from easier seasonal comparisons if weather patterns normalize. The stock price increase to $30.73 following the earnings release indicates investors are giving management credit for execution despite the margin challenges.

The key tension is whether revenue growth can persist while management simultaneously executes margin expansion. The 10.3% reported revenue growth provides a solid foundation, but converting that growth into acceptable returns on capital requires the cost transformation program to deliver as promised. With the thin operating margin currently, even achieving half of the targeted $200 million in savings by 2026-2027 would meaningfully improve profitability. The challenge lies in executing cost reductions while maintaining service quality and competitive position in a fragmented staffing market where scale advantages are difficult to capture.

Management’s emphasis on returning to growth carries strategic significance beyond the headline numbers. The statement that “In the first quarter, we delivered reported revenues of $4.5 billion, representing an organic constant currency growth of 3%” positions the quarter as an inflection point after what was clearly a difficult comparison period. The consistency of the 3% organic constant currency growth expectation into Q2 suggests this reflects genuine demand stabilization rather than one-time factors, though sustaining this pace through 2026 will require continued labor market resilience.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.