US futures are pointing to a higher open today after ending lower on Friday, as geopolitical worries faded after President Donald Trump tweeted stating the mission was accomplished. However, traders remained concerned that the US is intending new sanctions against Russia after the strikes in Syria. Investors turned their focus from the geopolitical situation to a busy earnings week.

The S&P futures rose 0.56% to 2,672.25, Dow futures advanced 0.62% to 24,486, and Nasdaq gained 0.58% to 6,679.25. Elsewhere, shares at Asian markets closed mostly lower on Monday, while European stocks are trading lower.

On the European economic front, data from Destatis showed that Germany’s manufacturing employment rose 2.7% to 5.6 million at the end of February from last year. Turkstat data revealed that Turkey’s industrial production grew 9.9% on year in February after increasing 12% in January. Turkish Statistical Institute data showed that Turkey’s unemployment rate rose to 10.8% in January from 10.4% in December.

Destatis data revealed that Germany’s wholesale prices increased at a steady pace of 1.2% on year in March from last month. The Hellenic Statistical Authority data showed that Greece consumer prices fell 0.2% on year in March after rising 0.1% in February. Statistics Denmark data revealed that Denmark’s producer prices increased 1.7% on year in March after rising 1.1% in February.

On the Asian economic front, data from the Statistics New Zealand showed that food prices in New Zealand rose 1% on month in March after falling 0.5% in February. Department of Statistics data revealed that Malaysia’s unemployment rate fell to 3.3% in February from 3.4% in January. Statistics Bureau data showed that Indonesia’s exports grew 6.14% and imports increased 9.07% on year in March. Ministry of Commerce & Industry data revealed that India’s wholesale price inflation slowed to 2.47% in March from 2.48% in February. The Urban Redevelopment Authority showed that Singapore home sales climbed to 716 new units in March from 374 units in February.

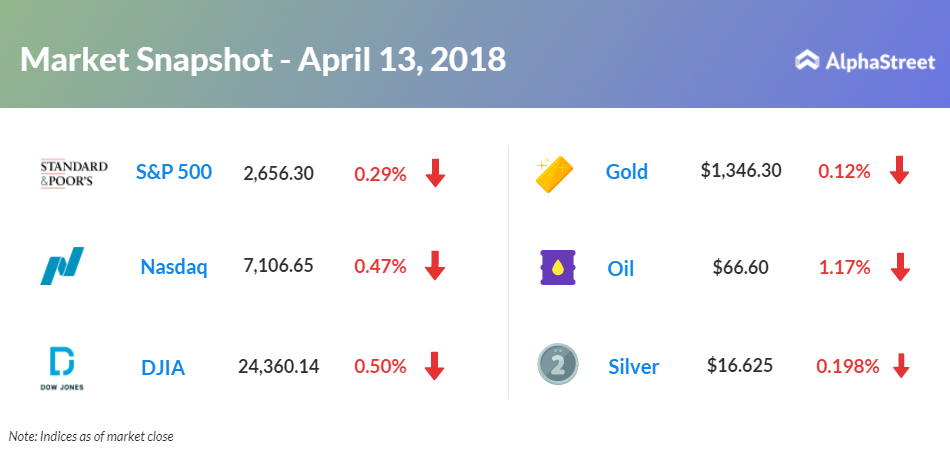

On April 13, US ended lower, with Dow down 0.50% to 24,360.14. Nasdaq fell 0.47% to 7,106.65, and the S&P 500 tumbled 0.29% to 2,656.30. The stock ended in red after seeing initial strength due to better-than-expected earnings from giants JPMorgan Chase (JPM), Citigroup (C) and Wells Fargo (WFC).

Meanwhile, key economic events scheduled for today include Commerce Department’s retail sales, Empire State manufacturing survey, Commerce Department’s business inventories, National Association of Home Builders/Wells Fargo’s housing market index, and Treasury International Capital data. Atlanta Federal Reserve Bank President Raphael Bostic and Dallas Fed President Robert Kaplan will be giving speeches today.

On the corporate front, Bank of America (BAC) inched up 0.94% in the premarket after better-than-expected first-quarter results. Netflix (NFLX) stock rose 1.27% in premarket ahead of first-quarter results. WPP Plc (WPP) stock fell 4.41% in premarket after executive chief Martin Sorrell has resigned over a probe into a personal misconduct allegation. Alkermes (ALKS) stock jumped 17.02% in the premarket after its new drug application for depression treatment was accepted by the FDA.

Crude oil futures are down 1.17% to $66.60. Gold is trading down 0.12% to $1,346.30, and silver is down 0.198% to $16.625. On the currency front, the US dollar is trading down 0.01% at 107.311 yen. Against the euro, the dollar is up 0.33% to $1.2369. Against the pound, the dollar is up 0.50% to $1.4307.