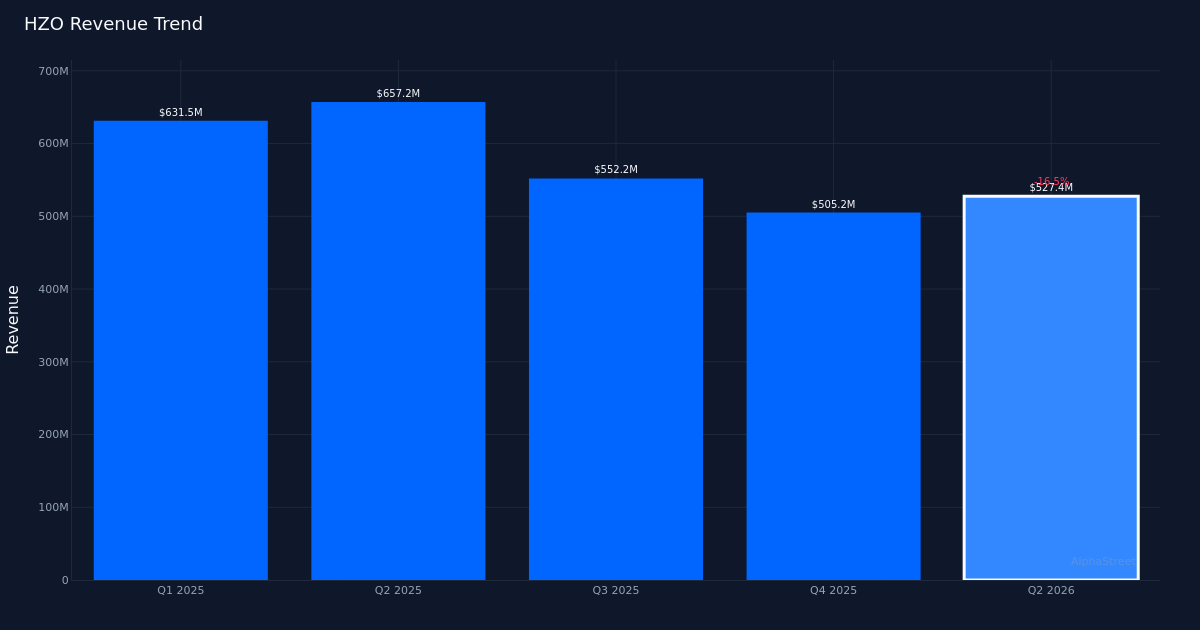

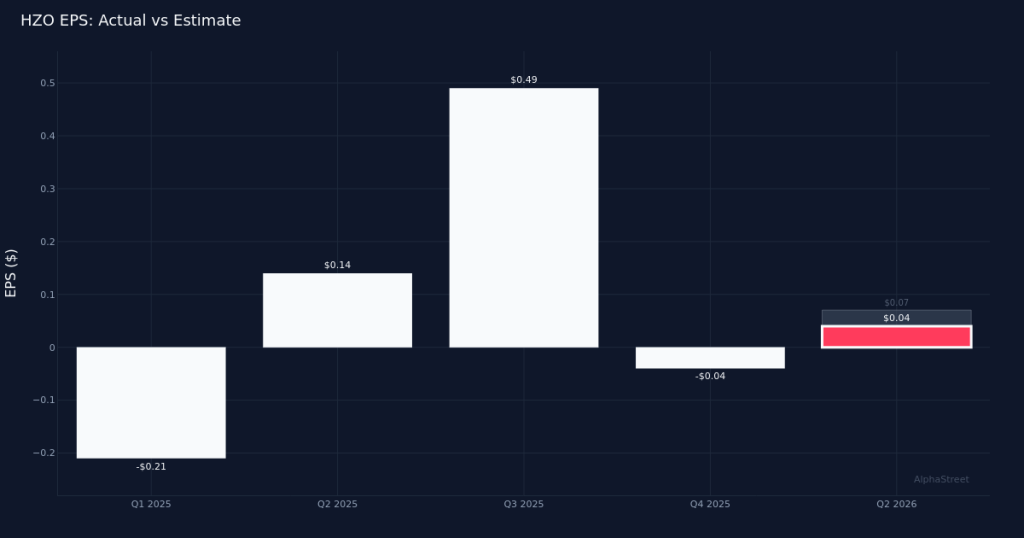

Earnings miss. MarineMax, Inc. (NYSE:HZO) delivered Q2 2026 adjusted earnings of $0.04 per share, falling short of the $0.07 consensus estimate by 42.9%. The specialty marine retailer posted revenue of $527.4M, down 16.5% from $631.5M in the year-ago quarter, as the company continues navigating challenging market conditions in the recreational boating sector. Bottom-line profit came in at just $900,000, underscoring the margin pressure facing the business amid softening consumer demand for discretionary big-ticket purchases.

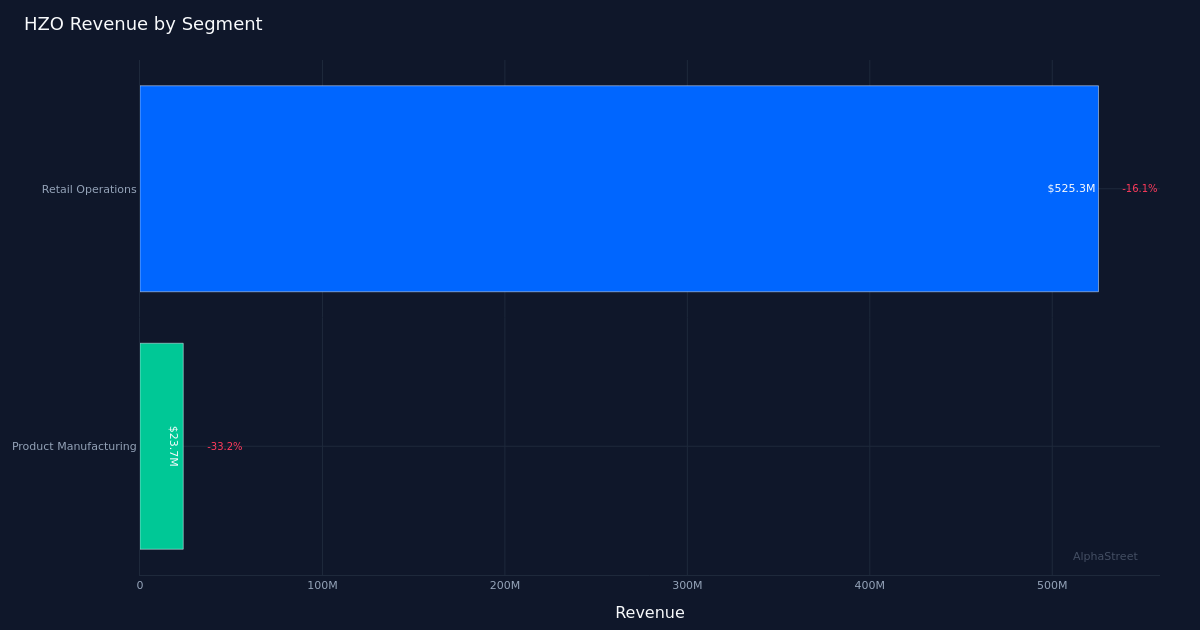

Weak comparable trends. Same-store sales declined 15.0% for the quarter, reflecting the challenging demand environment plaguing marine retailers as elevated interest rates and economic uncertainty keep potential boat buyers on the sidelines. This metric is particularly telling for MarineMax’s core business health, as it strips out the impact of new location openings and captures true demand trends at existing dealerships. The company’s Retail Operations segment, which generated $525.3M in revenue, declined 16.1% year-over-year, indicating broad-based weakness across the retail network of 120 total locations worldwide.

Margin compression evident. The quality of this quarter’s results raises concerns, as the earnings miss appears driven primarily by top-line pressure rather than controllable operational issues. With revenue down 16.5% while profit margins compressed dramatically to generate only $900,000 in net income, the company is clearly struggling to maintain profitability amid volume declines. The nearly non-existent bottom line suggests that cost-cutting measures have been unable to offset the revenue headwinds, a troubling dynamic for a retailer facing sustained demand weakness.

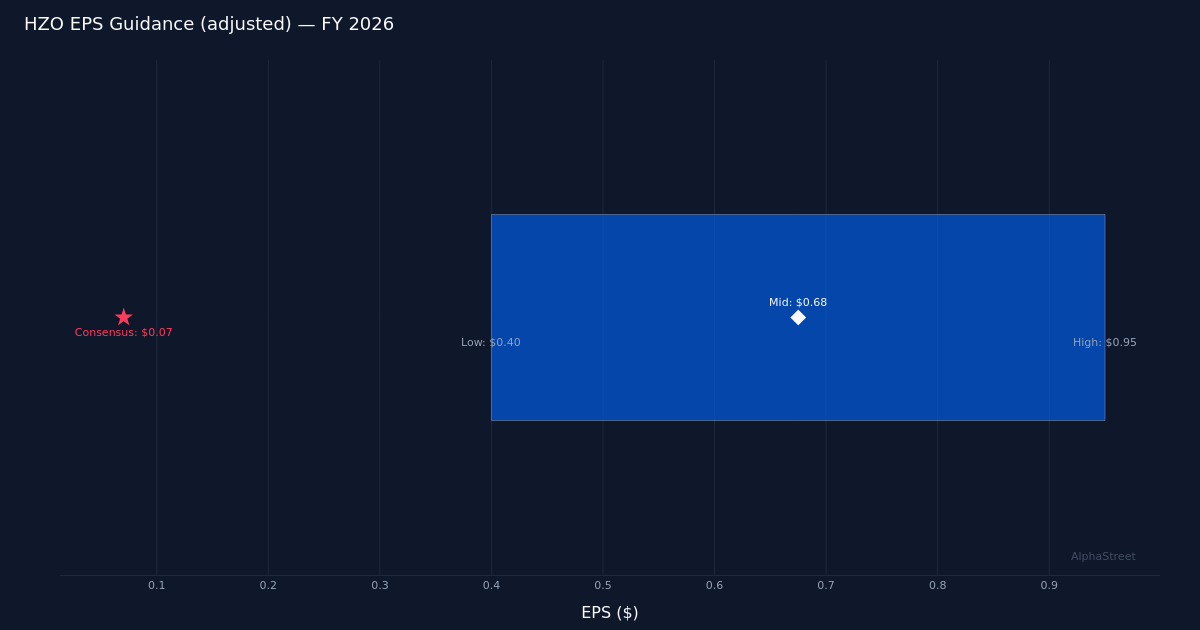

Muted guidance range. Management guided full-year FY 2026 adjusted EPS to a range of $0.40 to $0.95, a wide band that reflects significant uncertainty about the timing of a potential recovery in marine retail. The midpoint of $0.68 suggests the company expects continued headwinds throughout the fiscal year, with limited visibility into when consumer sentiment might improve enough to drive a meaningful rebound in boat sales. This cautious outlook aligns with broader industry concerns about affordability constraints and financing costs in the current environment.

Market reaction negative. Shares fell 2.1% to $29.29 following the release, a relatively modest decline that suggests investors may have already braced for disappointing results given broader marine retail trends. Despite the near-term challenges, Wall Street maintains a constructive view with analyst consensus showing 6 buy ratings, 3 hold ratings, and 0 sell ratings, indicating belief that the current downturn represents a cyclical trough rather than structural impairment.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.